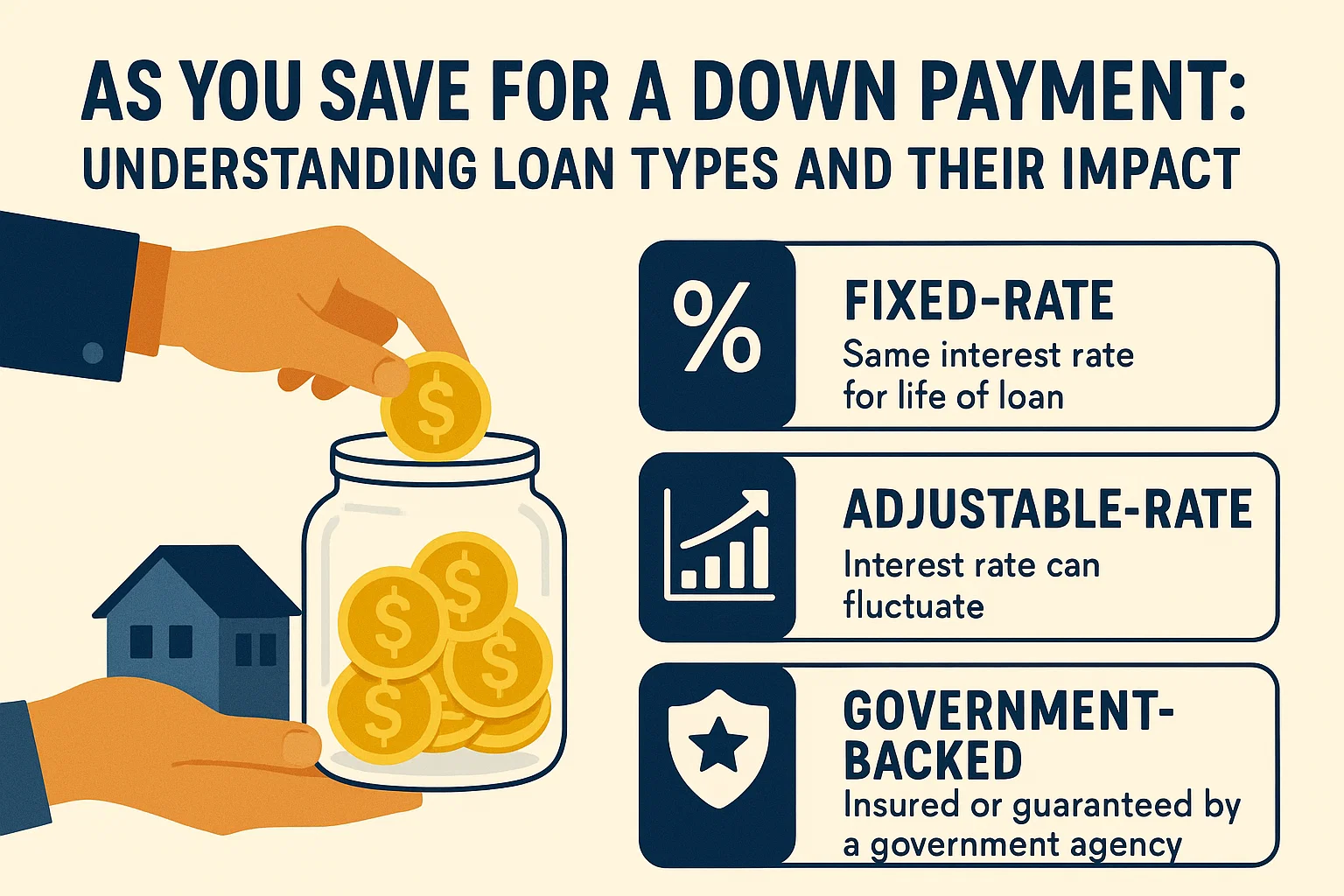

As You Save for a Down Payment: Understanding Loan Types and Their Impact

As You Save for a Down Payment: Understanding Loan Types and Their Impact

As you save for a down payment (you’re totally taking advantage of these saving tips, right?) and get closer to house hunting time, you’ll face big decisions about home loan options. Researching loan types early is critical. Why? While some loans require a 20% down payment, others offer 0% down. Each option has pros and cons: A smaller down payment means higher monthly costs, but for many, that’s easier than saving a large lump sum. The key is to understand how each loan type affects your down payment and monthly mortgage. Let’s break it down!

Understanding Down Payments

A down payment reduces the lender’s risk. The less they loan, the less they lose in a foreclosure. Your down payment is subtracted from the home’s purchase price, and the lender covers the rest. For example, a $90,000 down payment on a $300,000 home leaves a $210,000 mortgage.

Many first-time buyers assume they need 20% down. While 20% secures better terms, it’s not mandatory. However, smaller down payments often require mortgage insurance to protect the lender if you default.

Understanding Mortgage Insurance

Mortgage insurance protects lenders if you stop payments. Here are the common types:

Private Mortgage Insurance (PMI)

- Costs 0.5%–1% of the loan annually.

- Paid monthly and added to your mortgage payment.

- Example: On a $300,000 loan, PMI could add up to $250/month.

Up-Front Mortgage Insurance Premium (UFMIP)

- 1.75% of the loan due at closing.

- Can be paid upfront or rolled into the loan.

- Example: $5,250 UFMIP on a $300,000 loan adds ~$25/month if financed, but costs ~$9,000 over 30 years.

Annual MIP

- 0.45%–1.05% of the loan, paid monthly.

- Example: Adds up to $260/month on a $300,000 loan.

Loan types may require one or a combination of these. Always clarify how they impact your payments.

