Finding and Securing a Mortgage to Finance Your New Home: A Step-by-Step Checklist

Finding and Securing a Mortgage to Finance Your New Home: A Step-by-Step Checklist

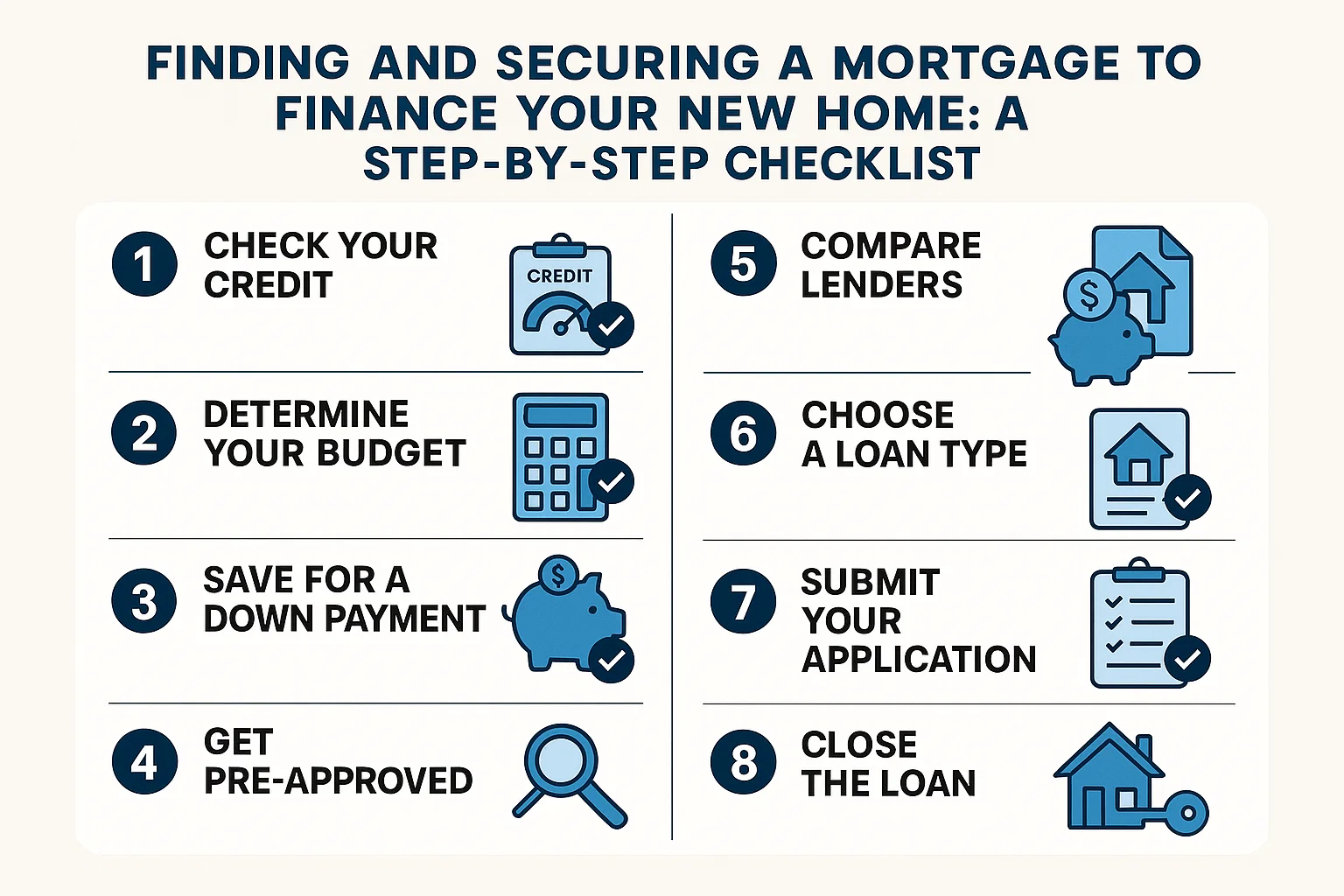

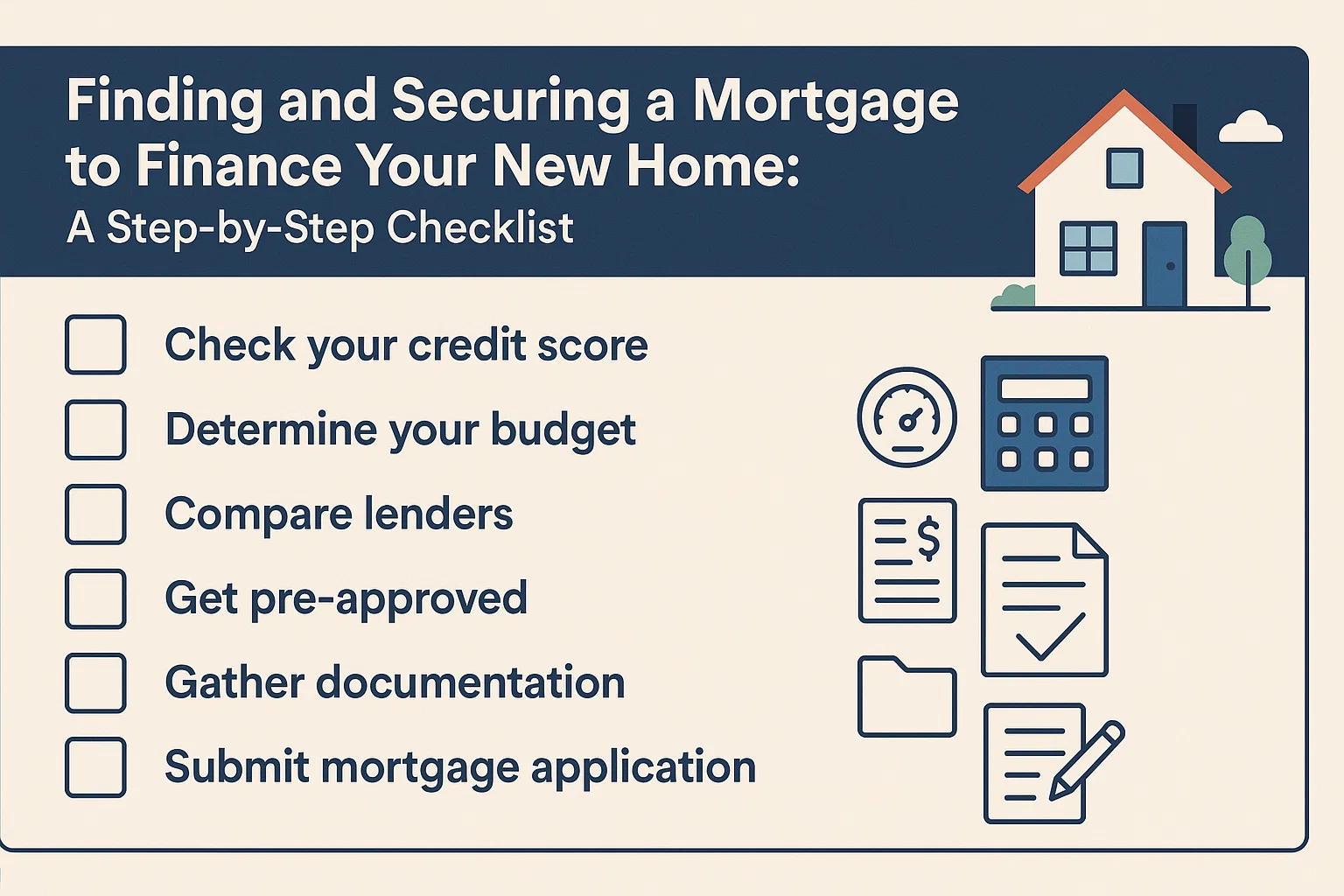

Navigating the mortgage process for your new home can feel overwhelming, especially as a first-time buyer. However, breaking it down into manageable steps can simplify the journey. This checklist will guide you through preparation, paperwork, and securing the most cost-effective loan. Let’s begin with the first four steps, which should be completed well before actively shopping for a loan.

1. Review Your Overall Financial Picture

- Analyze your monthly income, living expenses, and savings or equity available for a down payment.

- Calculate your debt-to-income (DTI) ratio—the percentage of your gross monthly income allocated to existing debts (credit cards, loans, etc.).

- Use online resources to estimate affordability. For detailed guidance, review the article “How Much Home Can You Really Afford?”

2. Check Your Credit Reports

- Request free annual reports from all three credit bureaus (Equifax, Experian, TransUnion).

- Dispute errors or outdated information with creditors immediately. Federal law guarantees your right to accurate reports.

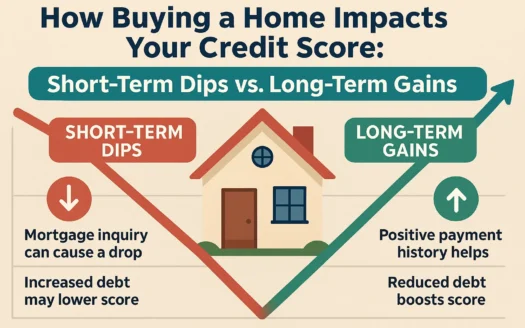

3. Check Your FICO Scores

- FICO scores determine mortgage eligibility and rates. Aim for a score of 680+ to qualify and 740+ for the best rates.

- Purchase your FICO scores directly from credit bureaus or via myFICO.com.

4. Compare Mortgage Types

- 30-Year vs. 15-Year Loans: Longer terms lower monthly payments; shorter terms build equity faster.

- FHA/VA/Rural Loans: Low down payments and credit requirements.

