Debunking the 20% Down Payment Myth: Home Loan Options Explained

Debunking the 20% Down Payment Myth: Home Loan Options Explained

This article provides general information only and is not financial, tax, or legal advice. Consult appropriate professionals for guidance specific to your situation.

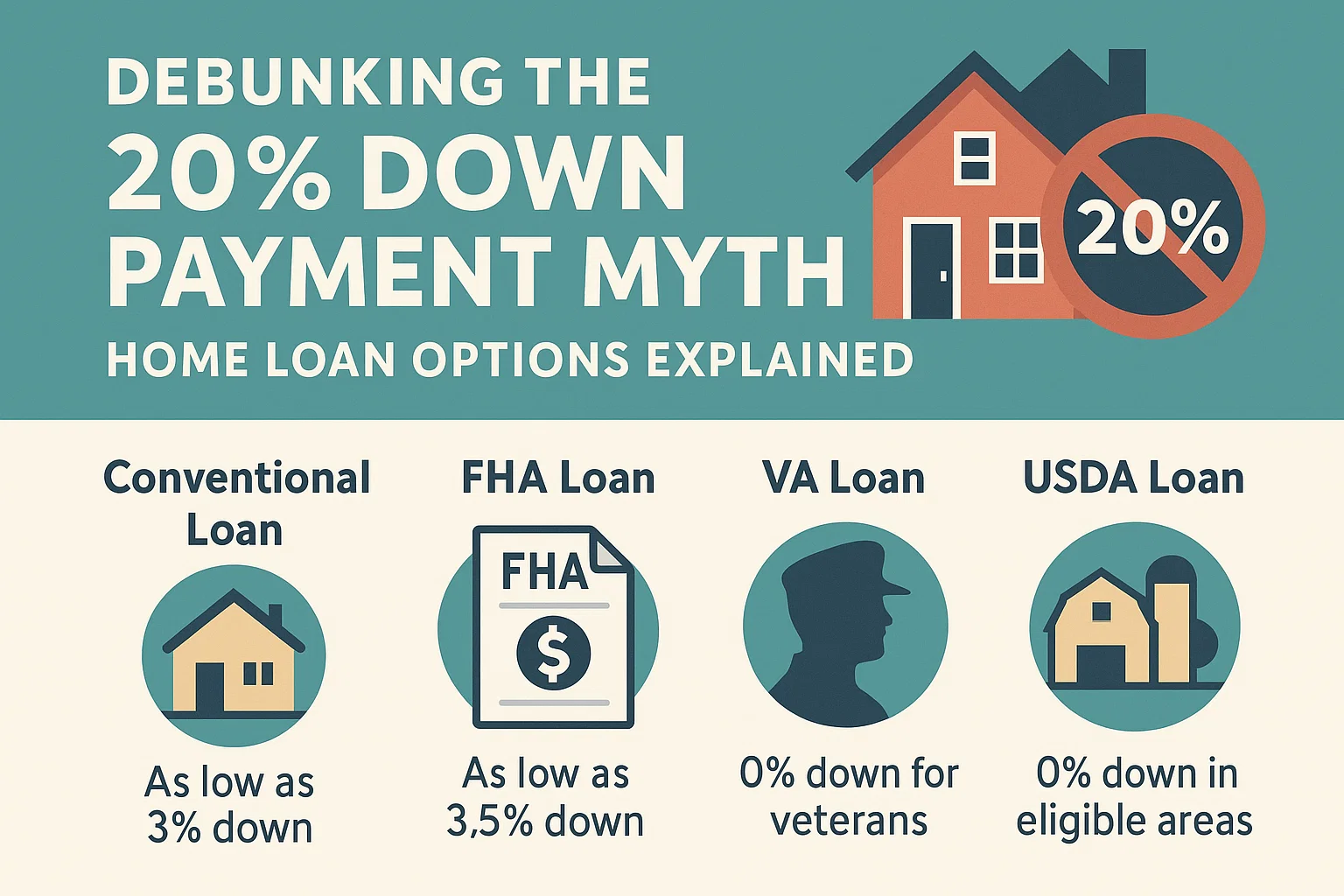

Do You Really Need a 20% Down Payment?

