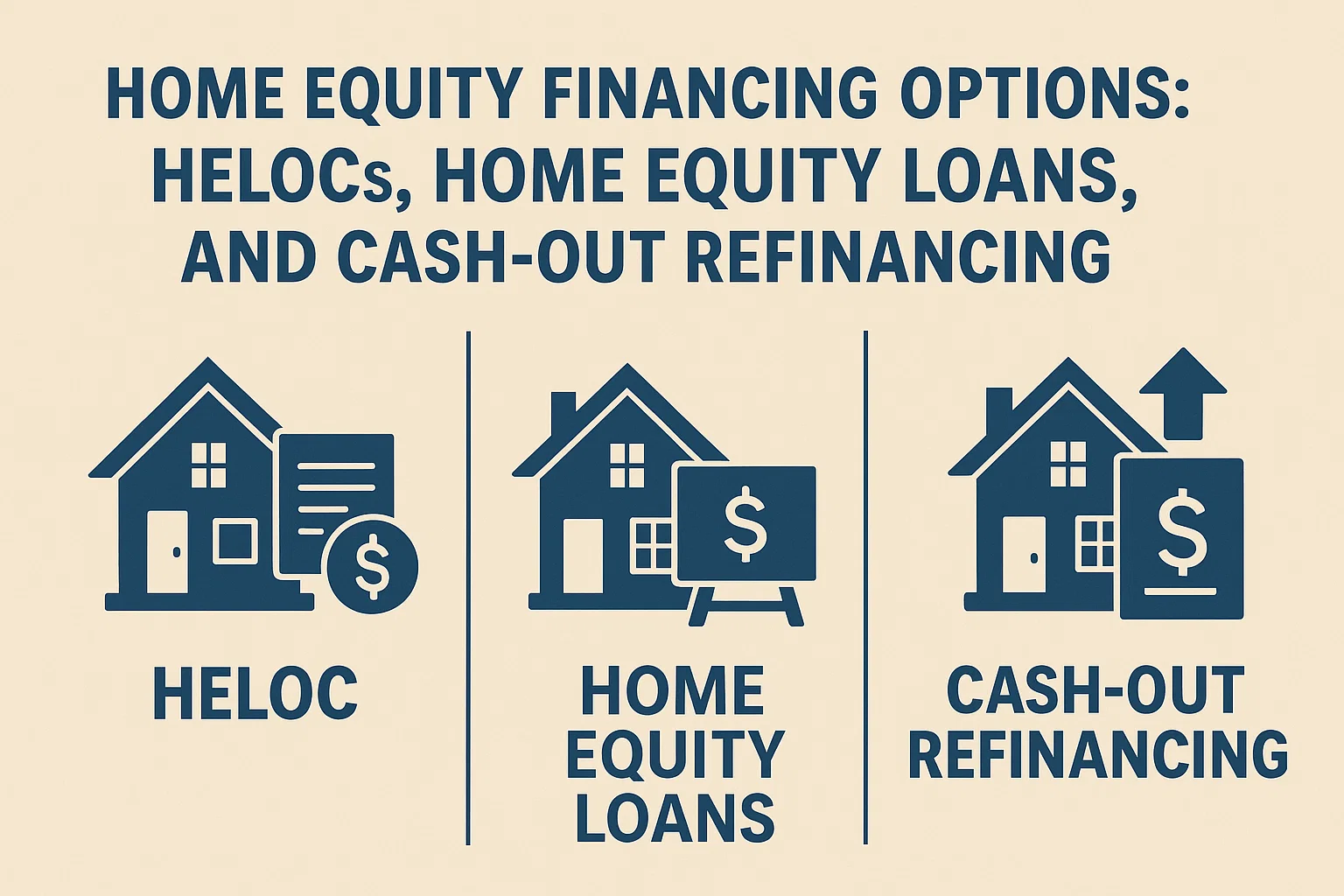

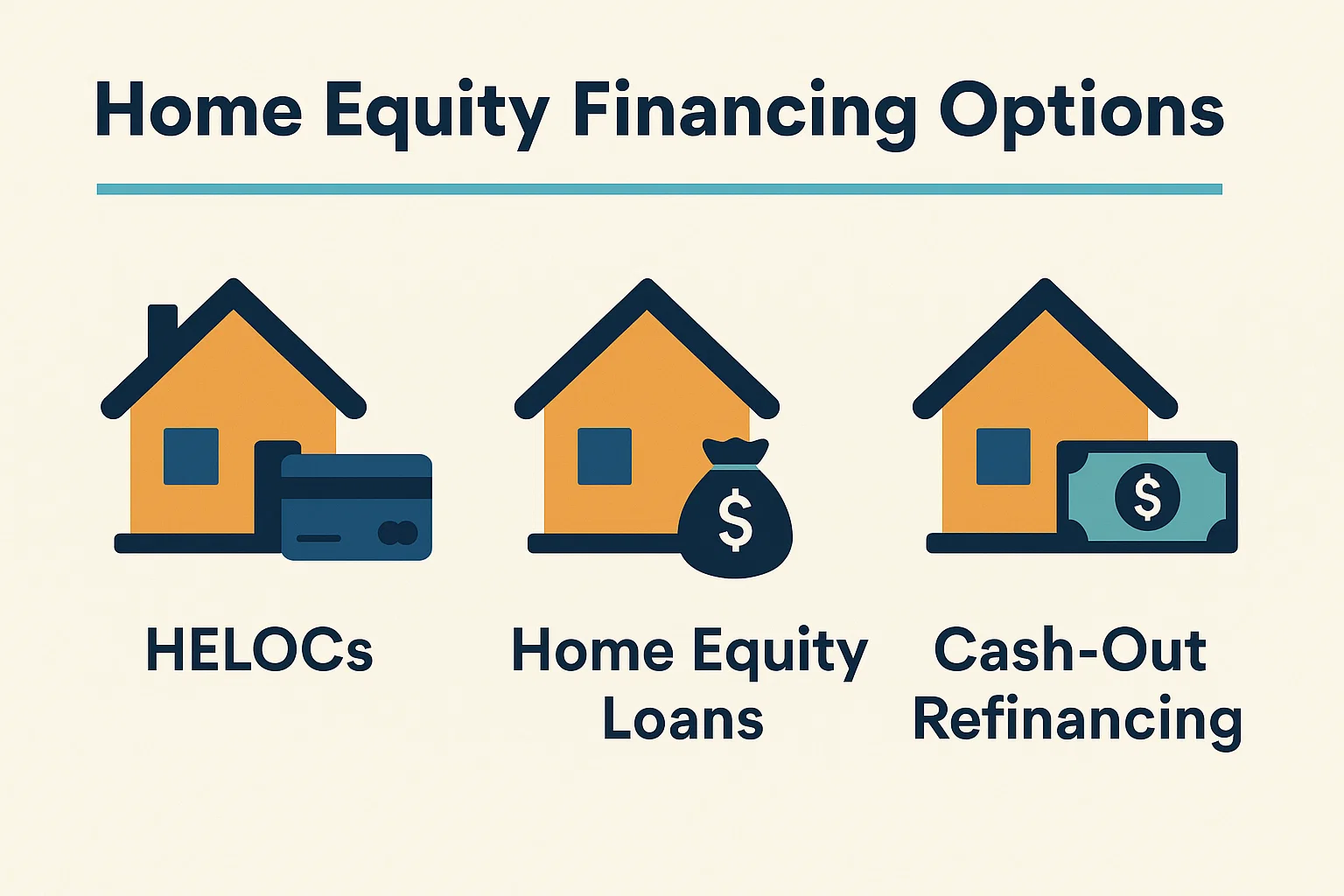

Home Equity Financing Options: HELOCs, Home Equity Loans, and Cash-Out Refinancing

Home Equity Loans, Home Equity Lines of Credit, and Cash-Out Refinancing: A Comprehensive Guide

As a homeowner, you have several options to secure extra cash when you need it by using your home’s equity. All three options allow you to use the financing as needed, whether to pay for major home renovations, consolidate debts, or cover emergency expenses. However, because your home is used as collateral, you risk losing equity if you default. Below, we break down how each option works, their benefits, and drawbacks.

How Does Each Option Work?

Home Equity Line of Credit (HELOC)

A HELOC functions like a revolving line of credit. You can withdraw funds as needed during a draw period (typically 10 years), making minimum interest-only payments. After the draw period ends, you enter the repayment period (10–20 years), where you repay the principal plus interest. Some lenders may require a balloon payment if the balance isn’t fully repaid by the end.

Home Equity Loans

This option provides a lump sum payout with fixed monthly payments over a term of 5–30 years. Often called a “second mortgage,” it uses your home equity as collateral. Borrowers must manage both their primary mortgage and this loan simultaneously.

Cash-Out Refinancing

This replaces your existing mortgage with a new, larger loan. The difference between the new loan and your current mortgage balance is paid out in cash. Terms, rates, and monthly payments are reset, which could lower costs if interest rates have dropped.

How Much Can I Borrow With Each Option?

