Unlocking Your Home-Buying Potential: A Financial Guide

Unlocking Your Home-Buying Potential: A Financial Guide

Whether you’re drawn to the timeless appeal of a rustic retreat or the sleek design of a modern dwelling, understanding your financial eligibility is the first step toward homeownership. With strategic planning and expert guidance, your ideal home may be closer than you think. Learn how to assess your buying power and enhance your chances of securing a mortgage.

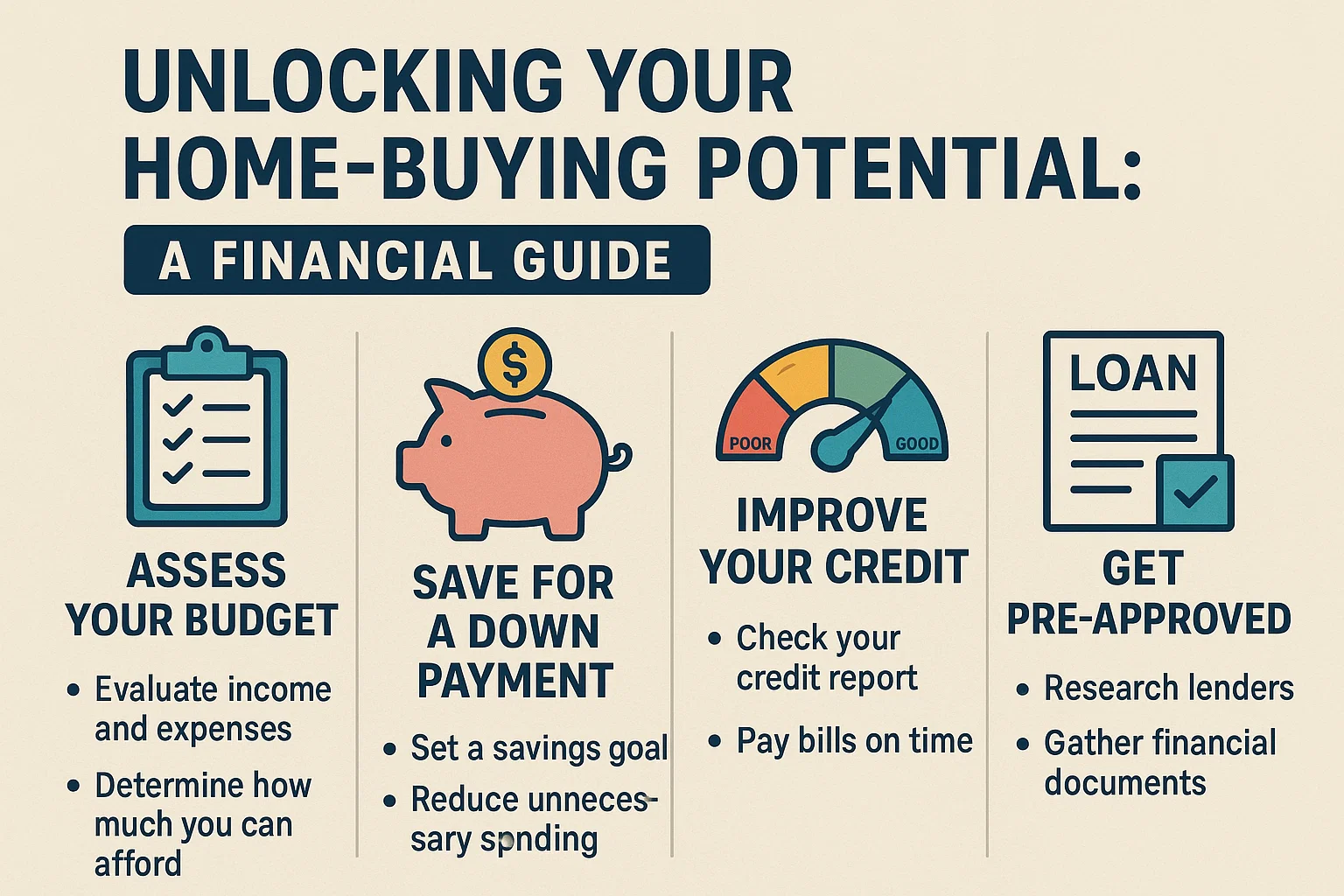

Step 1: Assess Your Financial Health

Your financial stability plays a pivotal role in determining your readiness to buy a home. Before approaching lenders, gather critical documents such as:

- Recent pay stubs

- Bank statements

- Tax returns

Review your credit report thoroughly to identify areas for improvement. Even if your credit score isn’t perfect, upcoming changes to credit reporting standards—or targeted financial adjustments—could boost your eligibility.

Step 2: Calculate the True Cost of Homeownership

A home’s listing price is just the beginning. To gauge affordability, factor in these ongoing expenses:

- Taxes, insurance, and HOA fees

- Maintenance and repairs (3–5% of the home’s value annually)

- Closing costs (2–5% of the home’s value)

- Emergency savings (3–5 months of mortgage payments)

Use online tools to model different budget scenarios, and consult a mortgage professional for a tailored estimate.

Step 3: Analyze Income, Debt, and Loan Terms

Key Questions to Ask:

- What is your total annual income, including secondary sources?

- How do monthly debts (credit cards, loans, etc.) impact your debt-to-income ratio?

- What mortgage term (15 vs. 30 years) aligns with your long-term goals?

- What interest rate are you comfortable accepting?

Step 4: Strengthen Your Financial Profile

Lenders prioritize applicants with stable finances and manageable debt. To improve your standing:

- Aim for a 10–20% down payment to avoid private mortgage insurance (PMI).

- Reduce high-interest debts to lower your debt-to-income ratio.

- Plan for unexpected costs to demonstrate financial preparedness.

Take Action Today

By understanding your financial landscape and preparing strategically, you can confidently pursue your dream home. Start by evaluating your budget, exploring loan options, and seeking expert advice to stay on track.