The Mortgage Underwriting Process: A Comprehensive Guide

The Mortgage Underwriting Process: A Comprehensive Guide

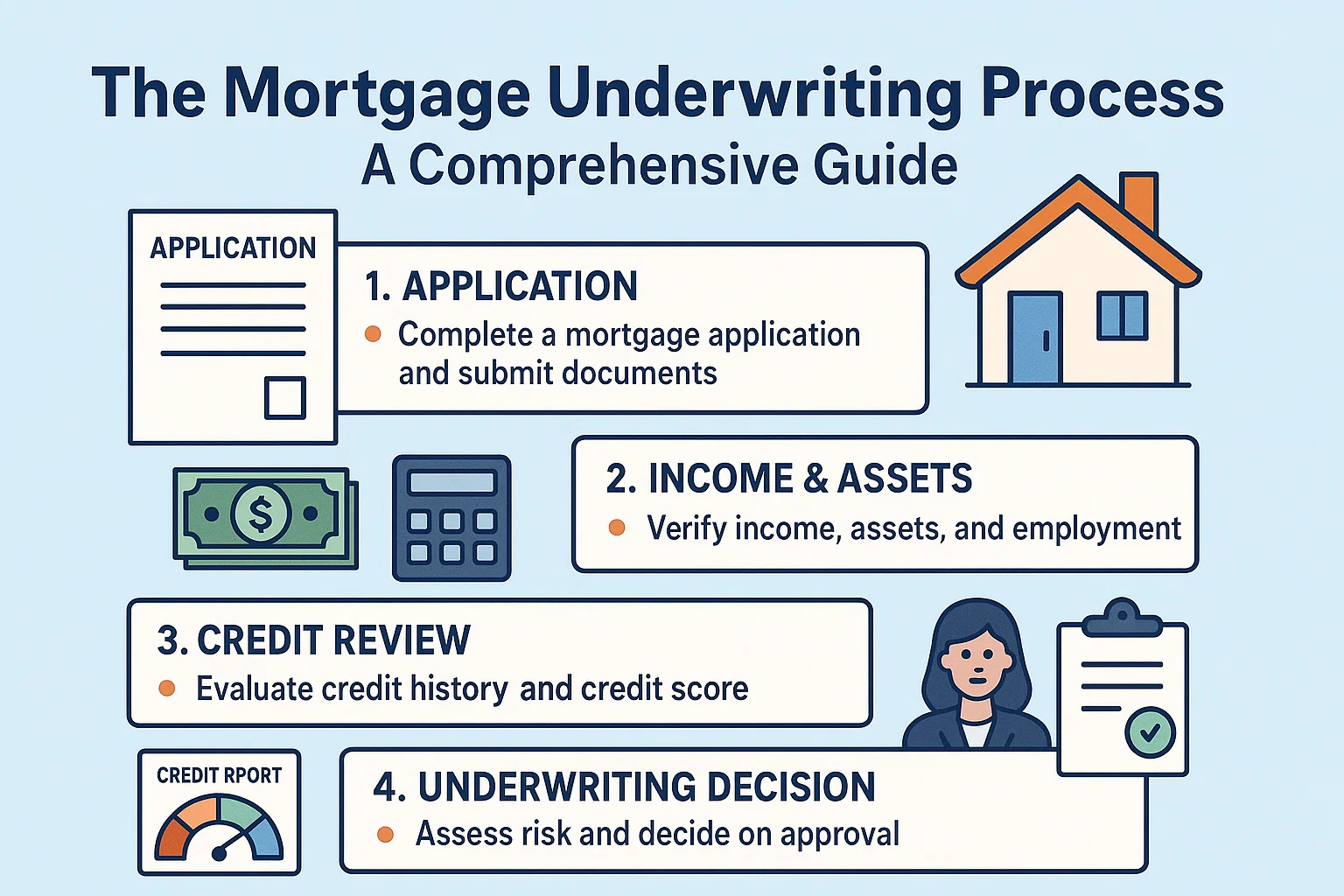

After collaborating with a Loan Officer to select the ideal loan option and submitting your financial documentation, your application moves to the next critical stage: underwriting. But what exactly does an underwriter do, and how do they influence your mortgage approval?

What Is Mortgage Underwriting?

Underwriting involves a meticulous review of your financial profile. The underwriter scrutinizes your income, assets, debts, and credit history to ensure compliance with your chosen loan program’s guidelines. Their analysis determines whether you qualify for the mortgage and can manage monthly payments responsibly.

Key Factors Evaluated During Underwriting

1. Income Verification

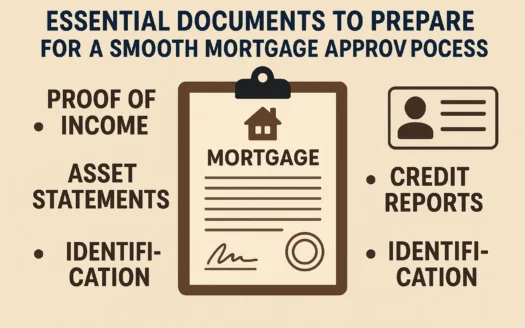

Underwriters require proof of stable income, such as:

- Recent pay stubs

- Tax returns

- Bank statements

- Accounting records (for self-employed applicants)

These documents confirm your ability to maintain consistent mortgage payments.

2. Debt-to-Income Ratio (DTI)

Your DTI is calculated by dividing your total monthly debt obligations by your gross monthly income. A lower ratio improves approval odds, as it signals financial stability and reduced risk of overextension.

3. Credit History Analysis

Underwriters review your credit report to identify potential risks, such as late payments or high credit utilization. Maintaining strong credit habits—like timely payments and low balances—boosts your chances of approval.

Why Does Underwriting Matter?

The underwriter’s role is to protect both lenders and borrowers by ensuring loans are granted responsibly. Their thorough evaluation minimizes financial risks and confirms your readiness for homeownership.

By understanding these steps, you can better prepare for a smooth underwriting process and move closer to securing your new home.