Photo Credit: Alexander Mils from Unsplash

- HELOC: Typically 60%–85% of your home’s value minus the mortgage balance.

- Home Equity Loan: Usually 75%–85% of your home’s equity.

- Cash-Out Refinance: Up to 80% of your home’s value (up to 100% for VA loans).

Interest Rates and Repayment

- HELOC: Variable rates (some lenders allow partial fixed rates during repayment).

- Home Equity Loan: Fixed rates with predictable payments.

- Cash-Out Refinance: Fixed or variable rates, depending on lender terms.

Closing Costs

All options include fees such as appraisal, title search, and application costs. Cash-out refinancing tends to be the most expensive due to the new mortgage setup.

Comparison Chart

| Loan Type | Interest Rate | Payout | Repayment Terms | Closing Costs |

|---|---|---|---|---|

| HELOC | Variable (partial fixed possible) | Revolving line of credit | 10-year draw period + 10–20-year repayment | Yes |

| Home Equity Loan | Fixed | Lump sum | Up to 30 years | Yes |

| Cash-Out Refinance | Fixed or variable | Lump sum | New mortgage terms | Yes |

When to Choose Each Option

HELOC

Ideal for ongoing or unpredictable expenses (e.g., renovations). Offers flexibility but requires discipline to manage variable rates and repayment spikes.

Home Equity Loan

Best for one-time expenses with known costs. Fixed payments simplify budgeting but add a second mortgage payment.

Cash-Out Refinance

Opt for this if rates have dropped or you need a large sum. Be prepared for higher long-term mortgage debt and potential PMI costs.

Final Considerations

Evaluate your financial stability, project scope, and risk tolerance before choosing. Consult a financial advisor to ensure your home equity remains protected.