Understanding Reverse Mortgages: A Comprehensive Guide for Seniors

Understanding Reverse Mortgages: A Comprehensive Guide for Seniors

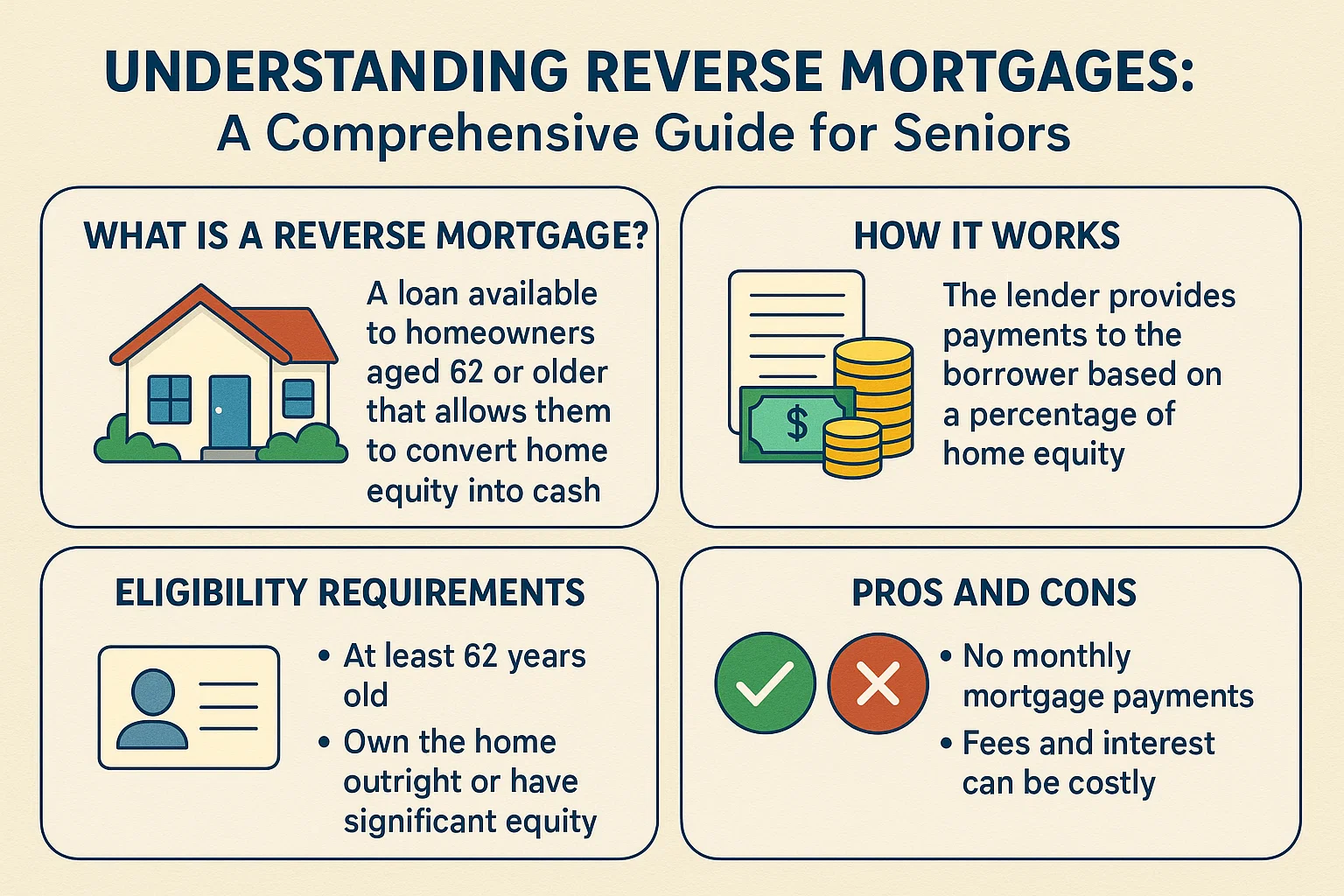

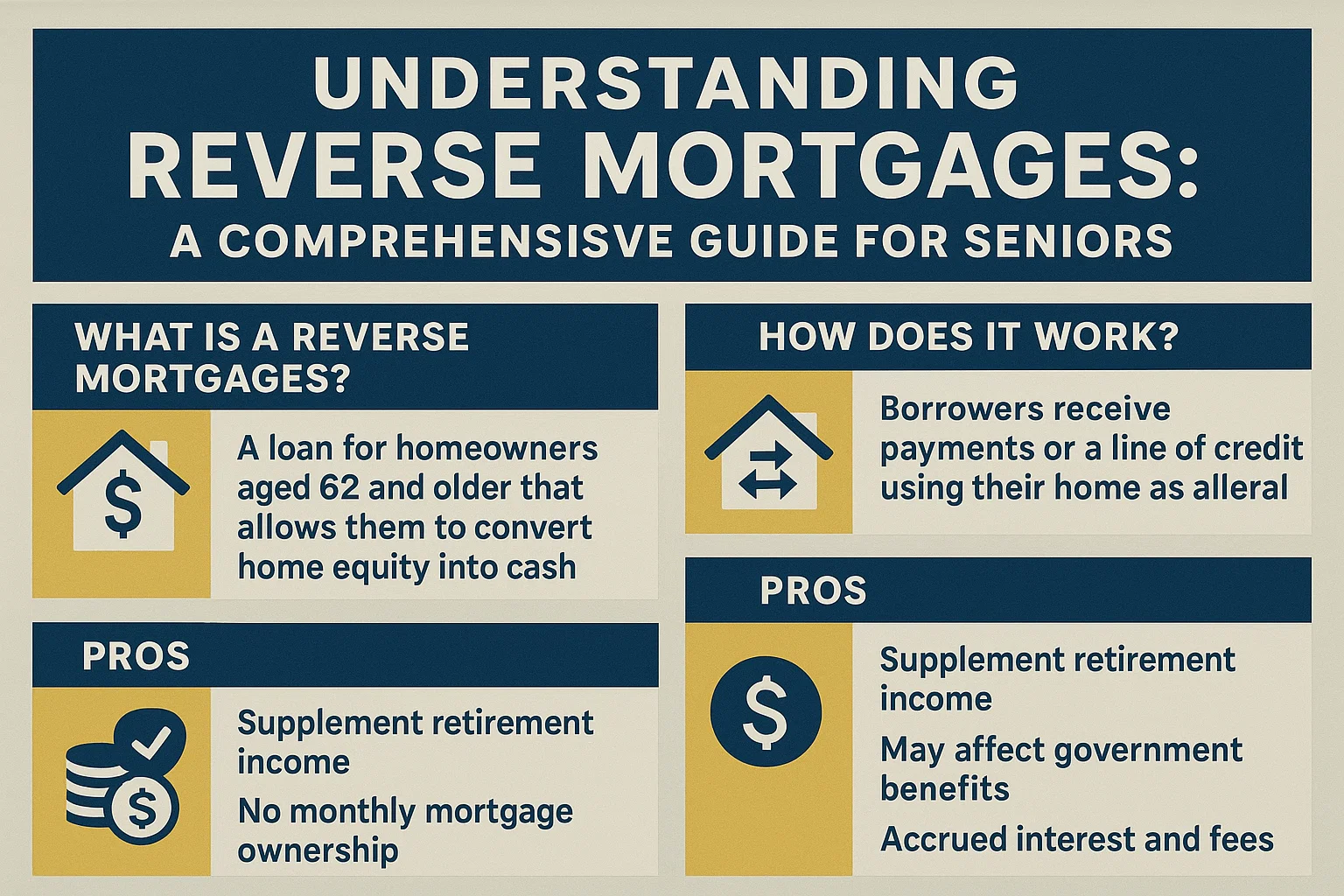

What Is a Reverse Mortgage?

A reverse mortgage allows homeowners aged 62 or older to convert home equity into cash while retaining ownership of their home. Unlike traditional mortgages, the lender pays the borrower, and repayment is deferred until the borrower moves out, sells the home, or passes away.

Key Benefits of a Reverse Mortgage

- Supplement monthly income

- Cover medical expenses or unexpected costs

- Pay off existing debts or mortgages

- Funds can be used flexibly with no restrictions

Eligibility Requirements

To qualify for a reverse mortgage, you must:

- Be at least 62 years old

- Have sufficient home equity (determined by appraisal)

- Meet financial criteria set by HUD

- Reside in an eligible property type (e.g., primary residence)

What If You Don’t Have Enough Equity?

A shortfall in equity doesn’t automatically disqualify you. Borrowers may pay down their existing mortgage balance to meet requirements.

How Much Can You Borrow?

The loan amount depends on:

- Your home’s appraised value

- Current interest rates

- Your age (older borrowers may qualify for larger amounts)

Interest Rates and Costs

Reverse mortgage rates fluctuate daily, similar to traditional mortgages. Your loan officer will work to secure the lowest possible rate. Costs include:

Upfront Costs

- Lender fees

- Mortgage insurance premiums

- Closing costs

Ongoing Costs

- Accrued interest

- Annual mortgage insurance

- Property taxes, homeowners insurance, and maintenance

Family Involvement

Family members are encouraged to participate in discussions with your mortgage loan officer to ensure clarity and address concerns.

Frequently Asked Questions

- How do I start the application process? Begin by consulting a licensed loan officer.

- How is a reverse mortgage different from a traditional mortgage? The lender pays you, and repayment is deferred.

- Can I use the funds for any purpose? Yes, there are no restrictions on fund usage.

- What if I already have a mortgage? You can use reverse mortgage funds to pay off existing loans.