Understanding Home Appraisals: Loan Approval vs. Property Taxes

Understanding Home Appraisals: Loan Approval vs. Property Taxes

If you are in the market to buy, or you recently purchased a new home, chances are you have heard of an appraisal, most likely from your mortgage lender. Simply put, an appraisal is a valuation of property, and an appraised value is an estimation of a property’s value at a given point in time.

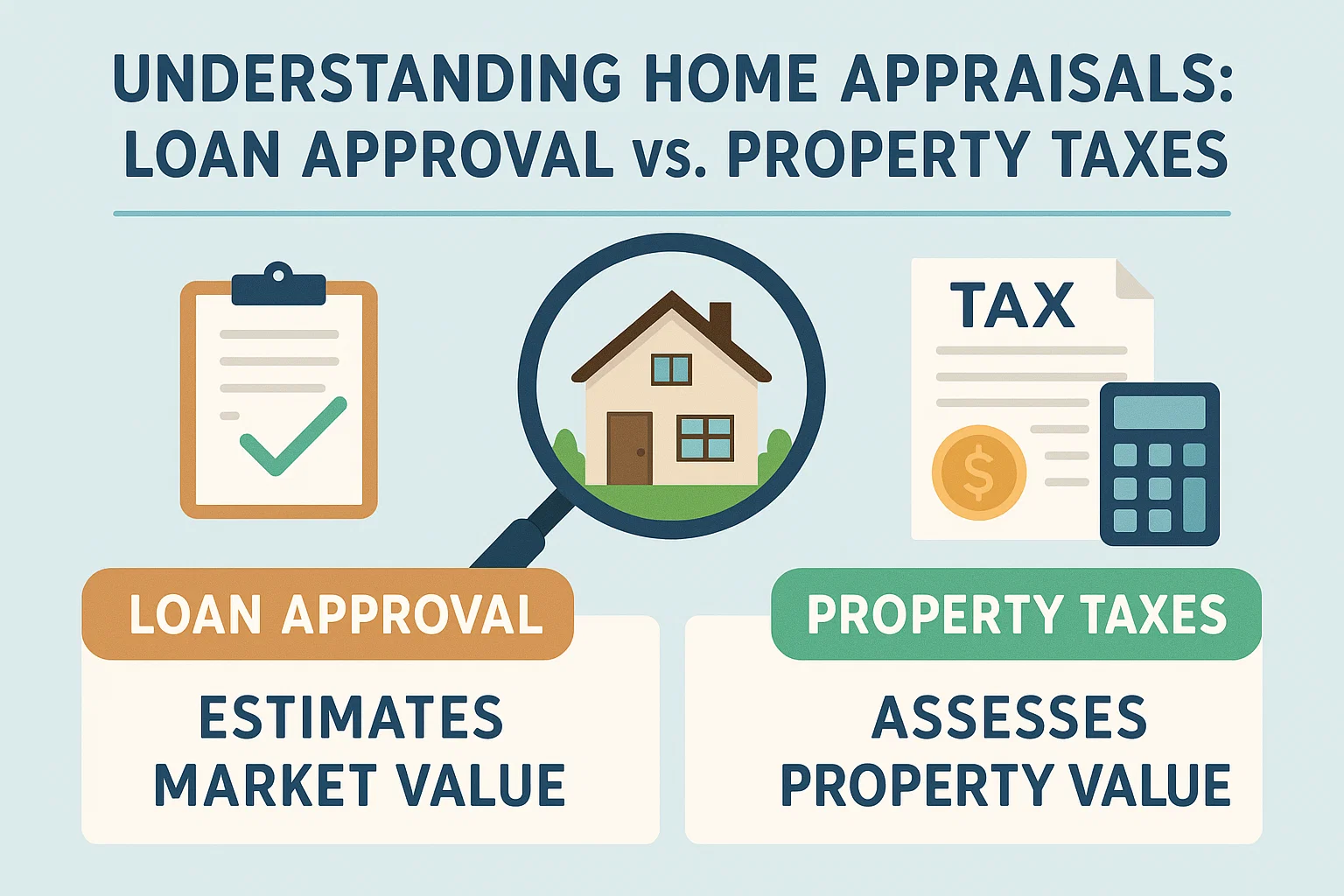

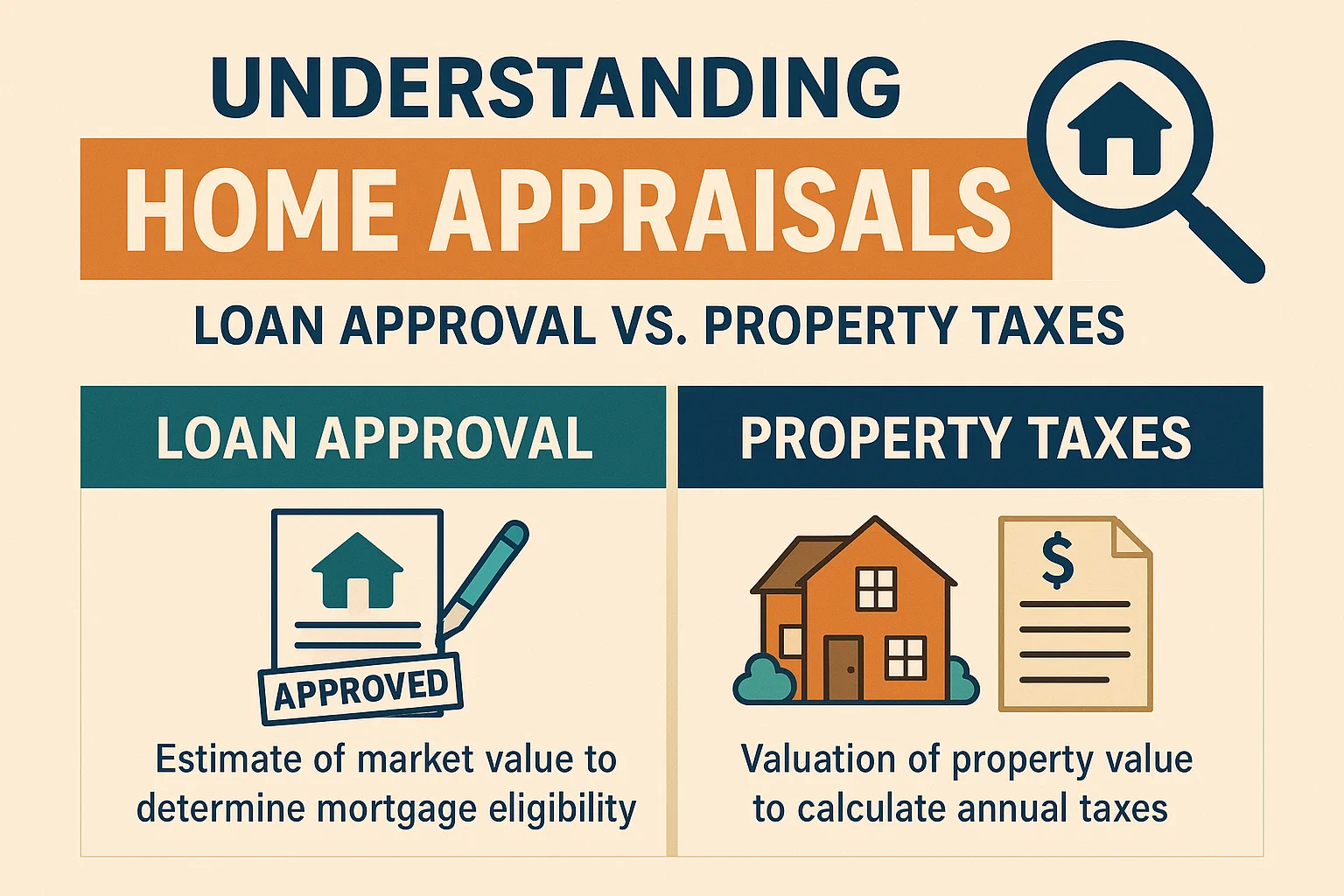

There are actually two appraisals involved in the homebuying process: the first is for the purpose of securing your loan prior to your purchase, and the second is used by the local taxing authority to determine how much you will pay in property taxes – this is often called a “tax assessment.”

What is the Appraisal in a Home Purchase?

For most, a home purchase requires taking out a mortgage with a bank or other lending institution. The lender wants to protect its investment, so it typically orders an appraisal of the property to determine if it is worth at least the amount the buyer is asking to borrow. This is important because, should you enter a mortgage agreement, your new home serves as collateral for the loan.

The cost of this appraisal varies and usually comes out of your own pocket. This charge will likely appear in your closing costs. While it may seem an inconvenient expense, appraisals can actually afford you security and even leverage. As a buyer taking on the expense of a home, you should want to feel certain that you are paying a fair price.

Appraisals can reveal if the property is worth less than the seller’s asking price. In that case, you can either walk away and save your money (as long as you have an appraisal contingency), or you can try to renegotiate the price with the seller.

How Appraisers Determine Property Value

Appraisers start by visiting the home to evaluate its condition and quality of construction. The appraiser will look over the exterior and interior of the home, noting its square footage, number of bedrooms and baths, homesite size, parking, and zoning. They mark up any issues and special features that respectively detract and add value to the home’s market price.

Other factors in the valuation include the home’s age, curb appeal, and recent repairs and improvements. Anything that is not affixed to the property, like décor and furniture, is not considered.

