Cash vs. Financing: Weighing the Risks in a Competitive Housing Market

Cash vs. Financing: Weighing the Risks in a Competitive Housing Market

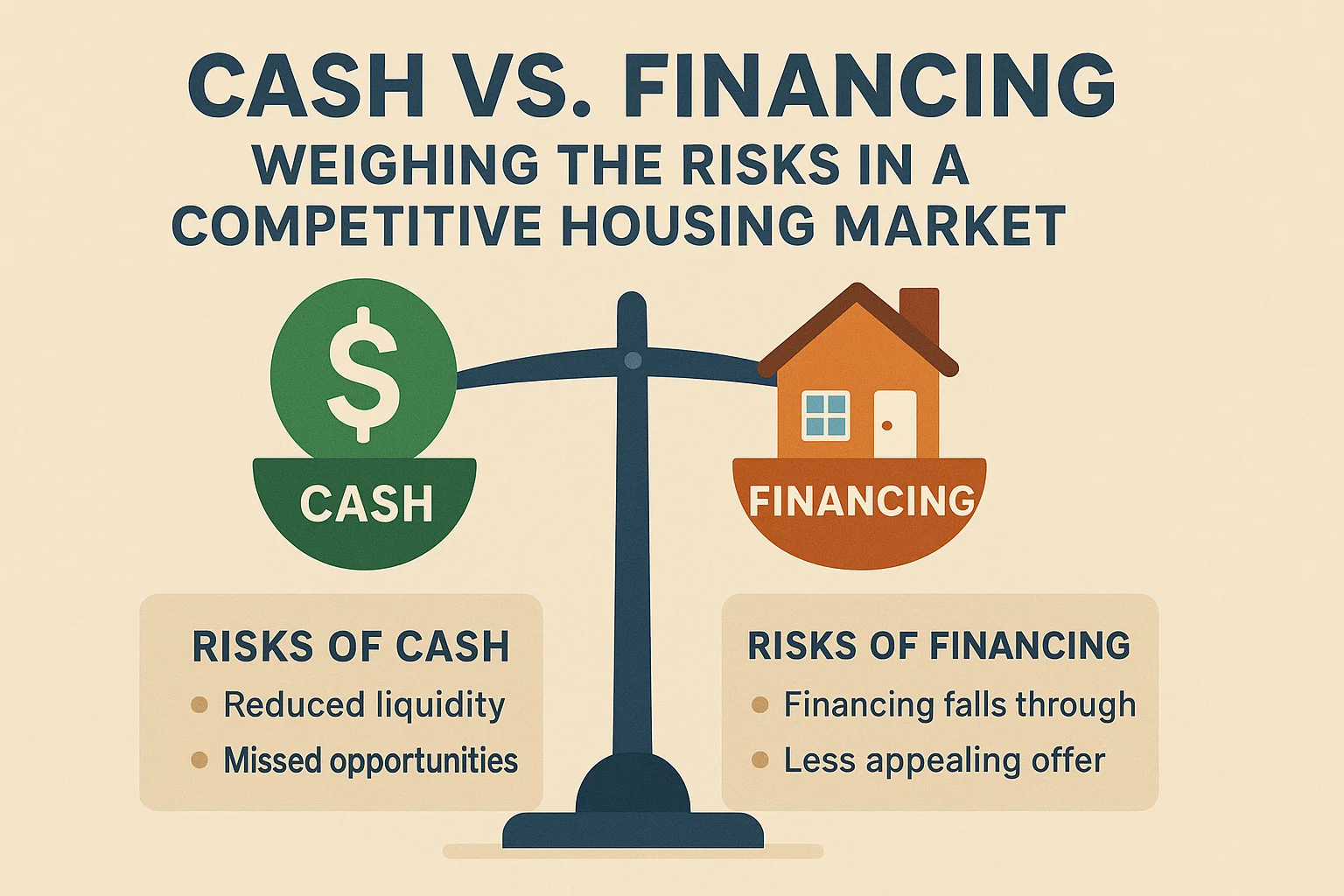

The Surge in Cash Offers

In today’s fast-paced real estate market, cash deals have become a popular tactic for buyers looking to stand out. Recent data shows a significant rise in all-cash purchases, with 30% of U.S. home sales in early 2025 funded entirely by cash—up from 25% the previous year. While cash offers can give buyers an edge, they also come with risks that may outweigh their appeal.

Why Cash Offers Are on the Rise

- Equity from High-Cost Markets: Buyers relocating from expensive areas are leveraging profits from sold properties to purchase homes outright in more affordable regions.

- Rising Home Values: A 14.6% annual spike in home values has boosted equity, enabling sellers to reinvest proceeds as cash buyers elsewhere.

- Stock Market Gains: Strong market performance has left many buyers with excess liquidity to fund primary or secondary homes.

- Speed and Certainty: Cash deals often close faster (as quickly as two weeks) and eliminate financing contingencies, reducing seller risk.

The Hidden Drawbacks of Cash Offers

1. Unexpected Delays

- Fund transfers between accounts can take days or weeks, depending on financial institutions.

- Inspections and title issues may still delay closing, even without mortgage requirements.

- Market volatility can shrink liquid assets, leaving buyers short if relying on stocks or investments.

2. Lack of Investment Diversity

Pouring all available cash into a home ties up wealth in a single asset. Economic shifts, local job losses, or declining property values could jeopardize financial stability.

3. Reduced Liquidity

Cash spent on a home becomes illiquid, limiting emergency funds for unexpected costs like medical bills or unemployment.

4. Lost Tax Benefits

Mortgage interest deductions, which reduce taxable income for loans up to $750,000, are unavailable to cash buyers.

5. Ongoing Monthly Costs

Even without a mortgage, homeowners must budget for property taxes, insurance, and HOA fees—expenses that mimic a monthly payment.

Is a Cash Offer Right for You?

While cash offers streamline transactions and strengthen bargaining power, they require careful financial planning. Consult a lending professional to assess your liquidity, tax implications, and long-term goals before committing. Alternatives like larger down payments or pre-approved mortgages may offer similar advantages without draining your savings.