Understanding Mortgage Rate Locks: Key Considerations for Homebuyers

Understanding Mortgage Rate Locks: Key Considerations for Homebuyers

Is Now the Right Time to Lock Your Rate?

Deciding when to lock in a mortgage rate is a common dilemma for borrowers. Unlike predictable financial decisions, timing a rate lock is akin to navigating stock market investments—there’s no one-size-fits-all answer. Your choice depends on market conditions and personal financial circumstances. For example:

- Well-qualified buyers might delay locking if they anticipate stable or improving rates.

- Borrowers near debt-to-income limits may prioritize locking immediately to avoid disqualification if rates rise.

Consulting a loan officer is critical to assess affordability and weigh the risks of locking versus floating your rate.

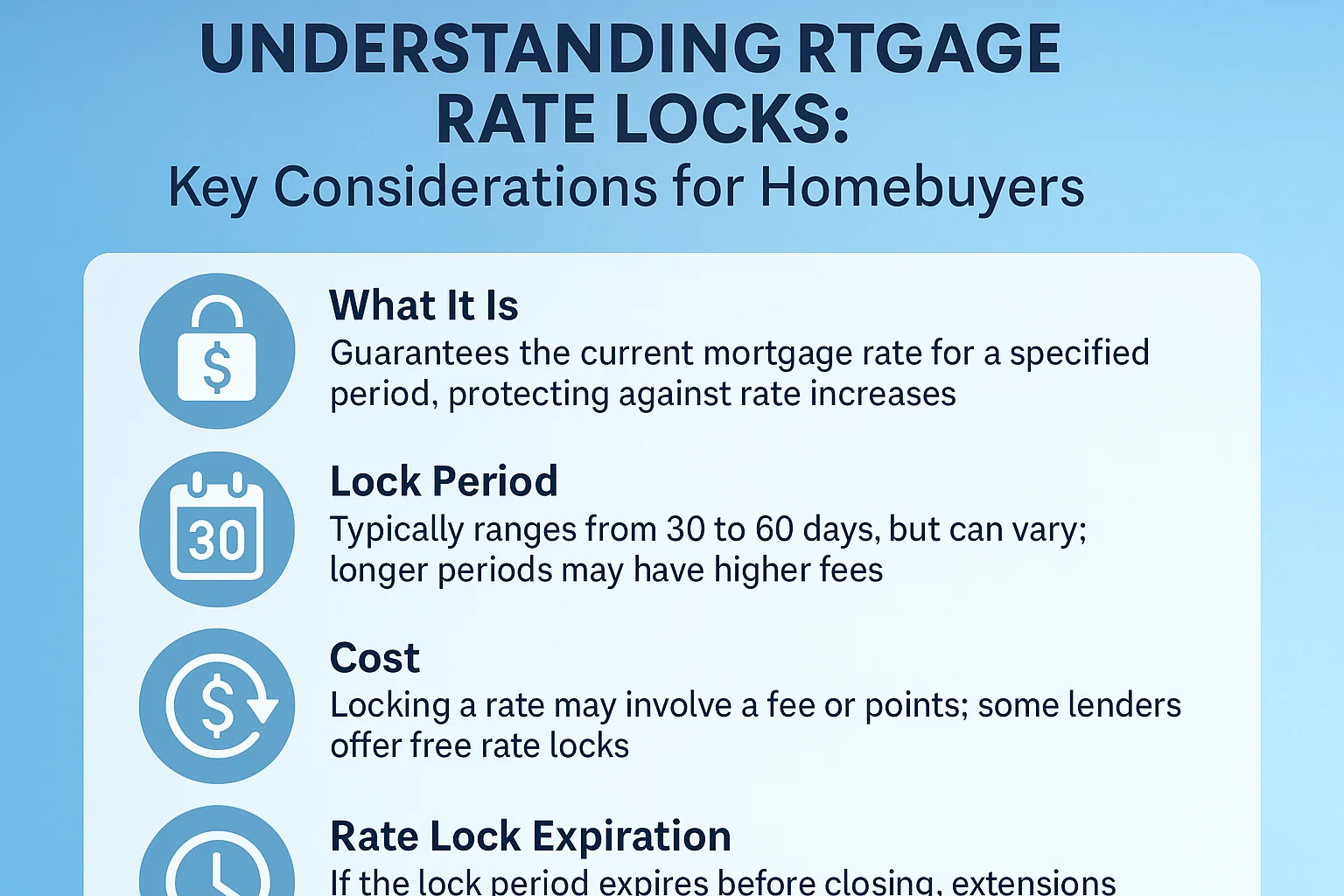

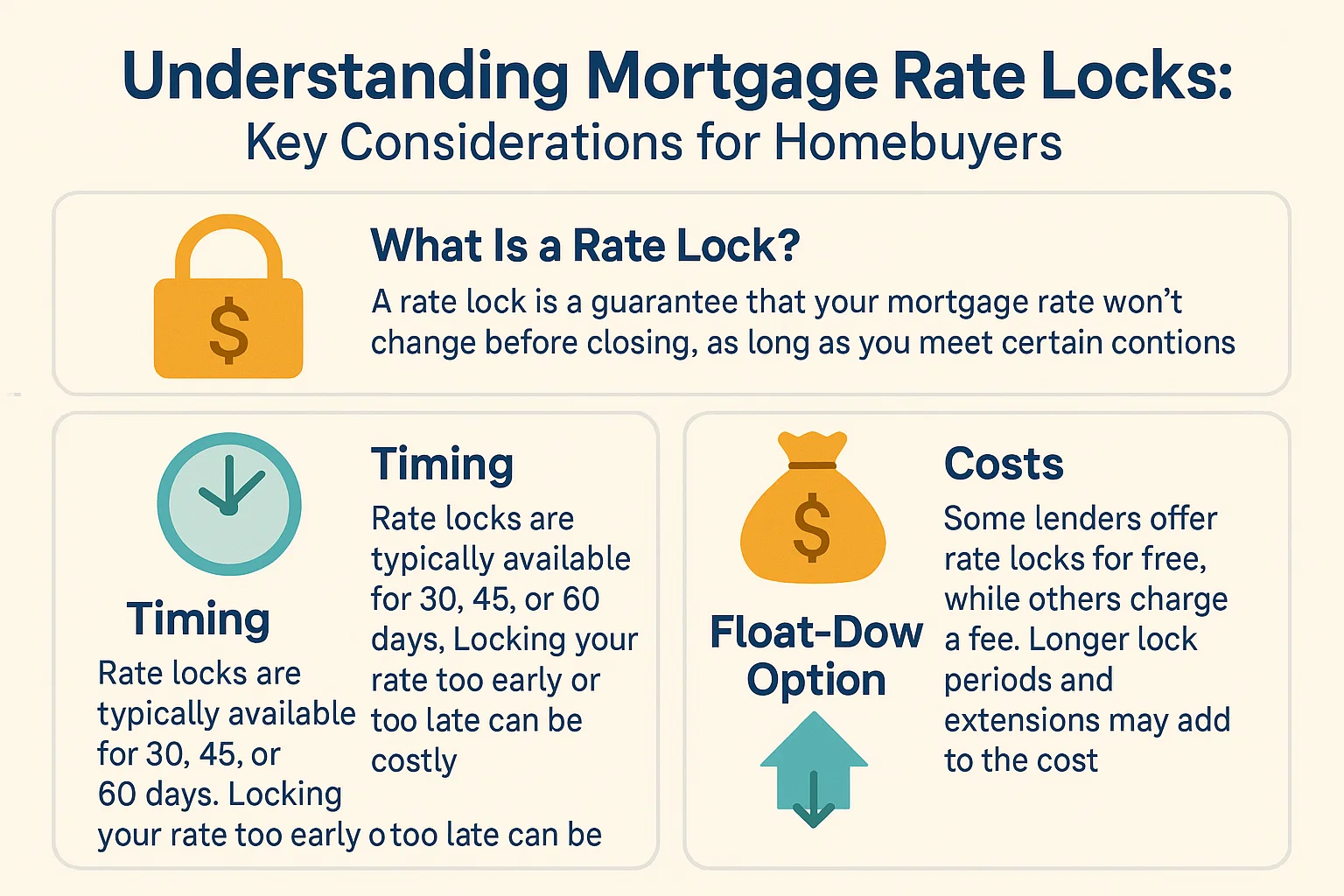

How Mortgage Rate Locks Work

A rate lock formalizes the agreed-upon interest rate, fees, and lock expiration date between borrower and lender. Until locked, the rate remains “floating,” meaning it can fluctuate with market changes. Once locked:

- Your rate stays protected even if market rates increase before closing.

- You won’t benefit from potential rate drops post-lock unless your lender offers a float-down option (more below).

Monitoring Mortgage Rate Trends

Tracking rate movements in the months leading to your mortgage application can inform your strategy:

- Rising rates: Lock early to avoid higher costs.

- Falling rates: Delay locking to capitalize on potential decreases.

While no one can predict rate shifts with certainty, staying informed helps you make educated decisions. Note: Less qualified buyers may need to lock promptly to secure approval.

Float-Down Options: A Middle Ground

Some lenders offer a float-down clause, allowing you to lock a rate while retaining one opportunity to lower it if market rates drop before closing. This feature often comes with an upfront fee, so evaluate its cost against potential savings.

Final Thoughts

The decision to lock your rate is deeply personal, influenced by risk tolerance, financial stability, and market outlook. Work closely with your loan officer to explore lock terms, timelines, and strategies tailored to your goals. By understanding your options, you can confidently navigate the mortgage process.