Understanding Mortgage Rate Locks: A Comprehensive Guide

Understanding Mortgage Rate Locks: A Comprehensive Guide

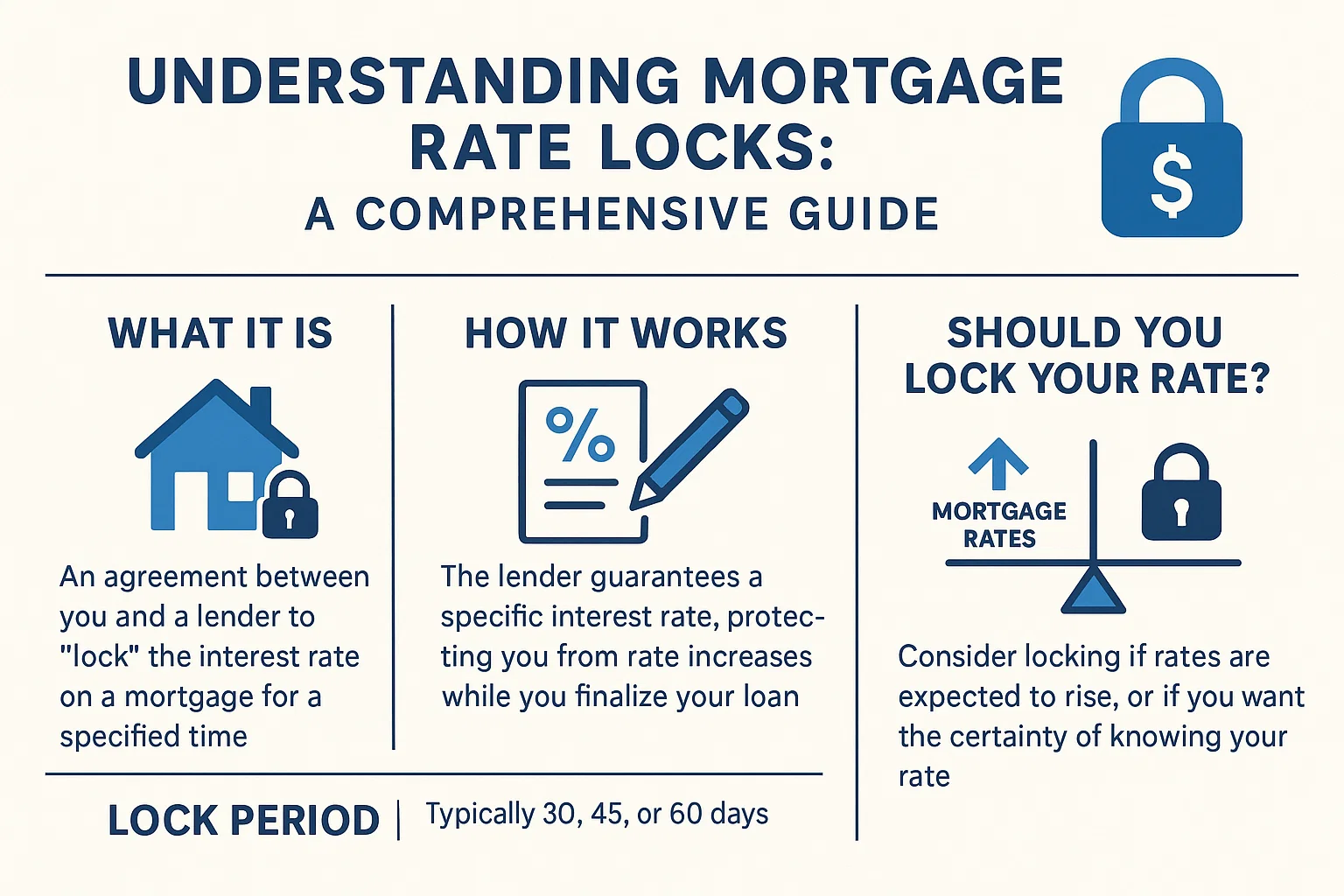

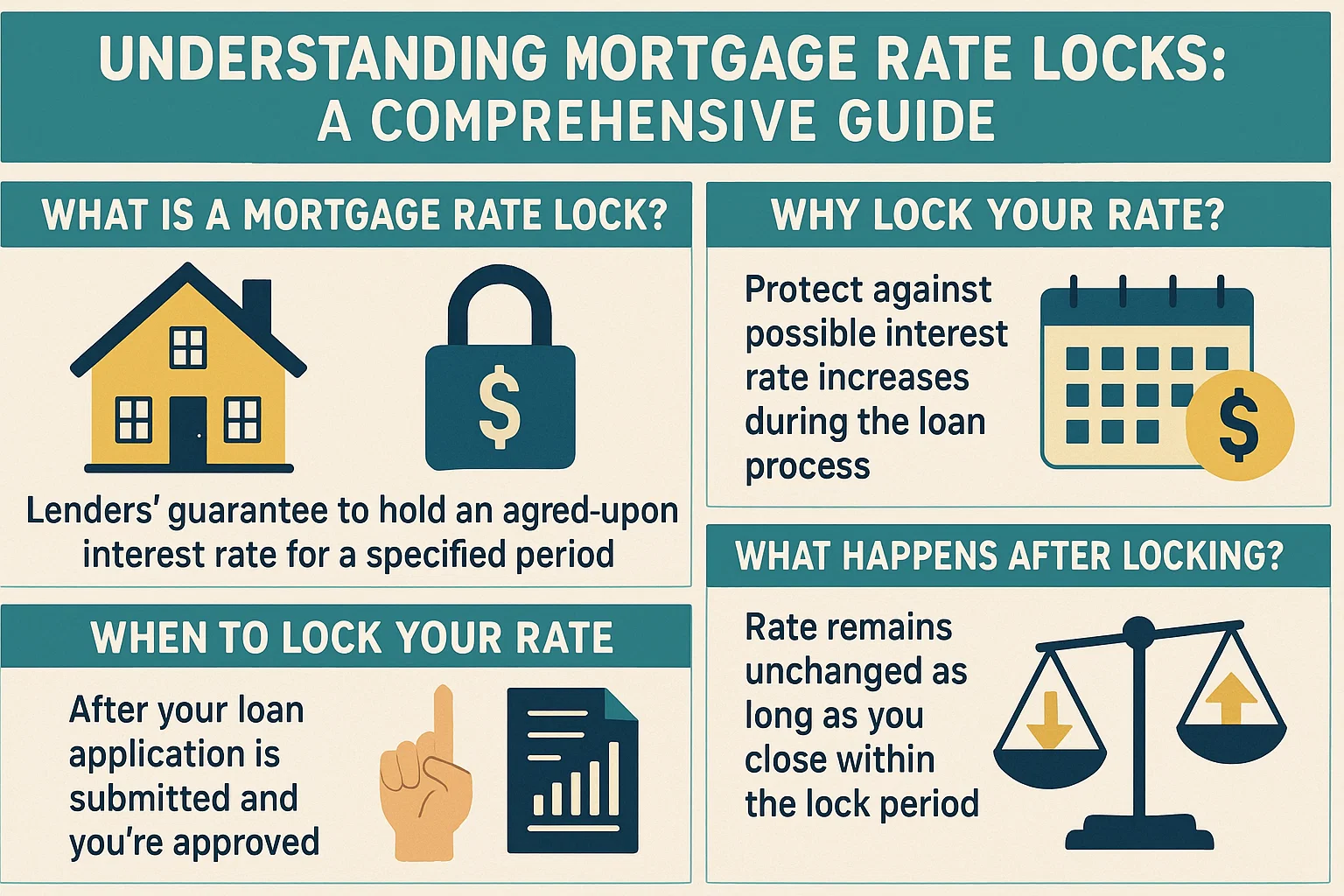

What Is a Mortgage Rate Lock?

A mortgage rate lock is a contractual agreement between a borrower and a lender that guarantees a specific interest rate for a predetermined period. This protects borrowers from market rate increases during the homebuying process. If rates rise after locking, the borrower retains the agreed-upon rate. However, if rates fall, some lenders offer “float-down” options to adjust the rate downward (more on this later).

How Does a Mortgage Interest Rate Lock Work?

When you lock your rate, you secure the current interest rate and loan terms by paying a fee. The rate remains fixed as long as your loan application details (e.g., credit score, down payment, or loan amount) stay unchanged. Locks typically expire after 30–60 days, though longer terms may be available for new construction purchases.

When Should You Lock Your Mortgage Rate?

Timing depends on market conditions and your closing timeline. Key considerations:

- Market Trends: Lock early if rates are rising.

- Closing Timeline: Ensure the lock period covers your expected closing date.

- New Construction: Longer locks (up to 364 days) may be negotiated.

Costs and Duration of Rate Locks

How Much Does It Cost?

