How Buying a Home Impacts Your Credit Score: Short-Term Dips vs. Long-Term Gains

How Buying a Home Impacts Your Credit Score: Short-Term Dips vs. Long-Term Gains

If you’re preparing to buy your first home, you may ask, “How will this affect my credit score?” While the mortgage process does influence your credit, the effects are typically minor and temporary. Here’s what you need to know.

The Mortgage Process and Your Credit Score

During prequalification, lenders review your credit report to assess your eligibility for a loan. Each review triggers a hard inquiry, which may lower your score slightly. To minimize this impact:

- Limit your mortgage shopping to a 30-day window: Credit bureaus often treat multiple inquiries within this period as a single event.

Why Opening a Mortgage Affects Your Score

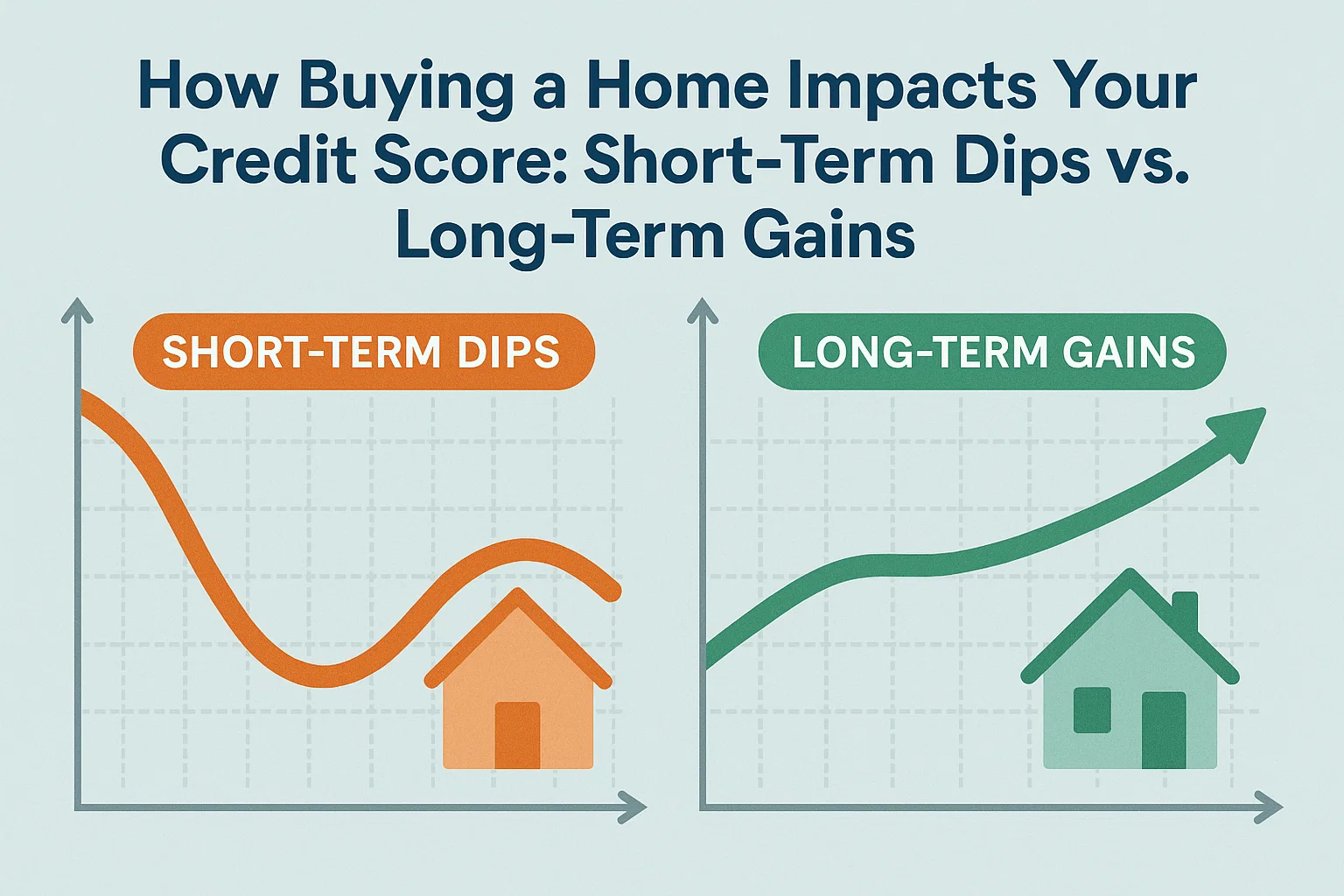

