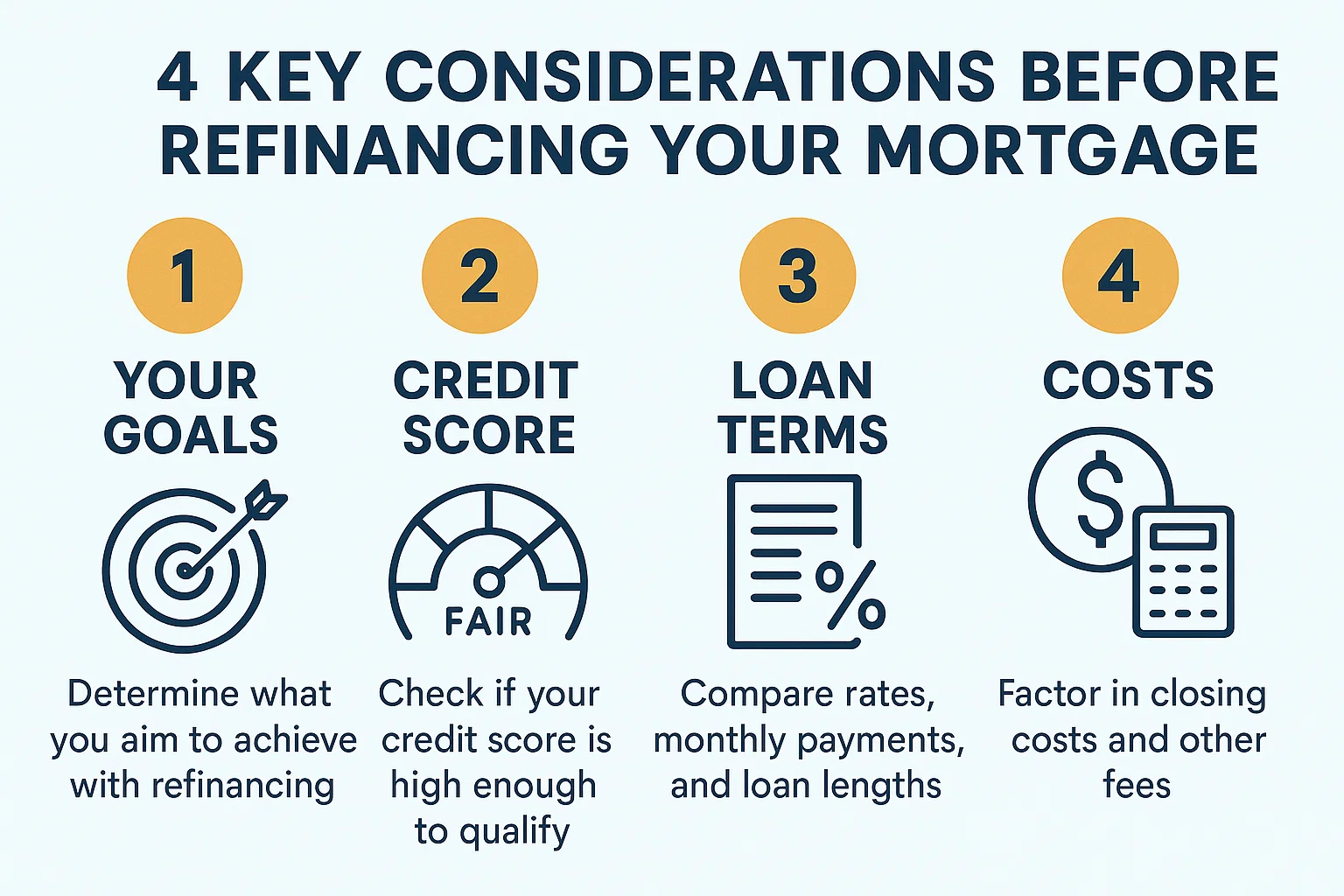

4 Key Considerations Before Refinancing Your Mortgage

4 Key Considerations Before Refinancing Your Mortgage

Deciding whether to refinance your mortgage is a significant financial choice. While securing a lower interest rate might seem appealing, it’s crucial to evaluate your circumstances carefully. Below are four essential factors to weigh before moving forward.

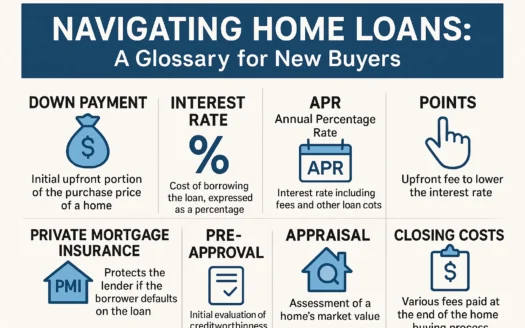

1. Clarify Your Financial Objectives

Reducing monthly payments is the most common reason to refinance. A lower interest rate or improved credit score could help achieve this. However, refinancing can also serve other goals:

- Shortening the loan term: Switching from a 30-year to a 15-year mortgage may align with long-term plans like retirement, but ensure higher monthly payments fit your budget.

- Switching to a fixed-rate loan: Replace an adjustable-rate mortgage (ARM) with a fixed-rate option to eliminate payment fluctuations and gain predictability.

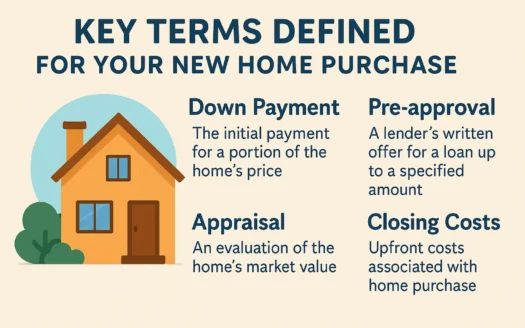

2. Evaluate Closing Costs and Break-Even Point

Refinancing typically involves closing costs ranging from 2% to 5% of the loan amount. Common fees include:

- Appraisal and underwriting fees

- Loan origination charges

- Title/attorney fees

- Escrow reserves and credit report fees

Calculate the break-even period by dividing closing costs by your monthly savings. For example, $5,000 in fees with $250 in monthly savings takes 20 months to break even. If you plan to sell before then, refinancing may not be worthwhile.

3. Assess Your Home Equity

For a cash-out refinance, retain at least 20% equity to avoid private mortgage insurance (PMI). Draining equity risks higher long-term costs and extends your repayment timeline. For instance, refinancing a 30-year loan after withdrawing cash could reset your amortization, adding years of interest payments. If your home’s value has declined, explore alternatives like personal loans instead.

4. Research Lenders and Loan Terms

Compare offers from multiple lenders to find the best rates and terms. Focus on:

- Interest rates and APR differences

- Loan flexibility and prepayment penalties

- Customer reviews and lender reputation

Understanding mortgage fundamentals—such as how amortization works—can help you make informed decisions. Dedicate time to research, as even small rate differences can yield significant savings over time.

By addressing these factors, you’ll be better equipped to decide whether refinancing aligns with your financial goals and current situation.