Fees vary by lender, loan size, and lock duration. Costs typically range from 0.25% to 0.50% of the loan amount. Longer locks often incur higher fees.

How Long Can You Lock a Rate?

Standard locks last 30–60 days. For new construction, locks up to 364 days may be available to account for potential delays.

Expired Locks and Extensions

If your lock expires before closing, you can:

- Pay to Extend: Average extension fees cost ~0.45% of the loan amount.

- Let It Expire: Accept the current market rate at closing.

The “Float-Down” Option

Some lenders allow a one-time rate reduction if market rates drop during the lock period. Float-down terms vary, so clarify eligibility and fees with your lender.

Pros and Cons of Rate Locks

Pros

- Protection against rising rates

- Predictable monthly payments

Cons

- Potential extension fees for delays

- Missed savings if rates drop (without a float-down)

Is a Rate Lock Worth It?

For risk-averse borrowers, yes. A lock provides stability amid market volatility. Evaluate fees, lock duration, and float-down options to decide.

Mortgage Rate Lock FAQs

- How often do rates change? Daily or even hourly.

- Can you lock without a contract? No—a signed agreement is required.

- Does pre-approval lock your rate? No. Locks occur after loan approval.

- Can a lender change a locked rate? Only if your loan terms change (e.g., credit score, down payment).