Demystifying Credit Scores: Ranges, Calculations, and Improvement Strategies

Demystifying Credit Scores: Ranges, Calculations, and Improvement Strategies

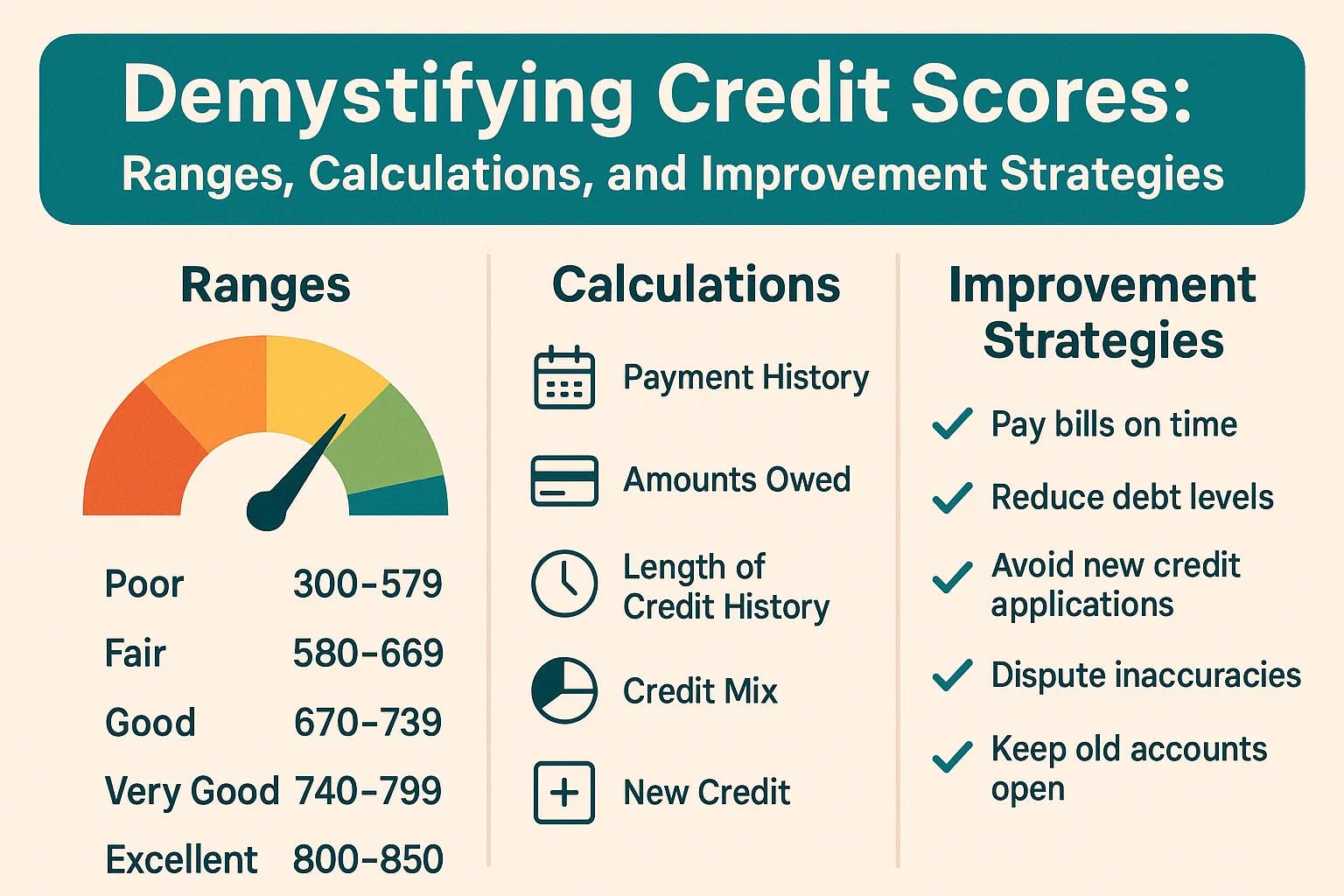

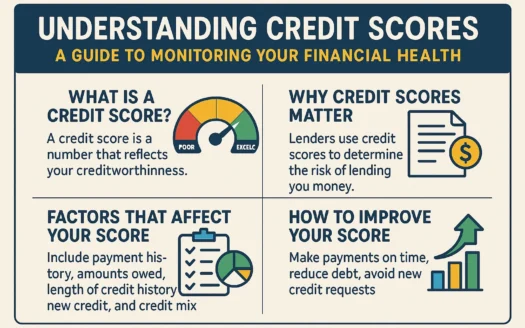

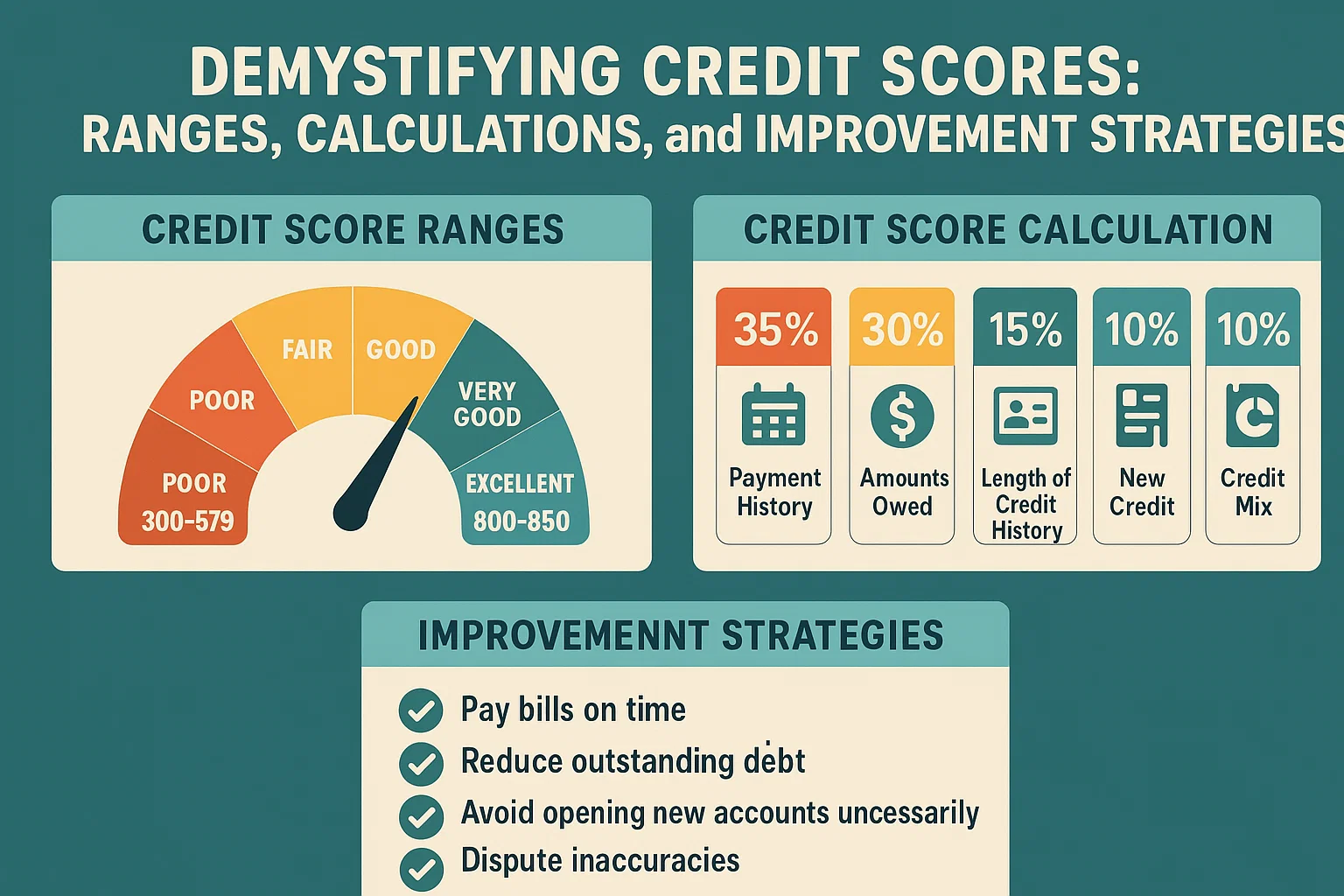

Credit scores play a pivotal role in financial decisions, yet many individuals remain unaware of how they truly work. While the FICO score (ranging from 300 to 850) is the most widely recognized metric, it’s important to note that multiple credit scoring models exist, each with its own unique range. This explains why credit scores may vary across reports—such as consumer reports versus mortgage lender evaluations—depending on the scoring system used.

How Credit Scores Are Calculated

The FICO score, a cornerstone of credit assessment, is determined by five key factors:

- Payment History (35%): Timely payments on loans, credit cards, and bills.

- Credit Utilization (30%): The ratio of current debt to available credit limits.

- Credit History Length (15%): The age of your oldest and newest accounts.

- Credit Mix (10%): Diversity of credit types (e.g., mortgages, credit cards, loans).

- New Credit Inquiries (10%): Recent applications for additional credit.

Proven Habits to Strengthen Your Credit

Improving your credit score requires consistent effort. Follow these actionable steps:

- Pay bills on time, every time: Late payments can significantly damage your score.

- Keep credit utilization below 30%: Aim to use less than one-third of your available credit.

- Avoid frequent credit applications: Multiple hard inquiries within a short period may lower your score.

- Monitor your credit reports: Regularly check for errors and dispute inaccuracies promptly.

Why Credit Health Matters

A strong credit score unlocks opportunities for favorable loan terms, lower interest rates, and smoother approvals for major milestones like homeownership. By understanding how scoring models work and adopting responsible financial habits, you can take control of your credit trajectory and build a more secure financial future.

Key Takeaways:

- Credit score ranges differ across scoring models—FICO is just one example.

- Payment history and credit utilization collectively impact 65% of your FICO score.

- Consistency and patience are critical for long-term credit improvement.