Financing Home Repairs: A Guide to FHA Rehabilitation Loans

Transform Your Home with an FHA Rehabilitation Loan

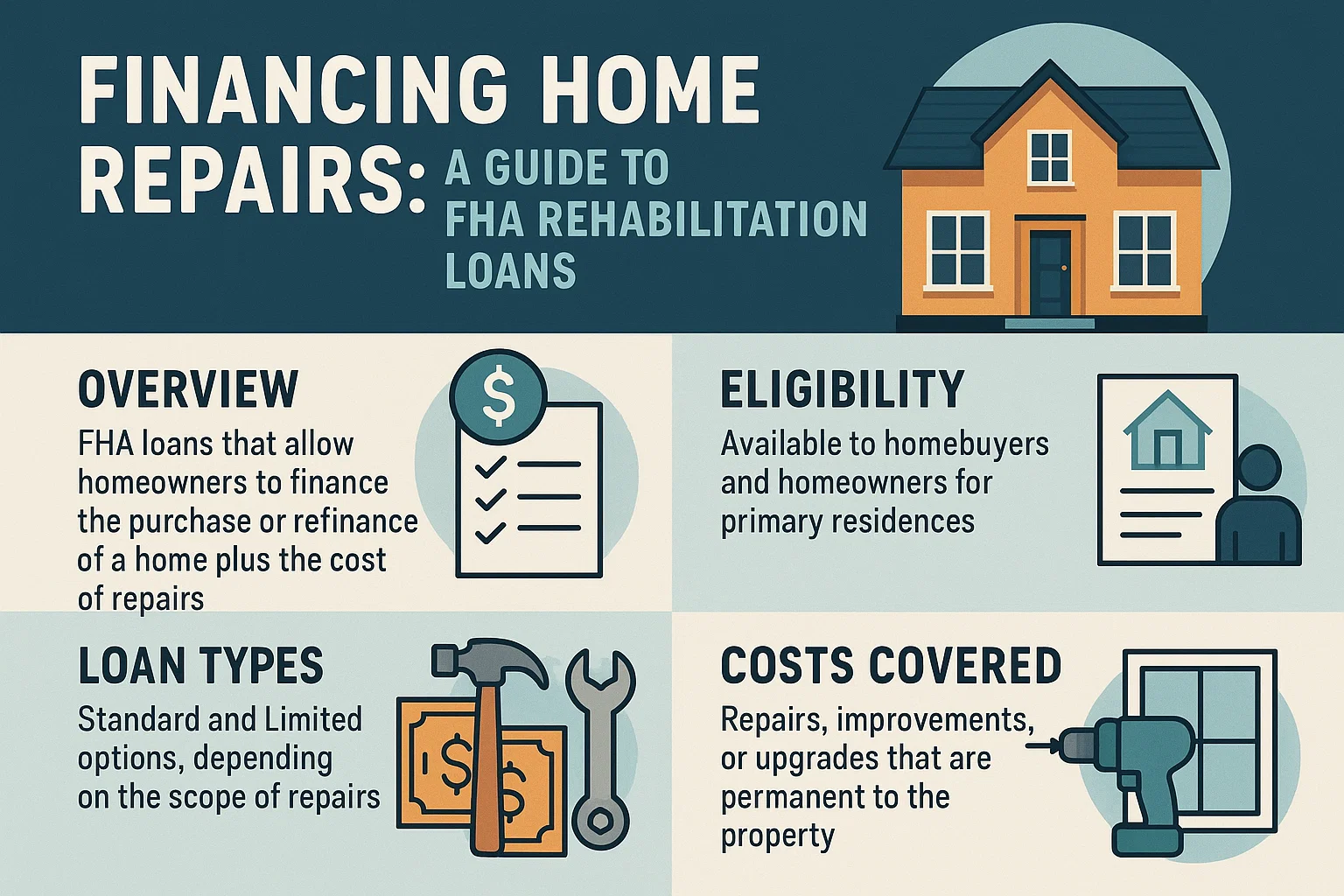

If your home has sustained damage from a natural disaster—such as flooding, storms, or fires—or you’ve discovered an opportunity to purchase a fixer-upper at a discounted price, an FHA 203(k) rehabilitation loan could be the solution you need. This specialized mortgage enables homeowners to finance both the purchase (or refinance) of a property and the cost of renovations, all while leveraging the home’s projected post-repair value. However, this loan is exclusively available for primary residences and cannot be used for investment properties.

How the FHA 203(k) Loan Works

Imagine your home requires a new roof after a severe storm, and your kitchen needs a full remodel. With a Standard FHA 203(k) loan, you can access funds from an escrow account to cover these repairs as the project progresses. This option is ideal for larger-scale renovations, including structural changes or major upgrades.

Standard vs. Limited FHA 203(k) Options

- Standard FHA 203(k): Designed for significant renovations, such as room additions, plumbing overhauls, or foundation repairs.

- Limited FHA 203(k): Tailored for smaller projects like repainting, flooring replacement, or minor cosmetic updates (with a maximum renovation cost of $35,000).

When to Consider an FHA 203(h) Loan

For homes that have sustained catastrophic damage—such as total roof collapse or severe structural compromise—the FHA 203(h) program may be more appropriate. This option provides financial support specifically for disaster recovery, helping homeowners rebuild from the ground up.

Take the Next Step

If your home requires repairs or upgrades, consult a licensed loan officer to explore your eligibility. They’ll guide you through the process, including:

- Reviewing your renovation scope and budget

- Coordinating with approved contractors

- Managing escrow disbursements as work progresses