The Hidden Advantages of Private Mortgage Insurance for Homebuyers

The Hidden Advantages of Private Mortgage Insurance for Homebuyers

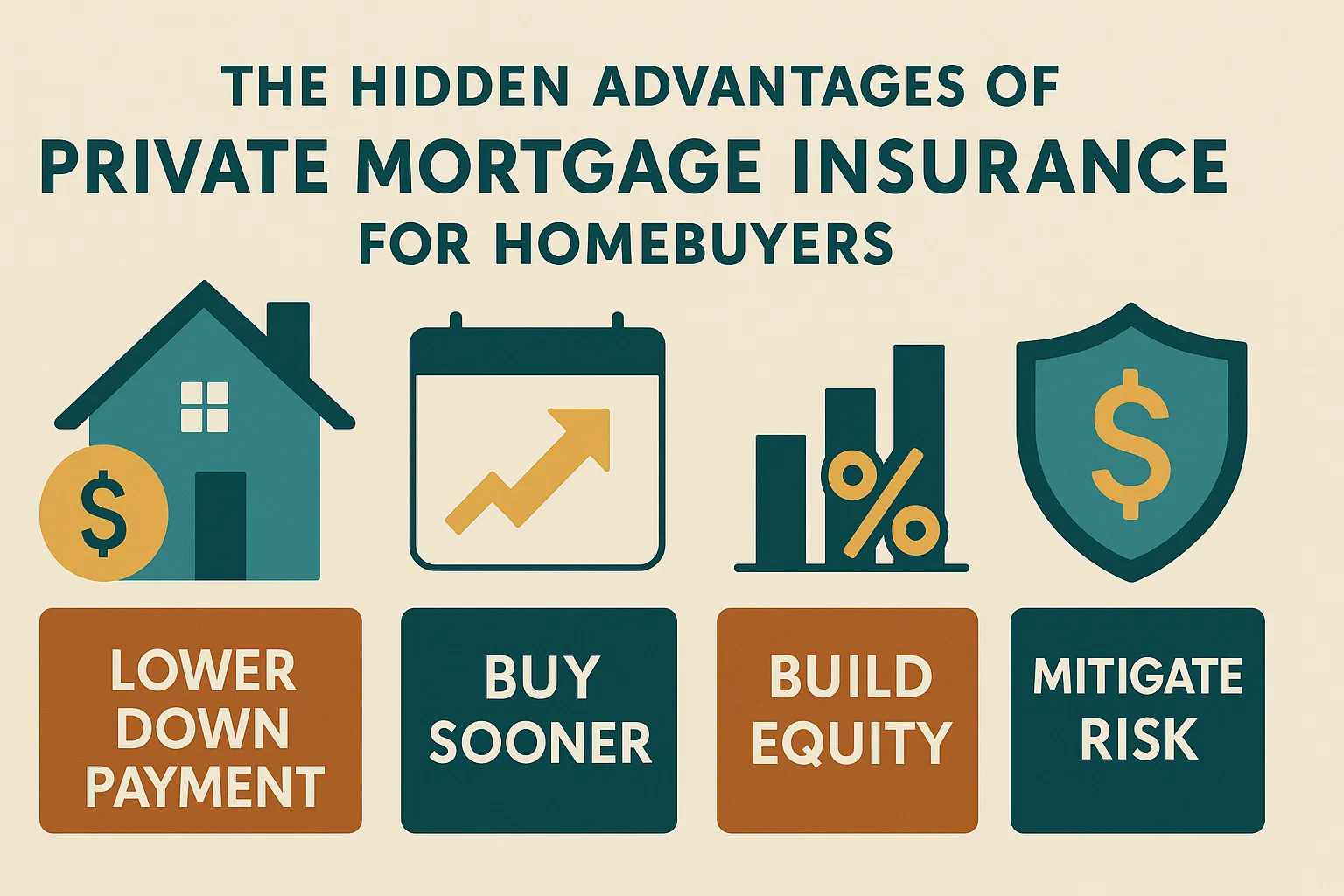

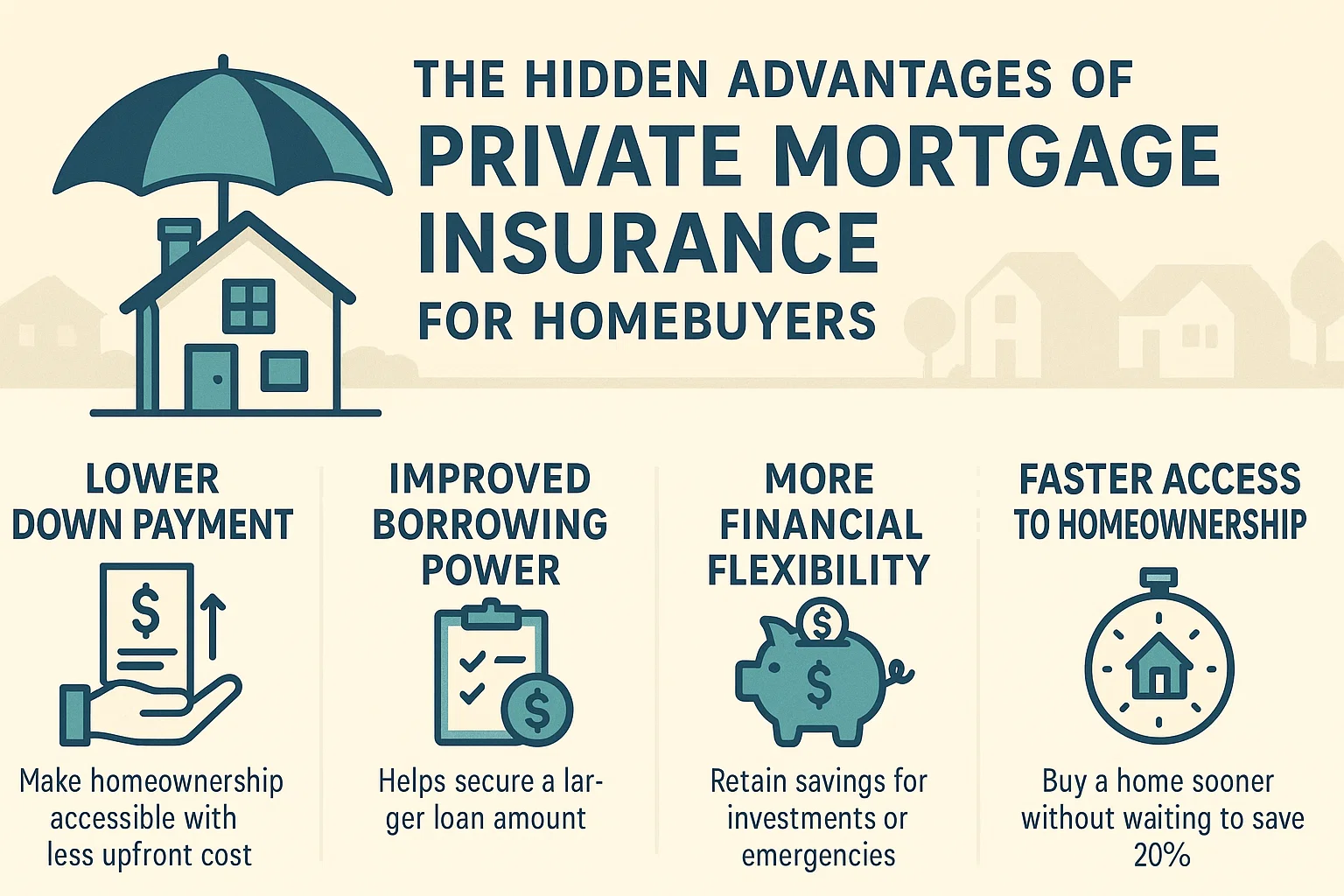

If you’re familiar with private mortgage insurance (PMI), your first thought might be: “This only helps the lender.” Most discussions focus on avoiding PMI by saving a 20% down payment or canceling it once equity reaches 20%. However, many buyers still choose loans requiring PMI—and for good reasons. Here’s why:

Why PMI Can Work in Your Favor

- Access to Financing Sooner

PMI lets lenders approve borrowers with smaller down payments (as low as 3-5%). For buyers without years to save, this opens doors to homeownership earlier. - Start Building Equity Immediately

Even with a smaller down payment, homeowners begin accruing equity as they make mortgage payments—and if property values rise, that equity grows faster. - Lock in Competitive Rates

PMI-backed loans often come with lower interest rates compared to alternatives like piggyback loans. Over time, this can save thousands in interest.

The Bottom Line

While PMI isn’t ideal for everyone, it empowers buyers to purchase homes sooner, capitalize on market opportunities, and build wealth through real estate—even before hitting that 20% equity milestone.