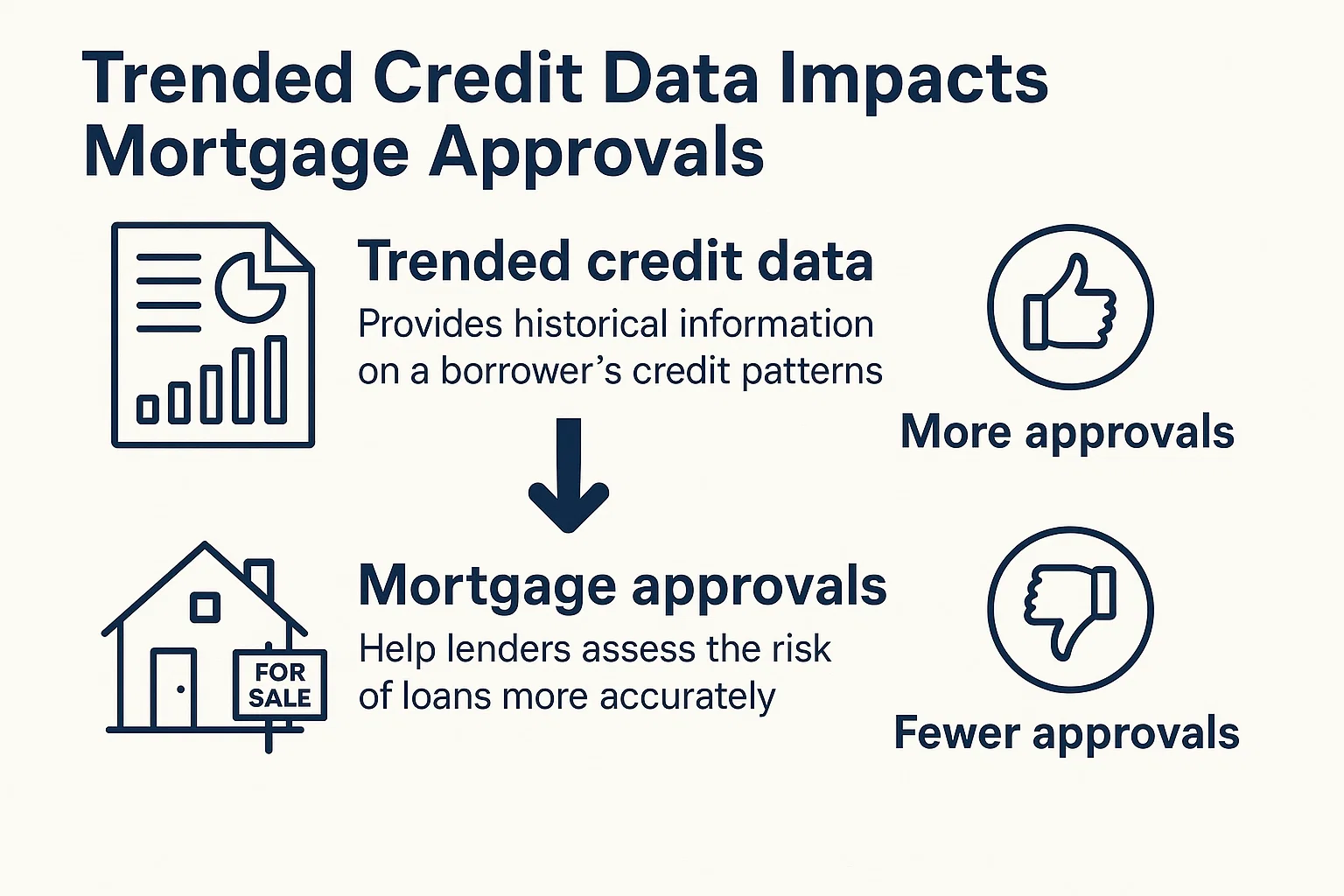

Trended Credit Data Impacts Mortgage Approvals

Tightened Credit Standards and Trended Data: Navigating Mortgage Approvals in a Post-Crisis Market

In the wake of the housing crisis, stricter credit standards have created hurdles for homebuyers with the financial capacity to purchase or build homes but face challenges securing mortgage approvals. Recent adjustments to mortgage programs aim to expand accessibility through lower down payments and alternative credit evaluations. Among these innovations, Fannie Mae has updated its underwriting software to incorporate trended credit data, offering lenders deeper insights into borrower behavior over time.

What is Trended Credit Data?

Unlike traditional credit reports—which provide a static snapshot of a borrower’s credit profile—trended credit data analyzes 24 months of credit card usage. This approach identifies patterns, such as consistent debt reduction or accumulation. For example, a traditional report might show a high credit card balance on the day it’s pulled, even if the borrower intends to pay it off before the due date. Trended data, however, reveals whether a borrower habitually pays balances in full or carries debt month-to-month.

“The intent of using trended credit data is to allow more access to credit for people who have been blocked,” explains Rick Sharga, chief marketing officer of Ten-X, an online real estate marketplace.

Transactors vs. Revolvers: How Borrowers Are Categorized

Fannie Mae’s system categorizes applicants into two groups:

- Transactors: Borrowers who pay credit card balances in full or significantly above the minimum each month.

- Revolvers: Borrowers who carry balances and make only minimum payments.

“Transactors are considered a better credit risk because they lower their credit utilization ratio,” says Kelli Yarbrough, vice president of loan retention at RoundPoint Mortgage Servicing Corporation. “Revolvers may signal financial strain, as carrying balances suggests limited liquidity.”

Potential Impact on Loan Approvals

While trended data could highlight responsible financial behavior obscured by a one-time credit misstep, experts caution that its immediate impact may be limited. Mark Dietz, senior vice president at EagleBank, notes that lenders still prioritize credit scores and loan-to-value ratios. Sharga adds, “In today’s risk-averse climate, this data might tip the scales against borderline applicants rather than expanding approvals.”

Tips for Strengthening Your Credit Profile

- Pay more than the minimum due on credit cards to reduce balances faster.

- Keep credit utilization below 30% of your limit to boost scores over time.

- Explore low down payment programs or builder incentives to free up cash for debt reduction.

- Consider portfolio lenders (those retaining loans in-house) for greater flexibility on credit scores or debt-to-income ratios.

Looking Ahead

Though trended data’s influence on approval rates remains uncertain, proactive credit management is key. As Dietz emphasizes, “Recent behavior carries the most weight. Prioritize timely payments and prudent credit use to improve your chances of securing a mortgage.”