Understanding FHA Loans: Key Benefits and Considerations

Understanding FHA Loans: Key Benefits and Considerations

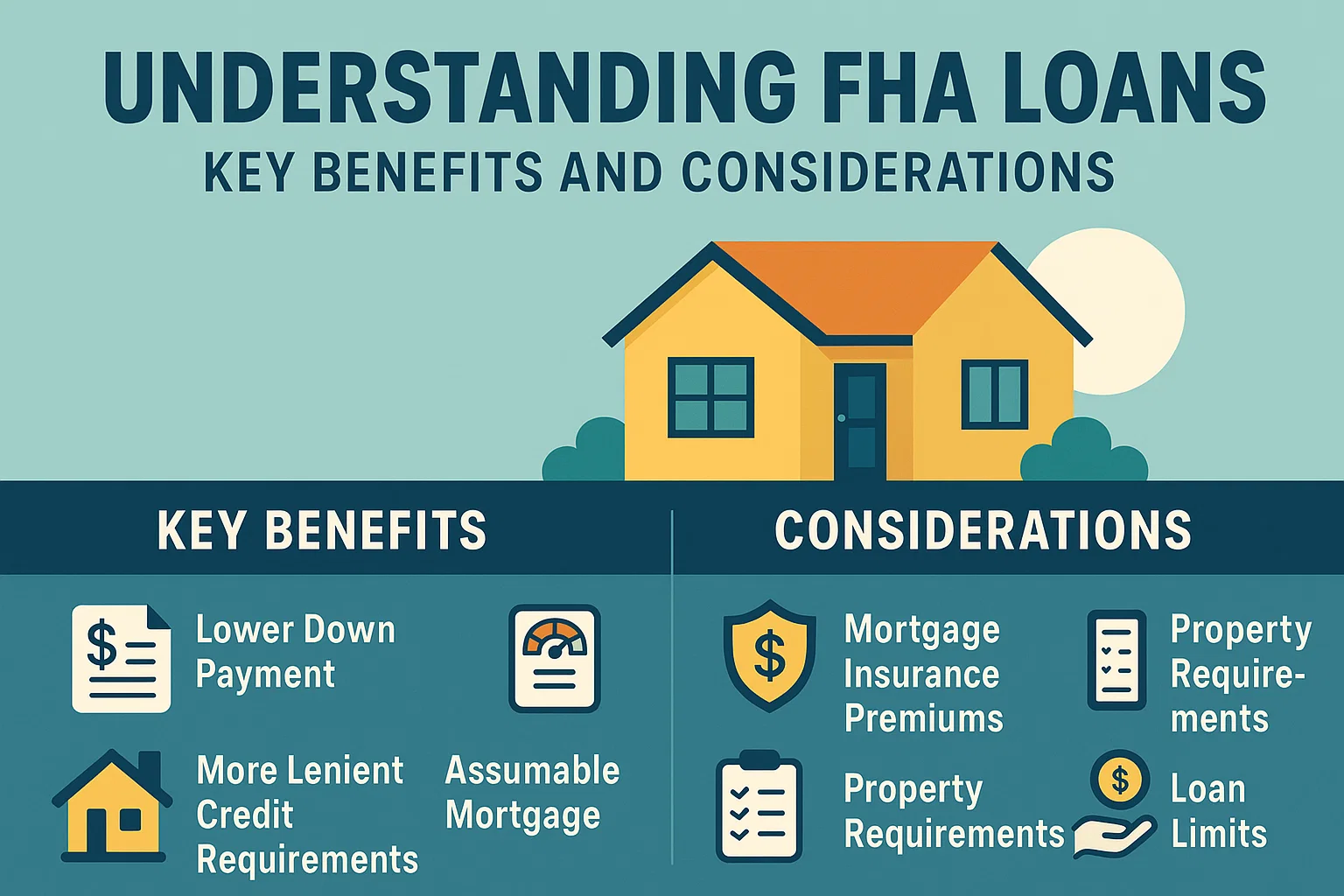

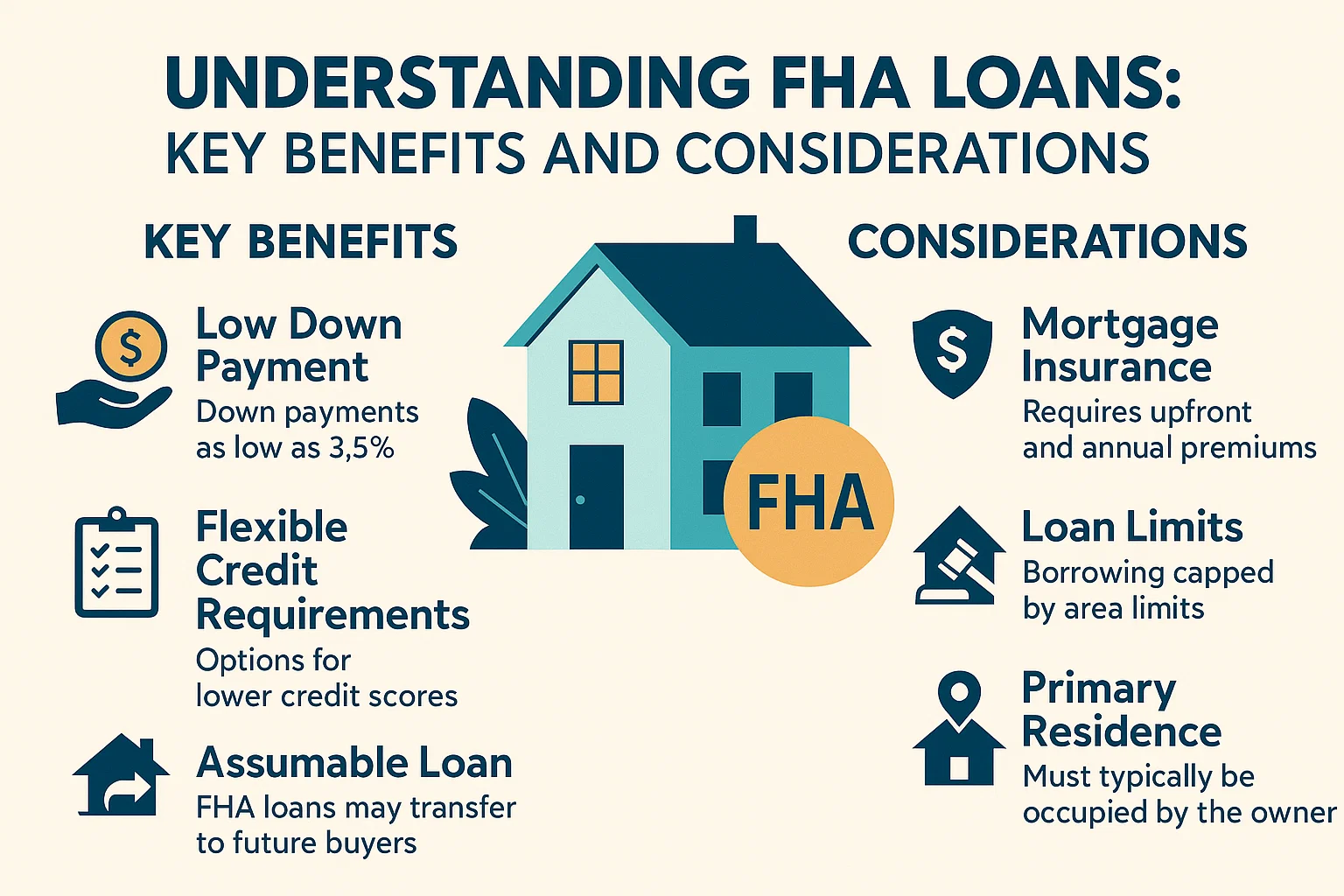

What Are FHA Loans?

Insured by the Federal Housing Administration (FHA), FHA loans are designed to help homebuyers, including first-time buyers, repeat purchasers, and those looking to refinance existing mortgages. These loans stand out for their accessible requirements and unique advantages.

Benefits of FHA Loans

- Lower Down Payment: FHA loans require as little as 3.5% down, compared to conventional loans that may demand up to 20%.

- Reduced Closing Costs: Borrowers often benefit from lower upfront fees compared to traditional mortgage options.

- Flexible Qualifications: Credit score requirements are generally more lenient, making homeownership accessible to a broader range of applicants.

Potential Drawbacks to Consider

- Mortgage Insurance Requirements: Depending on the loan-to-value ratio (LTV), FHA borrowers may be required to pay mortgage insurance for the entire loan term. In contrast, conventional loans typically remove this requirement once the borrower reaches 20% equity in the property.

- Loan Limits: FHA loans are subject to regional borrowing caps, which may restrict options for higher-priced homes.

FHA vs. Conventional Loans

While conventional loans often appeal to borrowers with strong credit or larger down payments, FHA loans provide a valuable alternative for those prioritizing affordability and flexibility. The choice ultimately depends on individual financial circumstances and long-term goals.