In addition to their visit, the appraiser researches the neighborhood and surrounding area. They pay attention to local issues and proximity to schools, hospitals, and amenities. More importantly though, the appraiser should review current market trends and comparable properties that are very similar to the home they are appraising.

Typically, the appraiser’s report will be available in less than a week. If they estimate the home is not worth the asking price, but you still wish to pursue the sale, your lender will probably lend no more than the appraised value.

What is the Appraisal for Property Taxes?

One of the responsibilities as a homeowner is paying property taxes. The county or other jurisdiction in which your property is located will issue an appraisal (sometimes called a “tax assessment”) of your home to determine its tax assessed value. That value is then used by local taxing authorities to determine what you will pay in property taxes.

This type of appraisal can occur annually or every three to five years. In addition to periodic assessments, most jurisdictions will reassess a property at the time of sale. Many jurisdictions use one of three approaches to assess a property: (1) sales comparison approach, (2) income approach, and (3) cost approach.

The Sales Comparison Approach

Similar to the appraisal for a home purchase, under the sales comparison approach, the appraiser identifies comparable properties similar to your own that sold in the last six to twelve months and are located in the same geographic area. They compare the age, size, condition, and quality of construction, and note any known repairs or improvements, before estimating your property’s market value.

Depending on where you live, the market value may not be the same as the tax assessed value. Some states use 100% of the market value to determine how much a homeowner will pay in property taxes. Other states use an assessment rate that is a percentage of the market value.

One issue with this type of appraisal is the appraiser frequently does not visit your home or the comparable properties to complete their assessment. Instead, they often pull information from online listings, which can introduce the possibility of mistakes. If you believe your property has not been properly assessed, you may have the opportunity to protest the tax assessed value of your home.

Conclusion

Understanding the difference between these two types of appraisals can help you navigate the homebuying process and manage your ongoing property tax obligations. Be sure to consult with professionals for advice specific to your situation.