Understanding FICO Scores: Your Key to Better Credit Opportunities

Understanding FICO Scores: Your Key to Better Credit Opportunities

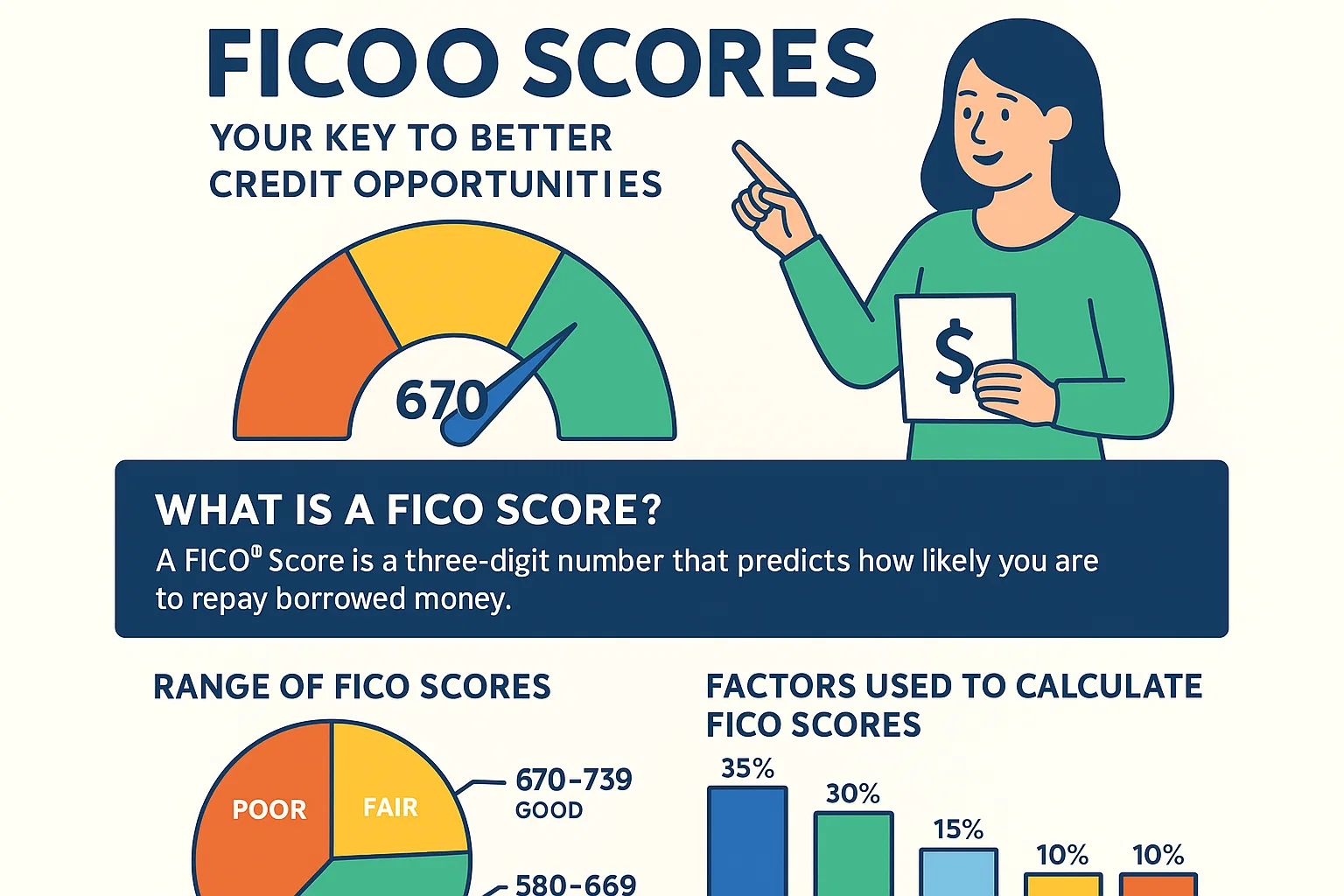

FICO scores play a pivotal role in 90% of credit decisions, helping lenders assess your credit risk and determine loan approvals, interest rates, and terms. Your score, combined with your financial circumstances (income, employment) and the type of credit you seek, shapes lenders’ decisions. Below, we break down how FICO scores work and what they mean for your financial future.

