Understanding Mortgage Pre-Qualification vs. Pre-Approval: A Homebuyer’s Guide

Understanding Mortgage Pre-Qualification vs. Pre-Approval: A Homebuyer’s Guide

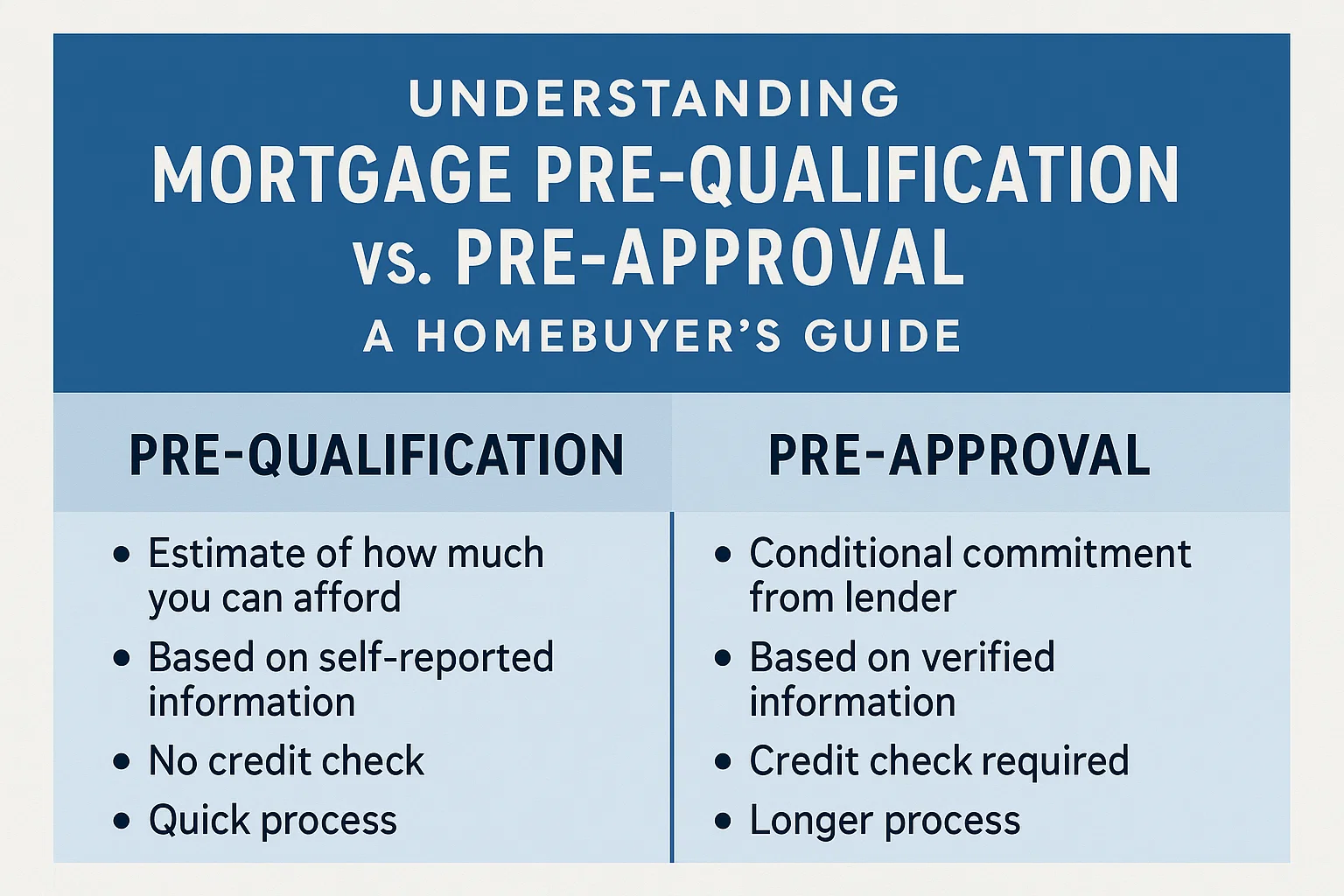

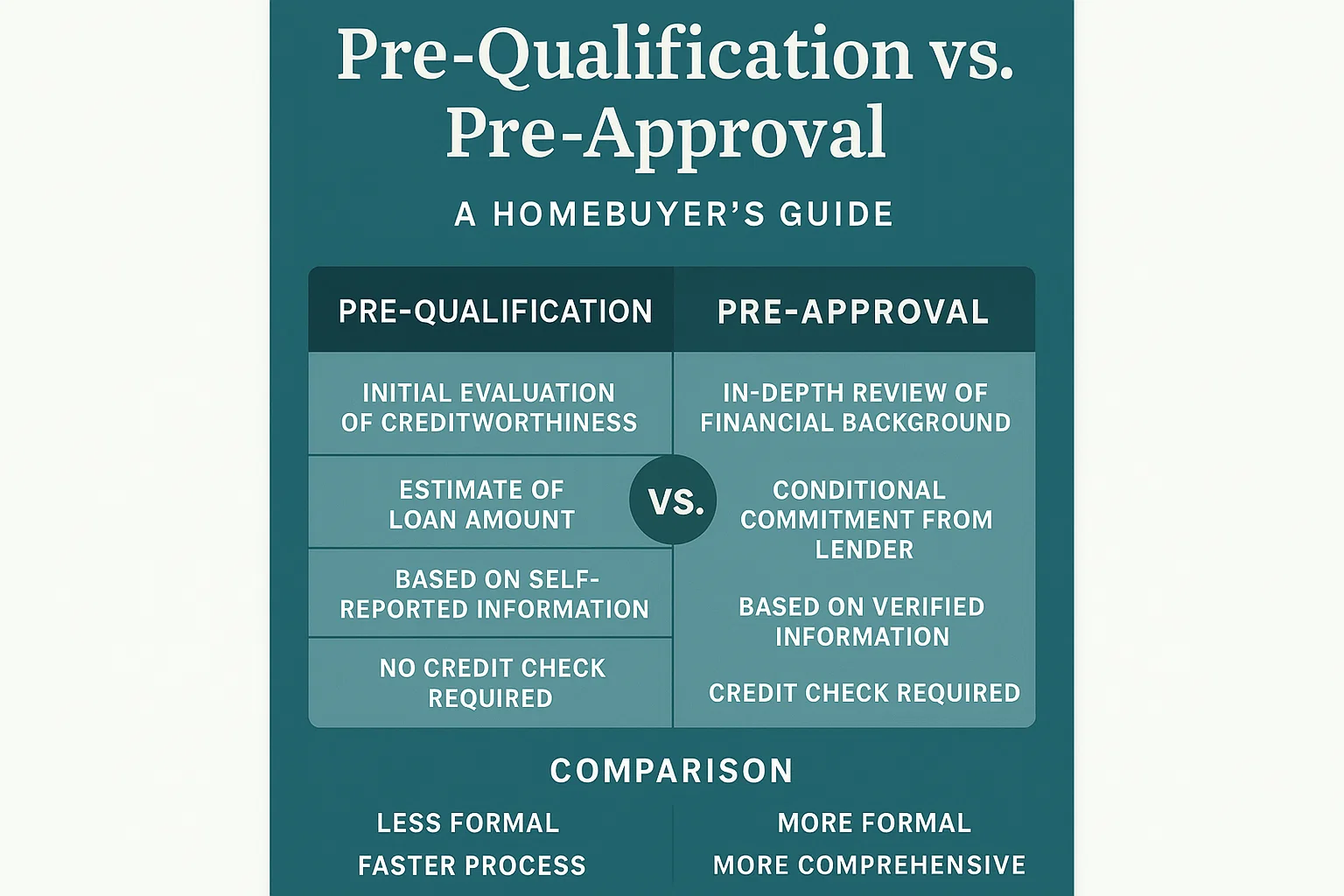

What Is Mortgage Pre-Qualification?

Mortgage pre-qualification is an optional step that provides a rough estimate of how much you might borrow based on self-reported financial details. It’s a useful starting point for first-time buyers or those with recent financial changes, but it holds no formal weight in the homebuying process. Here’s what you need to know:

- Involves a soft credit check (no impact on credit score).

- Offers general estimates for loan amounts and interest rates.

- Helps gauge readiness to buy a home but doesn’t guarantee lender approval.

Pre-qualification is ideal for early planning but won’t strengthen your offer when negotiating with sellers.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is a lender-verified commitment that strengthens your position as a serious buyer. It involves a thorough review of your finances and creditworthiness, resulting in a conditional offer for a specific loan amount. Key details include:

- Requires a hard credit check (temporarily affects credit score).

- Provides a formal pre-approval letter valid for 90 days.

- Demonstrates financial credibility to sellers, improving offer competitiveness.

Pre-approval is essential when you’re ready to make offers, as it signals your ability to secure financing.

Pre-Qualification vs. Pre-Approval: Which Should You Choose?

Your choice depends on your homebuying stage:

When to Choose Pre-Qualification:

- Pros: Quick process, no documentation, estimates budget range.

- Cons: Non-binding, lacks credit analysis, insufficient for offers.

When to Choose Pre-Approval:

- Pros: Lender-backed offer, strengthens negotiations, clarifies budget.

- Cons: Requires detailed paperwork, longer processing time.

Required Documentation

For Pre-Qualification:

- Basic income and employment details.

- Estimated down payment and desired loan amount.

- Permission for a soft credit inquiry.

For Pre-Approval:

- Recent pay stubs, tax returns, and bank statements.

- Proof of assets and down payment funds.

- Permission for a hard credit check.

Final Tips for Homebuyers

Use pre-qualification to set realistic expectations early in your search. Opt for pre-approval once you’re serious about making offers. Both steps streamline your journey, but only pre-approval carries weight in competitive markets. Always consult lenders to clarify terms and ensure alignment with your financial goals.