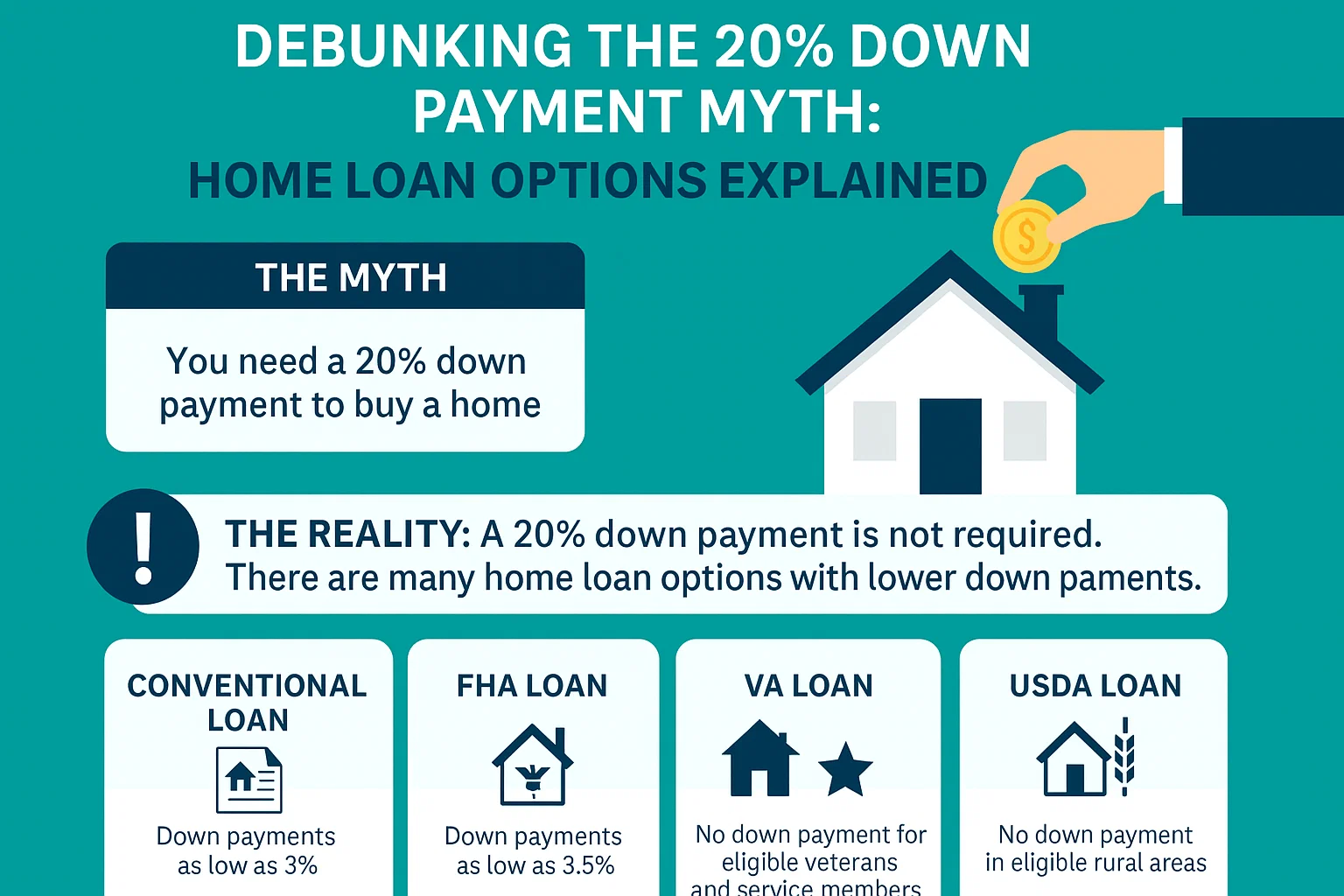

The short answer is no. The rule of 20% down is a myth. While putting 20% down on a new home offers certain benefits, you can still purchase your dream home with a smaller down payment. Let’s examine the loan options that make this possible.

Benefits of a 20% Down Payment

A down payment is an upfront payment made to purchase a home, calculated as a percentage of the home’s price. Larger down payments offer several advantages:

- Lower borrowing amount: You’ll need to borrow less money, reducing your overall debt

- Better lender perception: Demonstrates lower risk to lenders through improved loan-to-value (LTV) ratio

- Potential interest savings: Lower LTV may qualify you for better interest rates

- Reduced monthly payments: Smaller loan amounts mean lower monthly mortgage payments

- No PMI requirement: Avoids private mortgage insurance (PMI) fees typically required for smaller down payments

Assessing Your Financial Situation

Your ideal down payment amount depends on your specific financial circumstances:

- High savings, low income: Consider larger down payment to reduce monthly payments

- Low savings, steady income: Smaller down payment may work, with extra principal payments to build equity faster

Lenders evaluate your debt-to-income (DTI) ratio when qualifying you for loans. While 36% or lower is ideal, some loans accept higher ratios. A 50% DTI means half your monthly income goes toward debt payments, which may warrant paying down existing debt before applying for a mortgage.

Common Loan Options

The 20% down payment guideline originated from government-sponsored enterprises that guarantee most U.S. mortgages. Today, borrowers have multiple options:

Conventional Loans

Backed by private lenders, these come in two forms:

- Conforming loans: Meet standard guidelines, eligible for purchase by major mortgage entities

- Nonconforming (jumbo) loans: For luxury properties exceeding standard loan limits

FHA Loans

Designed for borrowers with moderate incomes and lower credit scores:

- 3.5% down payment with 580+ credit score

- 10% down with 500-579 credit score

- Requires mortgage insurance (MIP) for either 11 years or loan duration

VA Loans

For military members, veterans, and eligible spouses:

- No down payment required

- No mortgage insurance

- Competitive interest rates

- One-time funding fee instead of ongoing insurance

USDA Loans

For rural and suburban home purchases:

- 100% financing available (no down payment)

- Mandatory mortgage insurance with upfront and annual fees

HomeReady™ Mortgage

A Fannie Mae program with flexible requirements:

- 3% minimum down payment

- Accepts credit scores as low as 620

- Allows DTI up to 50%

- Requires homeownership education

Piggyback Loans

A secondary loan that combines with a conventional loan:

- Typically requires 10% down (some accept 5%)

- Second loan covers difference to reach 20%

- Avoids PMI but often has higher interest rates

Down Payment Assistance Programs

Various assistance programs may be available, typically for first-time homebuyers. These can provide funds as:

- Grants (no repayment required)

- Interest-free loans

- Forgivable loans (repaid only if home is sold or mortgage paid off)

Availability varies by location and program requirements.

Conclusion

The belief that you need 20% down to buy a home is outdated. While larger down payments offer advantages, numerous loan options and assistance programs exist to help buyers with various financial situations achieve homeownership. Consult with mortgage professionals to explore the best solution for your needs.