Debunking Common Home Buying Myths

Debunking Common Home Buying Myths

When it comes to buying a home, several myths may prevent potential homeowners from pursuing their dream of homeownership. Let’s clarify some of the most common misconceptions about the home buying process.

First-time buyers often make assumptions about down payments and other aspects of purchasing a home. The reality is that mortgage financing regulations have evolved significantly since the 2008 financial crisis. While lending standards initially tightened, adjustments were later made to improve accessibility for qualified buyers.

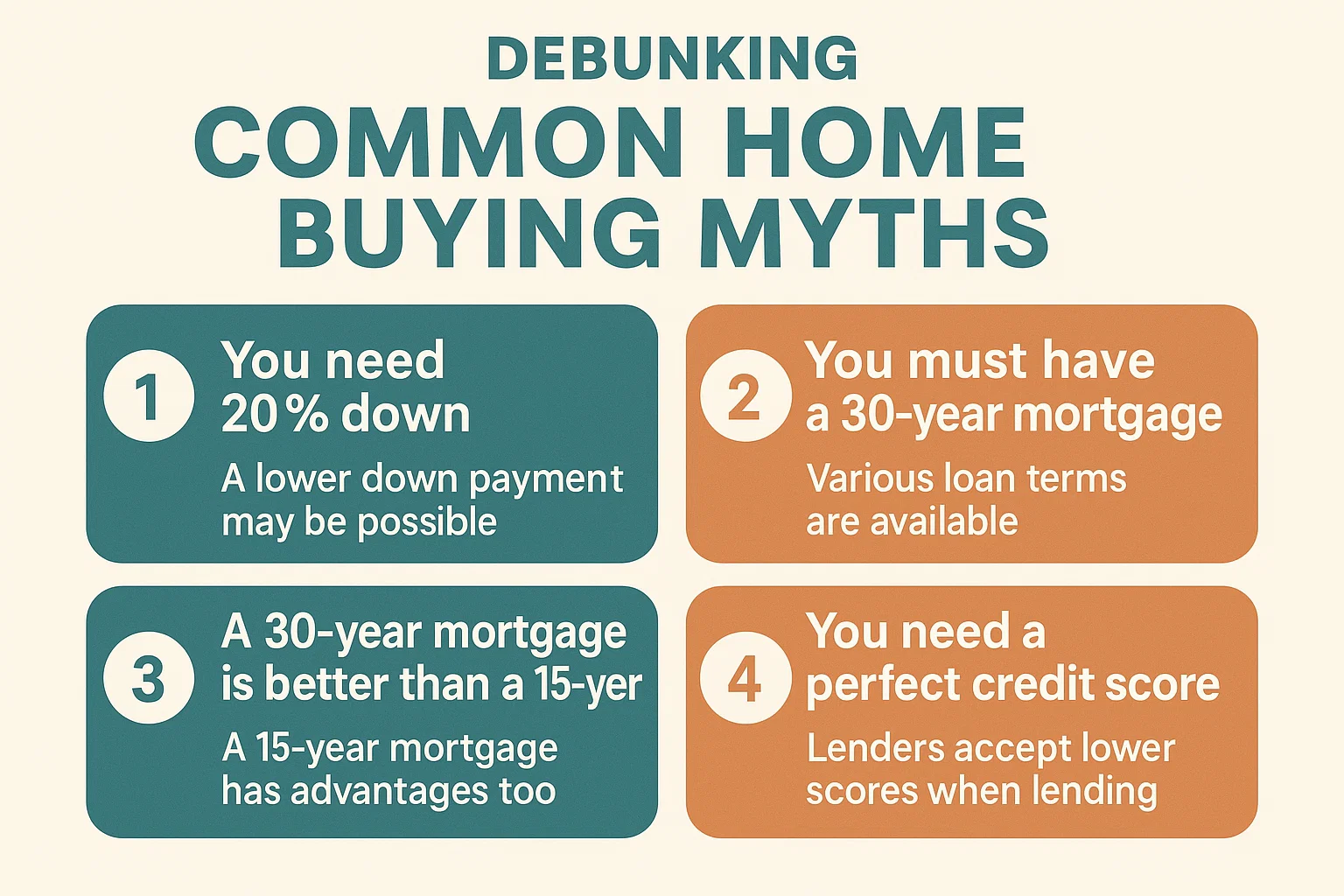

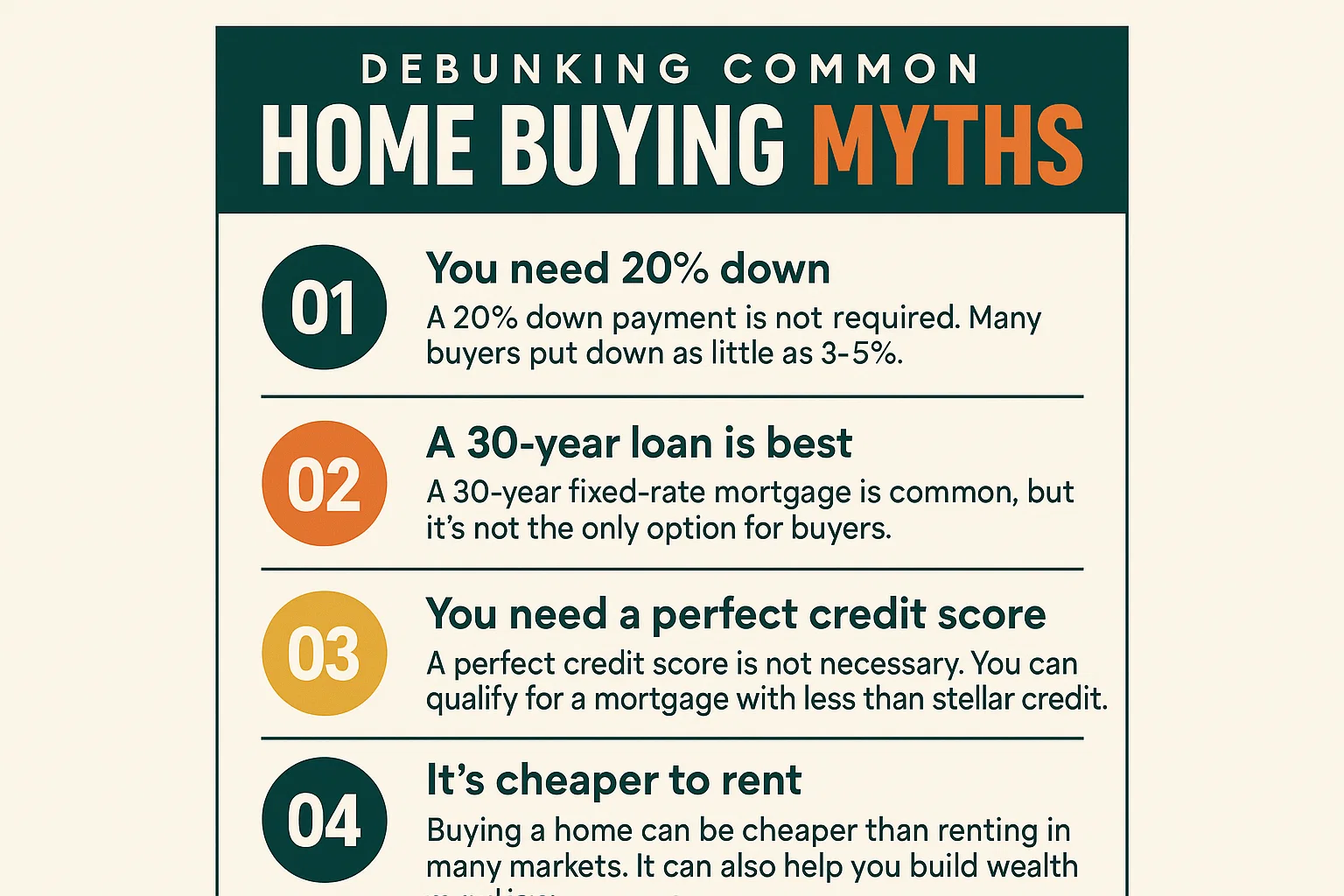

Myth: A Big Down Payment Is Required

Contrary to popular belief, most lenders require between 5% and 20% of a home’s purchase price for a down payment. For down payments under 20%, private mortgage insurance (PMI) is typically required to protect the lender. PMI usually costs between 0.5% and 1% of the loan amount annually.

Government-backed loans offer even more flexibility:

- FHA loans require as little as 3.5% down

- VA and USDA loans require no down payment for eligible buyers

Some programs allow buyers to pay mortgage insurance upfront rather than monthly, and various assistance programs may provide grants to qualified buyers who complete homebuyer education courses.

Myth: You Need Perfect Credit

While better credit scores secure more favorable terms, you don’t need perfect credit to buy a home:

- Conventional mortgages typically require a 640+ credit score

- FHA loans are available with scores as low as 580

- USDA loans require a minimum 620 score

Borrowers with lower scores may qualify but should expect higher interest rates.

Myth: Fixed-Rate Loans Are Always Best

The best loan type depends on how long you plan to stay in the home:

- 30-year fixed-rate mortgages work well for long-term homeowners

- Adjustable-rate mortgages (ARMs) or shorter-term fixed loans may be better for those planning to move within 4-7 years

ARMs often start with lower rates than fixed-rate loans, though they can adjust over time based on market conditions.

Myth: Location Is Everything

While location matters, the “perfect” neighborhood isn’t always the best investment. Savvy buyers should consider:

- Areas with planned development or construction

- Neighborhoods that may improve over 5-10 years

- Communities that offer good value relative to nearby areas

Sometimes the best opportunities are in neighborhoods that haven’t yet reached their full potential.