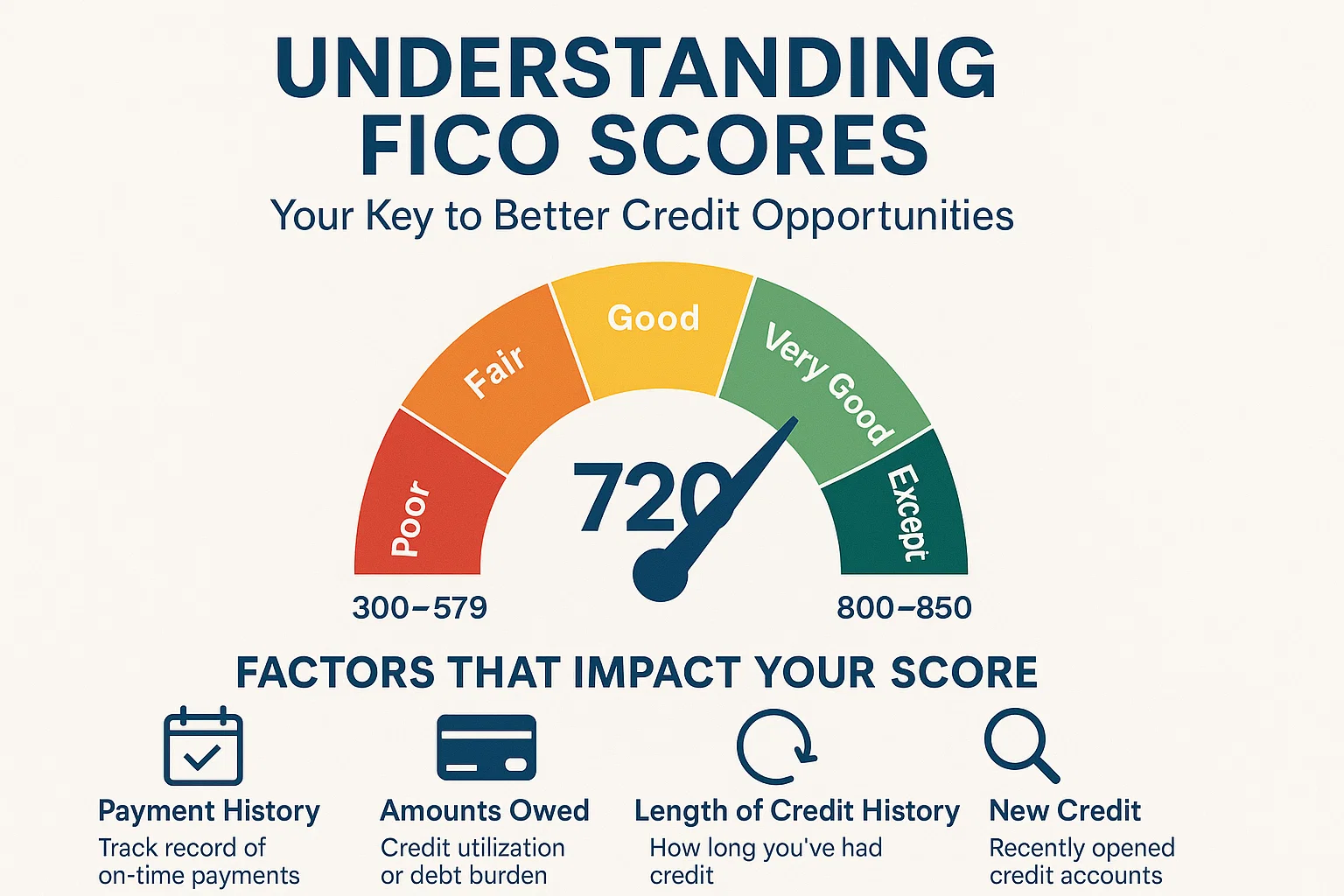

Key Factors Influencing Your FICO Score

- Payment History (35%): Tracks timely payments and delinquencies.

- Amounts Owed (30%): Reflects your credit utilization ratio.

- Length of Credit History (15%): Considers the age of your accounts.

- New Credit (10%): Includes recent credit inquiries or accounts.

- Credit Mix (10%): Evaluates diversity in credit types (e.g., loans, credit cards).

FICO Score Ranges and Their Implications

Scores range from 300 to 850. Higher scores unlock better terms, while lower scores may lead to rejections or costly fees. Here’s what each range means:

Exceptional (800+)

Borrowers in this range enjoy streamlined approvals and the most competitive rates. Likelihood of delinquent payments: ~1%.

Very Good (740–799)

Qualify for favorable interest rates with strong approval odds. Likelihood of delinquent payments: ~2%.

Good (670–739)

Considered “acceptable” borrowers but may not receive the best rates. Likelihood of delinquent payments: ~8%.

Fair (580–669)

May face higher interest rates or subprime labels. Likelihood of delinquent payments: ~28%.

Poor (579 or below)

Risk rejection or additional fees when applying for credit. Likelihood of delinquent payments: ~61%.

Why Your FICO Score Matters

Your FICO score is a cornerstone of your financial profile. While lenders also evaluate income and debt, a strong score opens doors to better opportunities. Start by reviewing your current score and addressing weaknesses—whether paying down balances, avoiding late payments, or limiting new credit applications. Small improvements can save thousands over time.

*Delinquent payment likelihoods are approximate and based on historical data.