Understanding Conventional Mortgage Loans: Key Features and Benefits

Understanding Conventional Mortgage Loans: Key Features and Benefits

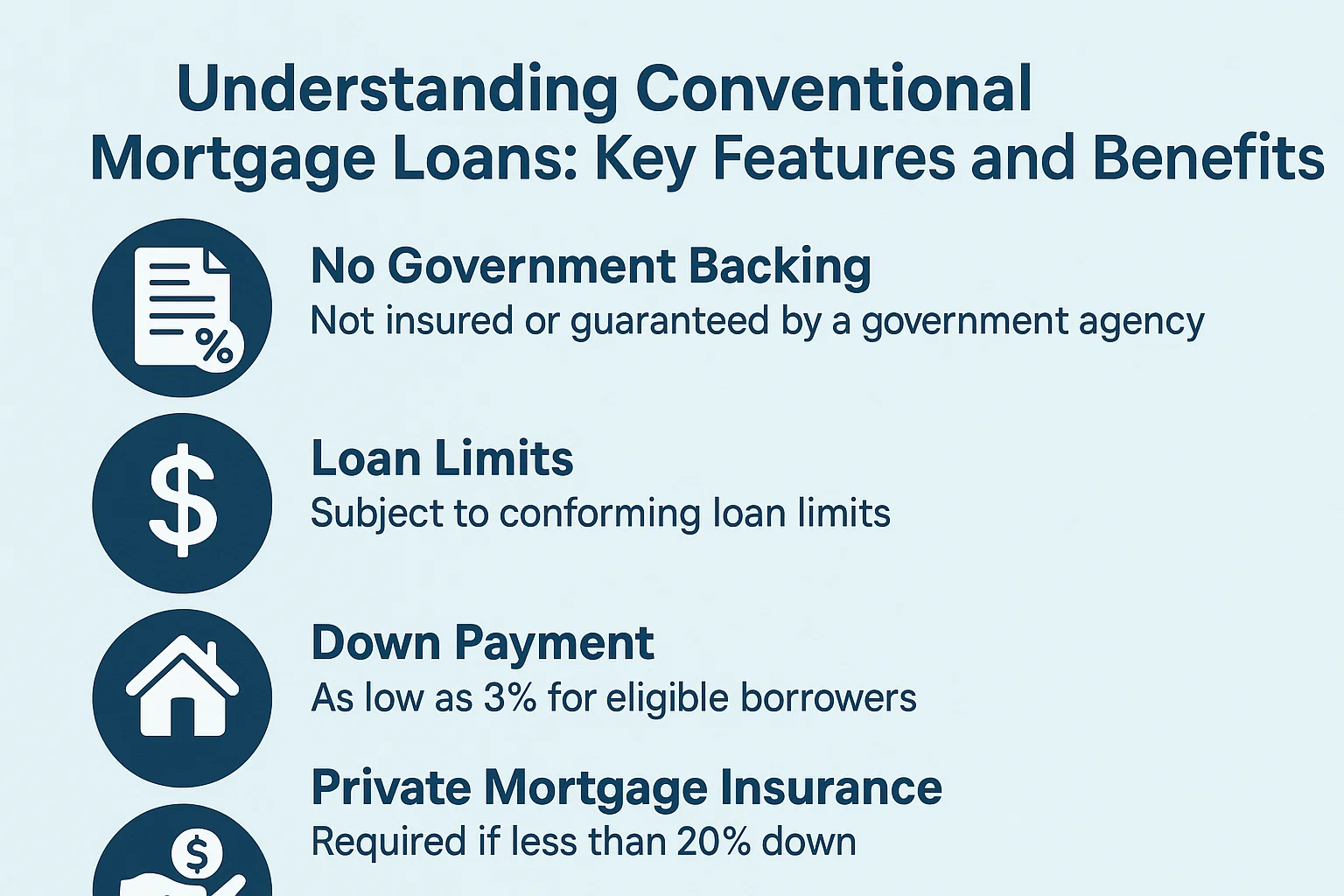

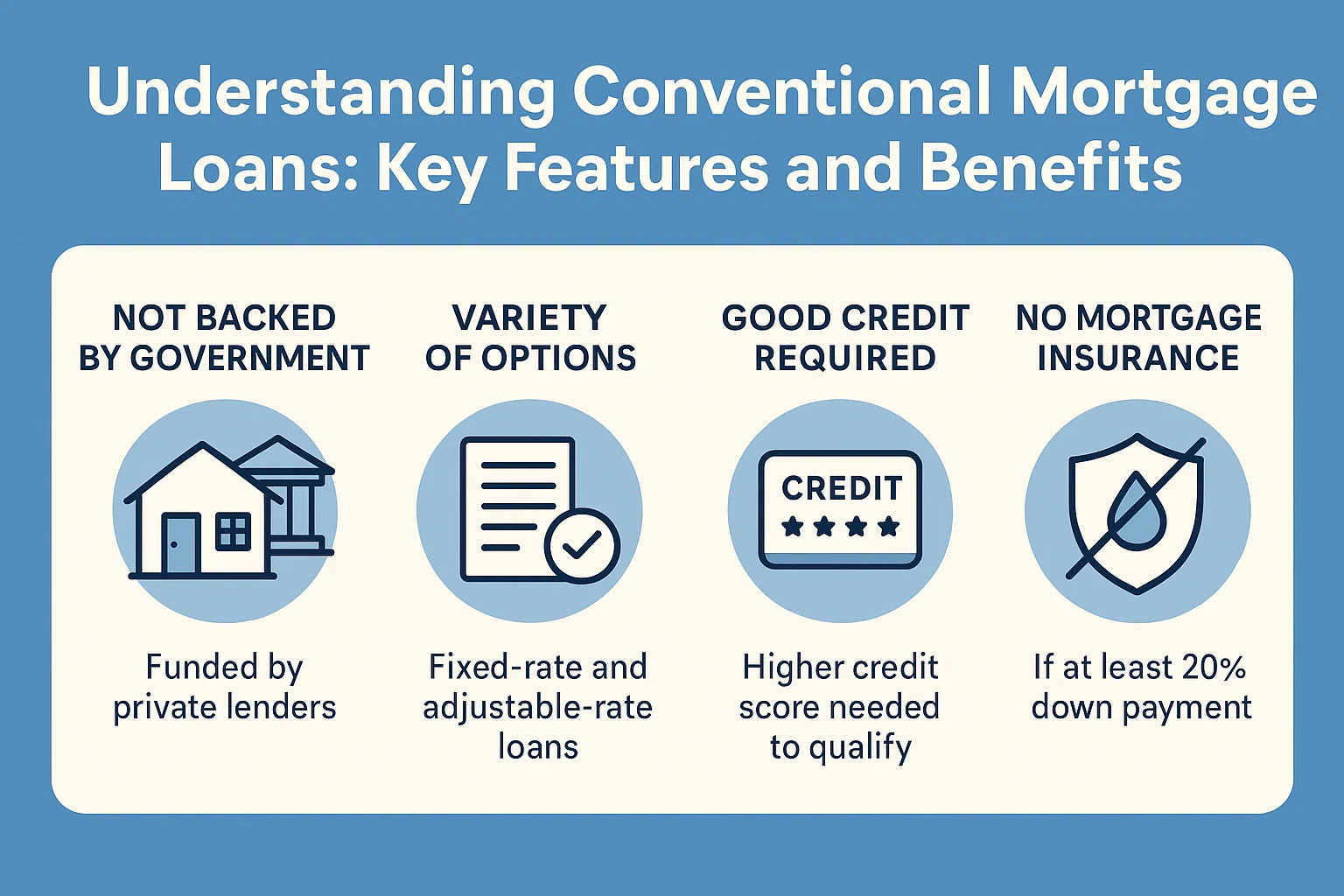

A conventional mortgage loan is a type of generic home loan not backed by government agencies like the FHA, USDA, or VA. These loans are offered by private lenders and provide greater flexibility in terms of structure and eligibility requirements.

Types of Conventional Mortgages

Conforming Loans

Conforming loans adhere to guidelines set by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. Key characteristics include:

- Eligibility for purchase by GSEs, which helps lenders free up capital to issue more loans.

- Loan amounts must fall under government-mandated caps.

- Borrowers typically need a higher credit score compared to government-backed loans (e.g., FHA or VA loans).

Non-Conforming Loans (Jumbo Loans)

Non-conforming loans exceed conforming loan limits and often require stricter qualifications. Features include:

- Higher loan amounts, ideal for luxury or high-cost properties.

- More rigorous approval criteria, such as higher credit scores and larger down payments.

- Increased lender risk due to the larger loan size.

Advantages of Conventional Loans

- Flexibility: Available through numerous lenders with varying terms.

- Competitive Rates: Often offer lower interest rates for borrowers with strong credit.

- No Government Restrictions: Avoid mandatory mortgage insurance in some cases, unlike FHA loans.

Conclusion

Conventional mortgages provide versatile options for homebuyers, whether through conforming loans with standardized terms or jumbo loans for higher-value purchases. Borrowers should evaluate their financial standing and compare loan types to determine the best fit for their needs.