Demystifying Special Financing in Mortgage Lending

Demystifying Special Financing in Mortgage Lending

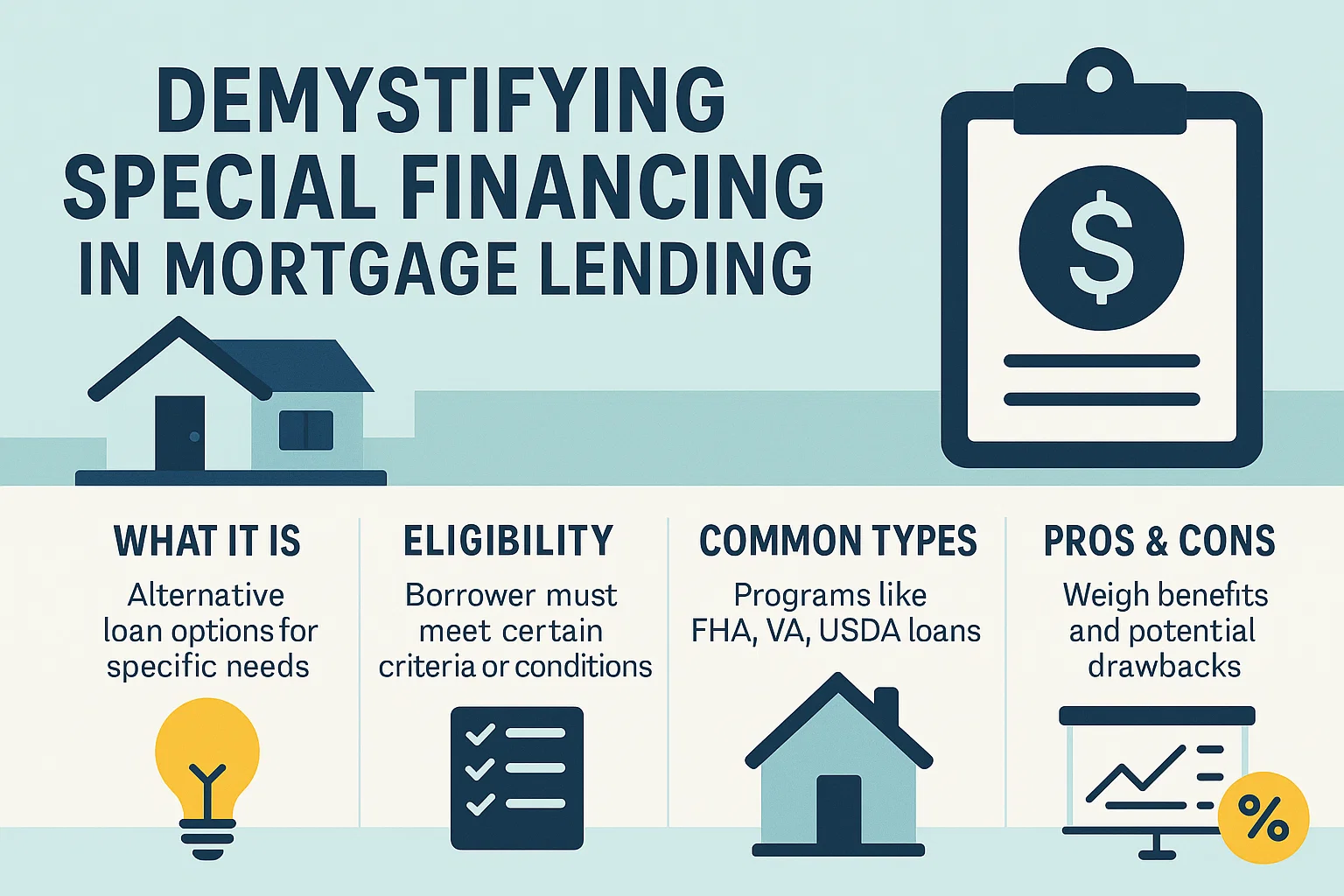

What Is Special Financing?

The term “special financing” can mean different things depending on the industry. For example:

- Auto dealers may use it to describe loans for buyers with poor credit.

- Retailers might offer deferred-interest plans that delay payments.

In mortgage lending, however, special financing carries a more borrower-friendly definition. It often refers to programs designed to reduce costs for qualified buyers—especially those with good credit.

How Mortgage Special Financing Works

Special financing options in mortgages aim to:

- Lower monthly payments by hundreds of dollars.

- Save thousands in interest over the loan’s lifetime.

- Make homeownership more accessible and affordable.

Special Financing vs. Market Rates: A Practical Example

Consider a 30-year fixed-rate FHA loan on a $420,000 home:

- Without special financing: Payments align with standard market rates.

- With special financing: Borrowers benefit from reduced rates, leading to significant savings.

While exact numbers depend on current rates, special financing typically offers a clear financial advantage.

Is Special Financing Right for You?

If you’re exploring mortgage options, special financing could be a strategic choice. Consult a mortgage advisor to compare programs, eligibility criteria, and long-term benefits tailored to your financial situation.