Understanding Credit Scores for Homebuyers

Understanding Credit Scores for Homebuyers

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Consult a qualified professional for guidance on credit scores and loans.

Do You Need a Perfect Credit Score to Buy a Home?

It depends on what you mean by “perfect.” The highest possible credit score is 850, but achieving that number is nearly impossible—and unnecessary. Lenders do not require a perfect score for loan approval. Instead of aiming for perfection, ask: Do I need a high credit score to buy a home? The answer is no.

However, lenders do consider your credit score because it reflects your reliability as a borrower. A higher score can improve loan terms, including down payment requirements and interest rates. A low credit score doesn’t necessarily disqualify you from getting a loan—certain loan programs accommodate lower scores.

Why Does Your Credit Score Matter?

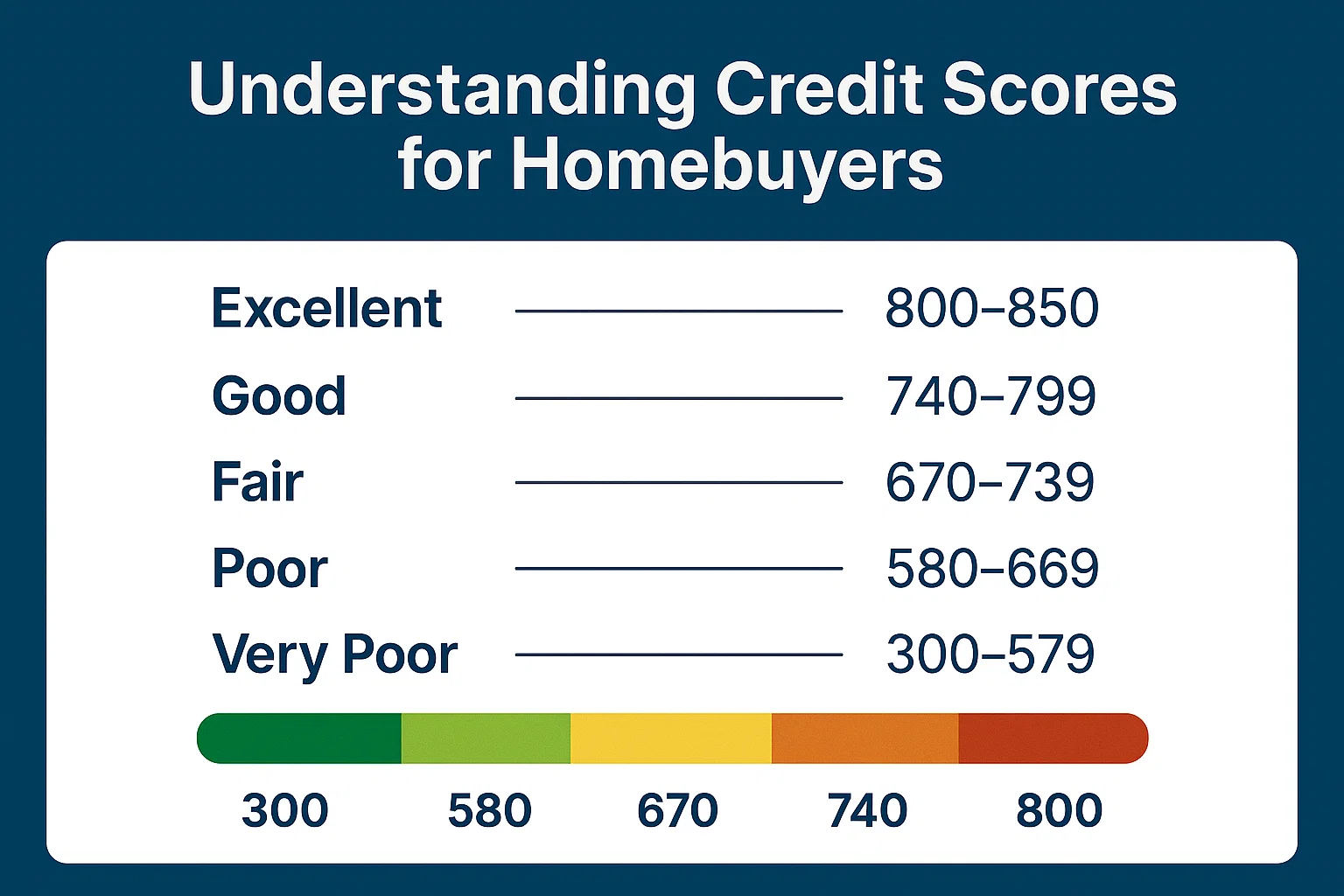

Your credit score is a three-digit number (ranging from 300 to 850) that evaluates your creditworthiness. It helps lenders assess the risk of lending to you based on factors such as:

- Payment history

- Credit utilization

- Length of credit history

- Recent credit inquiries

- Derogatory marks (e.g., late payments, bankruptcies)

A higher credit score indicates lower risk to lenders, making loan approval easier. A lower score may still qualify you for a loan, but with stricter conditions:

- Larger down payment – Reduces the lender’s risk by lowering the loan-to-value ratio.

- Higher interest rate – Increases the lender’s return to offset potential risk.

These conditions can make homeownership more expensive, so improving your credit score before applying for a loan is beneficial.

Loan Options for Different Credit Scores

Loan requirements vary by lender and location, but here’s a general overview of credit score expectations for common loan types:

Jumbo Loans

Minimum credit score: 700+

Used for luxury homes exceeding standard loan limits.

USDA Loans

Minimum credit score: 640+

Designed for rural and suburban homebuyers.

Conventional Loans

Minimum credit score: 620-680

Must meet Fannie Mae and Freddie Mac guidelines. A higher score may avoid private mortgage insurance (PMI).

VA Loans

Minimum credit score: 580-620

Available to military service members, veterans, and eligible spouses.

FHA Loans

Minimum credit score: 500-580

Government-backed loans with flexible credit requirements. Lower scores require a larger down payment.

Each loan type has unique qualifications, so consulting a loan professional is recommended.

How to Improve Your Credit Score

Rebuilding credit takes time—often six months to a year—but these steps can help:

Check Your Credit Report

Request a free annual report and dispute any errors. Monitoring your report can also detect identity theft.

Understand Credit Score Factors

FICO scores (commonly used by lenders) are calculated based on:

- Payment history (35%)

- Amount owed (30%)

- Length of credit history (15%)

- New credit applications (10%)

- Credit mix (10%)

Building or Repairing Credit

For new credit users:

- Open a credit account (e.g., secured card).

- Make small, manageable charges.

- Avoid maxing out credit lines.

- Pay bills on time.

- Space out credit applications.

For credit repair:

- Pay bills on time.

- Reduce outstanding debt.

- Keep credit balances low.

- Avoid opening new accounts.

- Keep old accounts open (if no fees apply).

Negative marks (late payments, bankruptcies) may take 7-10 years to disappear from your report.

Final Thoughts

You don’t need a high credit score to buy a home, but a better score can lead to more favorable loan terms. If you have time, improving your credit before applying can save money in the long run. For personalized advice, consult a financial or credit expert.