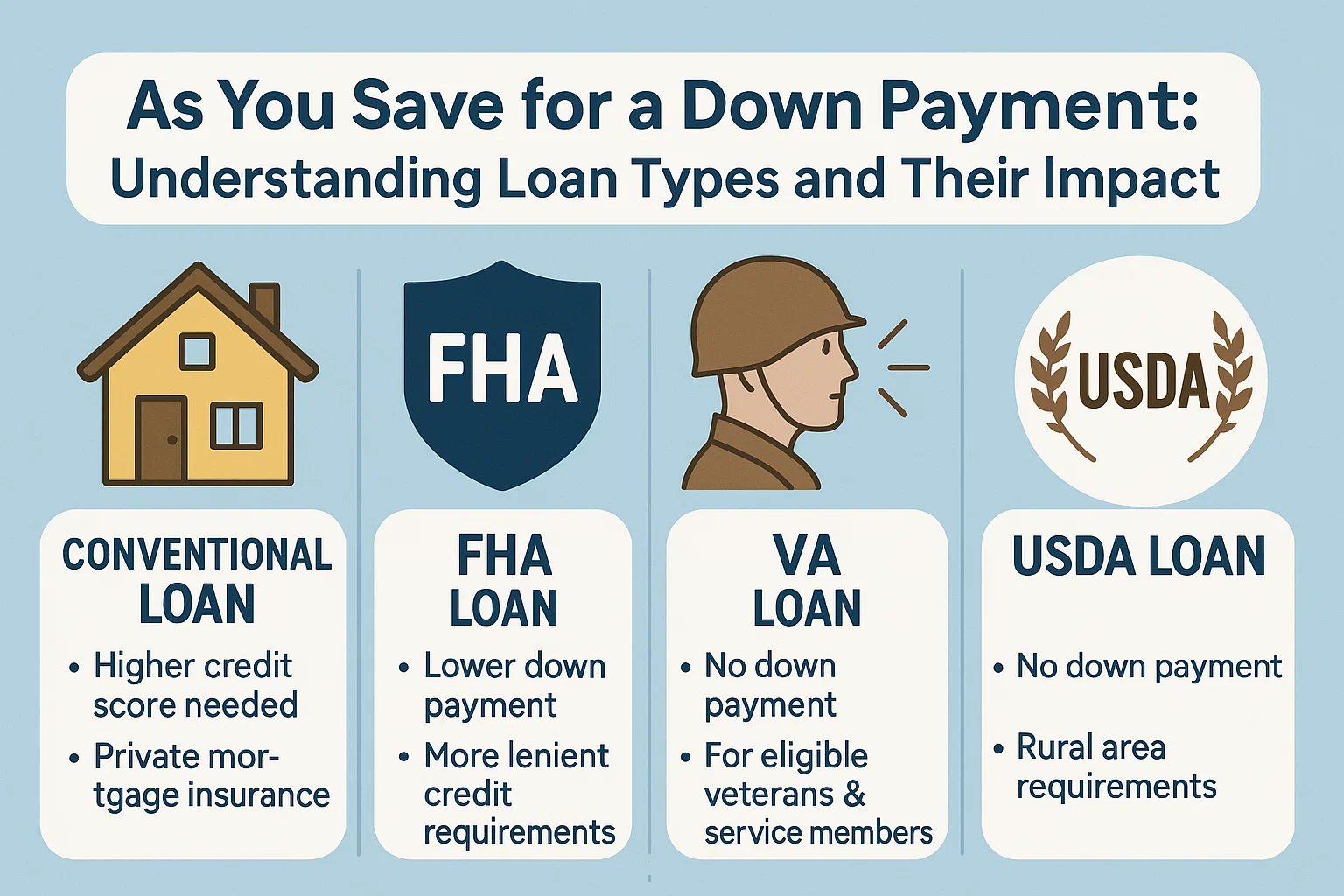

Loan Types Explained

Conventional Loans

- Down Payment: Typically 20% (no mortgage insurance). Lower down payments require PMI.

- Interest Rates: Vary by market, credit score, and optional mortgage points (fees to lower rates).

- Best For: Borrowers with strong credit and savings.

FHA Loans

- Down Payment: 3.5%–10% (based on credit score).

- Requirements: Both UFMIP and annual MIP.

- Best For: First-time or lower-income buyers.

USDA Loans

- Down Payment: 0% (must buy in eligible rural/suburban areas).

- Requirements: 0.3% annual MIP + 1% UFMIP. Income limits apply (≤115% of area median income).

- Best For: Moderate-to-low-income buyers in qualifying regions.

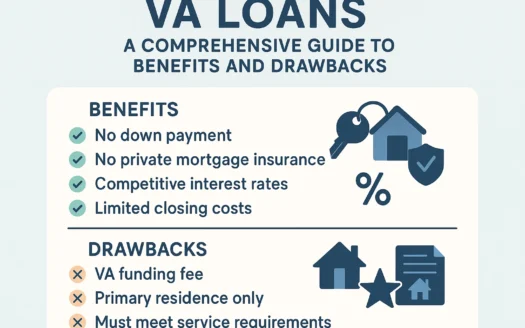

VA Loans

- Down Payment: 0% (no mortgage insurance).

- Eligibility: Veterans/active military members with a Certificate of Eligibility.

- Best For: Qualified service members seeking flexible terms.

Final Tips

Your loan type significantly impacts your down payment and monthly costs. Start researching early to gauge affordability. Ask lenders to “run the numbers” for multiple scenarios—this is a lifelong investment, and clarity is key. Use your lender as a resource to explore options tailored to your financial goals.