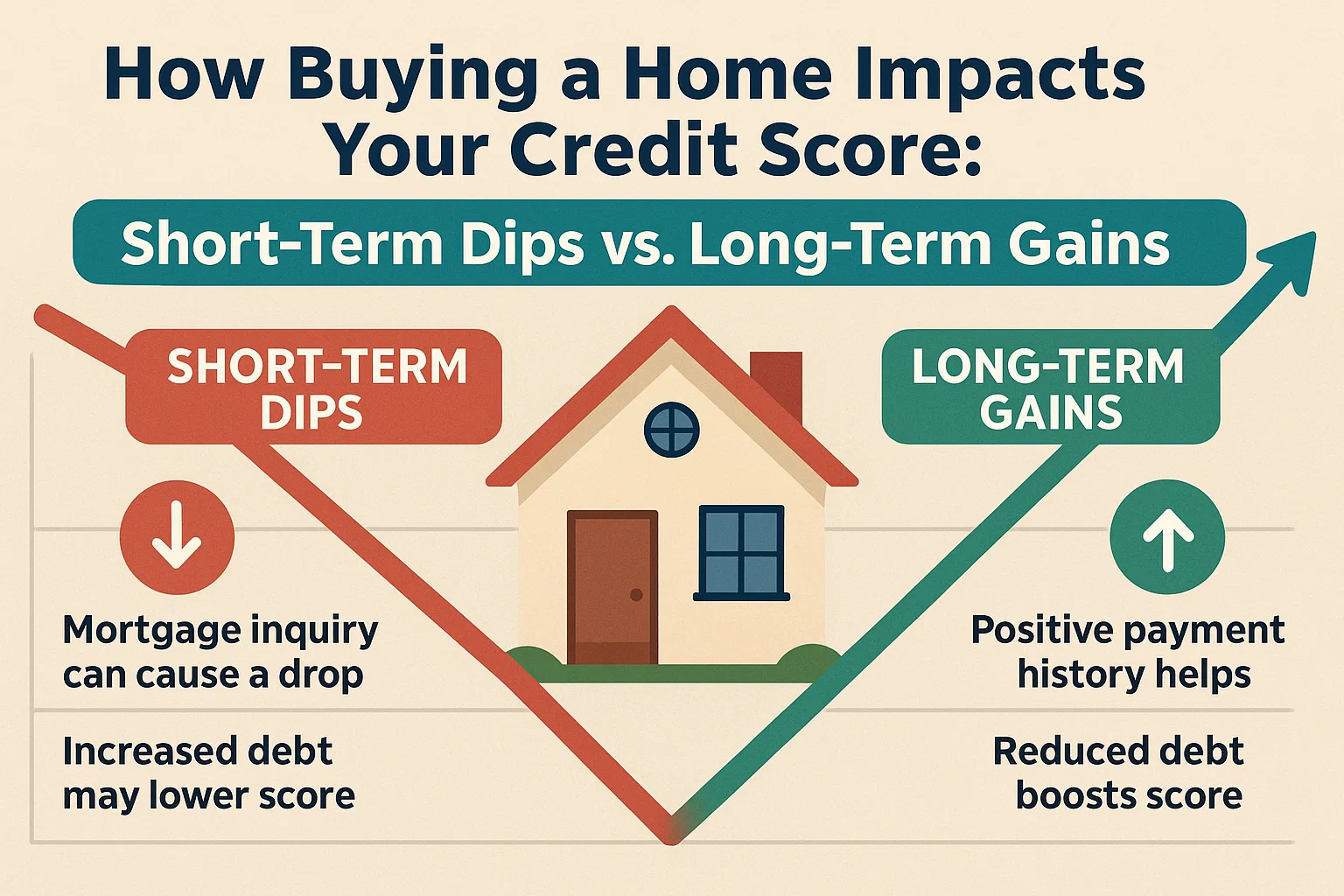

Approving a mortgage loan creates a larger temporary dip in your credit score. As a first-time buyer with no prior mortgage history, lenders view this as a higher-risk financial commitment. However, this drop is not permanent.

Long-Term Credit Benefits of a Mortgage

While initial effects may seem concerning, a mortgage can boost your credit health over time. Consistent, on-time payments demonstrate financial responsibility, leading to:

- A stronger payment history (35% of your credit score)

- Improved credit mix (10% of your score)

- Gradual recovery and growth of your score

Key Takeaway

Short-term credit score fluctuations are normal during the homebuying process. Focus on maintaining timely payments post-purchase to build a healthier financial profile over time.