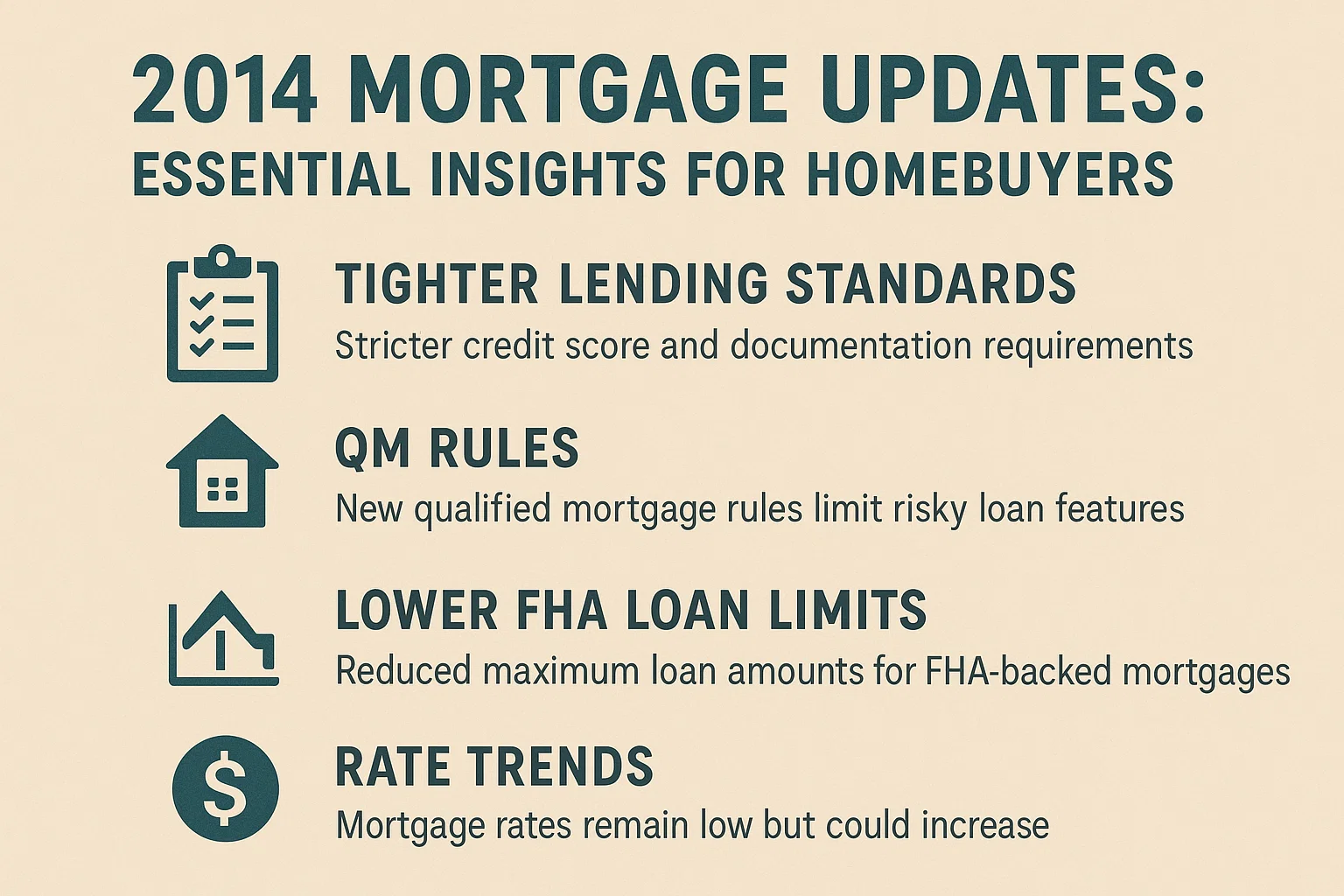

2014 Mortgage Updates: Essential Insights for Homebuyers

2014 Mortgage Updates: Essential Insights for Homebuyers

If you haven’t tracked recent mortgage trends, 2014 has introduced significant changes for homebuyers. New loan limits, eligibility criteria, and financing options may impact your home purchase plans. Here’s what you need to know.

FHA Loan Limits: Key Reductions

Federal Housing Administration (FHA) loans have long been favored for their lower down payments and flexible credit requirements. However, 2014 brought nationwide reductions to FHA loan limits. For example:

- Los Angeles County’s limit dropped from $729,750 in 2013 to $625,500 in 2014.

Homes exceeding these limits now require alternative financing. Consult a loan officer to explore options tailored to your situation.

Exploring Alternative Mortgage Options

Conventional Mortgages

Unlike government-backed loans, conventional mortgages typically require a 5% minimum down payment. They offer flexibility for buyers who no longer qualify for FHA loans.

VA Loans

Eligible military members, veterans, and surviving spouses may qualify for Department of Veterans Affairs (VA) loans. Benefits include:

- No down payment requirements

- No monthly mortgage insurance

Bond and Rural Housing Loans

Local bond programs or USDA-backed rural loans may be available. Discuss eligibility and terms with a mortgage professional.

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-Rate Mortgages

Ideal for long-term homeowners, these loans provide stable payments and immunity to interest rate hikes over the loan’s lifespan.

Adjustable-Rate Mortgages (ARMs)

ARMs offer lower initial rates, benefiting those planning shorter-term ownership. For example, a 5-year hybrid ARM could save money if you sell before the adjustable period begins.

Final Tip: Every buyer’s financial situation is unique. Partner with an experienced loan officer to evaluate rates, terms, and eligibility for your ideal mortgage solution.