Navigating 2014 Mortgage Changes: Key Updates for Homebuyers

Navigating 2014 Mortgage Changes: Key Updates for Homebuyers

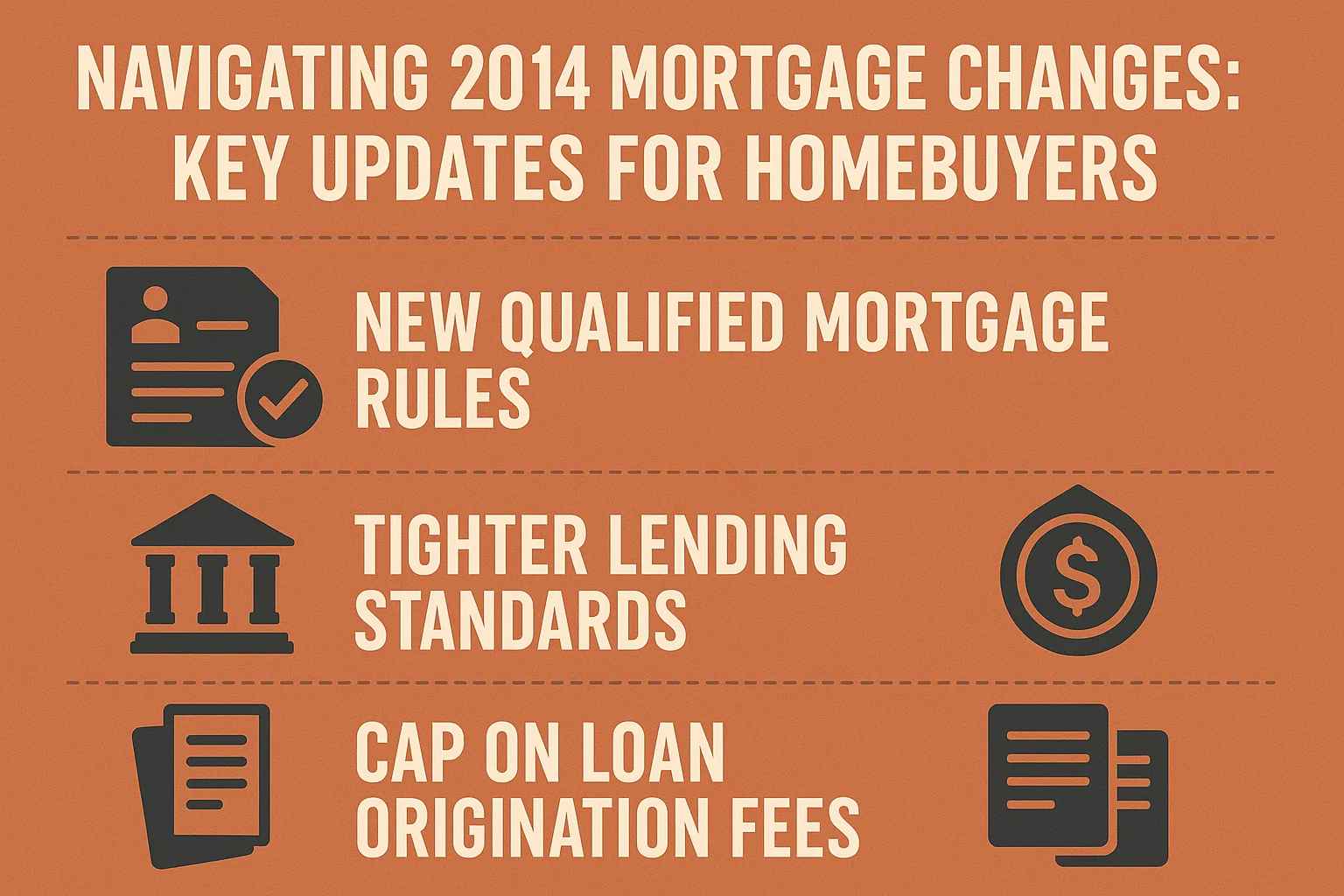

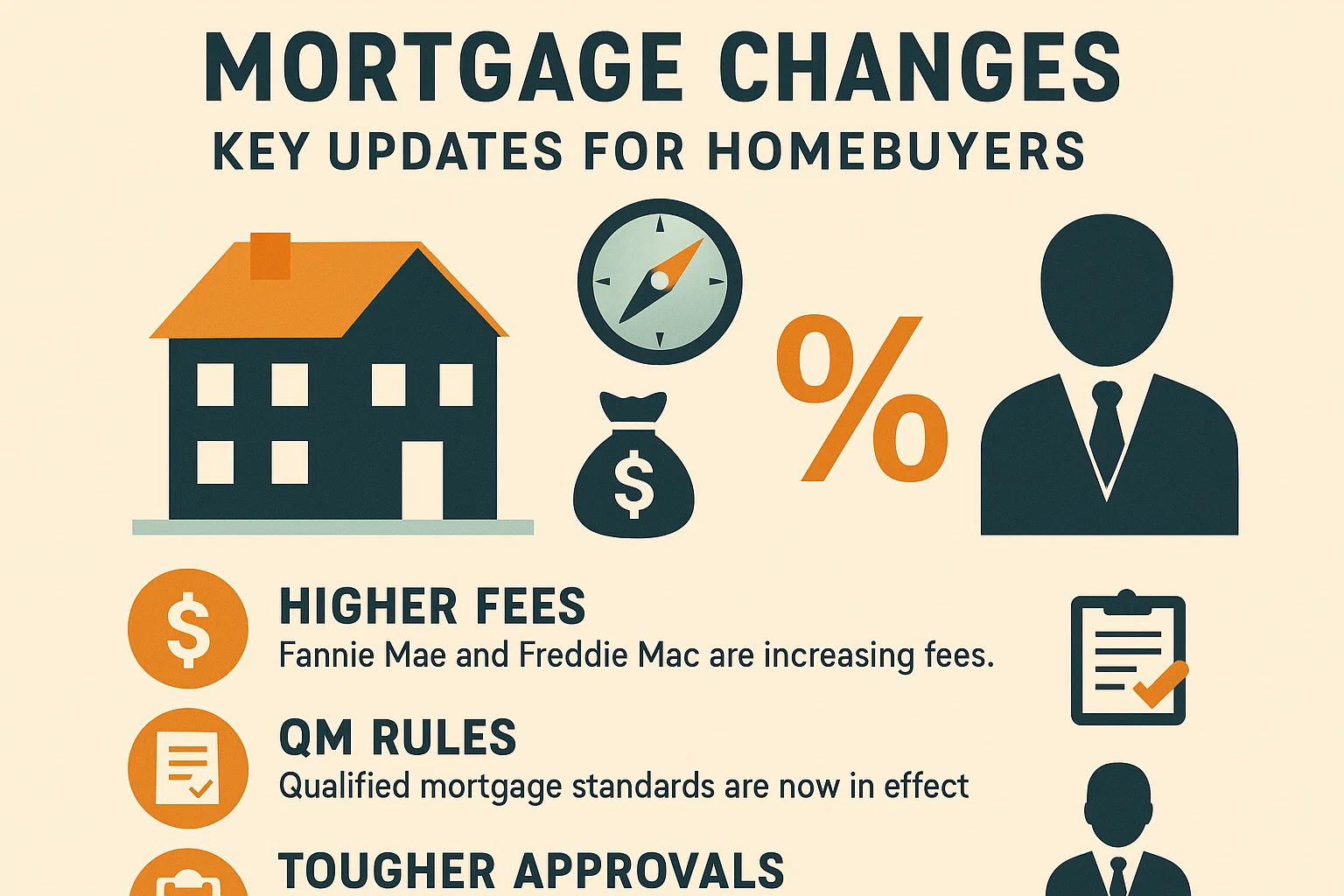

Understanding Qualified Mortgage Rules

Starting in January 2014, the Consumer Financial Protection Bureau (CFPB) introduced new regulations under the Dodd-Frank Act to define qualified mortgages. These rules set standards for lenders to assess a borrower’s ability to repay loans, aiming to reduce risky lending practices. Key features include:

- Debt-to-Income Ratio: Borrowers must maintain a monthly debt-to-income ratio of 43% or lower.

- Risk-Free Terms: Loans cannot include risky features like interest-only periods, negative amortization, balloon payments, or terms exceeding 30 years.

- Fee Restrictions: Limits on upfront or hidden fees, such as origination costs and real estate service charges.

These changes aim to protect borrowers from unaffordable debt while maintaining accessibility for those with smaller down payments or credit scores above 620.

FHA Loan Limit Adjustments

Federal Housing Administration (FHA) loan limits decreased in most U.S. counties between 2013 and 2014. Prospective homebuyers should verify current limits in their area to determine how much they can finance through an FHA loan.

Essential Financial Preparation Tips

To better prepare for homeownership in light of these updates, consider the following strategies:

- Credit Score Goals: While no minimum credit score is mandated, aim for at least 620 (ideally 720+) to improve approval odds.

- Budget Planning: Calculate affordability using the 43% debt-to-income threshold and account for potential interest rate increases.

- Down Payment Flexibility: Loans with down payments below 20% remain available for qualified buyers.

Final Considerations

Stay informed about evolving mortgage regulations and consult a trusted loan officer to navigate eligibility requirements. Proactive financial planning remains critical to securing a home within your budget.