- Adjustable-Rate Mortgages (ARMs): Fixed rates initially, then adjust annually. Riskier if rates rise.

- Conventional Loans: Ideal with a 20% down payment.

5. Shop for a Mortgage

- Compare rates, terms, and lender reputations online and locally.

- Note: Quotes are non-binding until you submit a formal application.

Key Factors to Compare:

- Interest Rates: Small rate differences often reflect varying fees.

- Points: Upfront fees to lower rates. Choose lower points for short-term homeownership.

- Annual Percentage Rate (APR): Reflects the true cost of the loan, including fees.

- Rate Lock Costs: Fees to guarantee rates beyond 30, 45, or 60 days.

- Debt-to-Income Limits: Confirm your DTI aligns with lender requirements.

- Loan Amount: Verify the lender’s maximum offer based on your finances.

- Turnaround Time: Average processing duration from application to closing.

- Junk Fees: Scrutinize origination, processing, and application charges.

6. Select the Best Lender

- Choose the loan with the lowest total cost and terms that fit your goals.

- Request a pre-approval letter to strengthen homebuying offers.

7. Find a Home and Sign a Purchase Contract

- Submit a copy of the signed contract with your loan application.

8. Submit a Formal Loan Application

- Review the lender’s Truth in Lending Disclosure and Good Faith Estimate within three business days.

- Clarify fees and confirm closing details upfront.

9. Monitor Loan Processing

- Track the appraisal, underwriting requests, and potential delays.

- Request a copy of the appraisal and review it for accuracy.

10. Review the Settlement Sheet (HUD-1)

- Compare line-item charges with initial estimates three days before closing.

- Dispute discrepancies immediately.

11. Closing Day

- Sign final documents. Congratulations—you’re a homeowner!