Navigating Family Financial Support for Homeownership: A Comprehensive Guide

Navigating Family Financial Support for Homeownership: A Comprehensive Guide

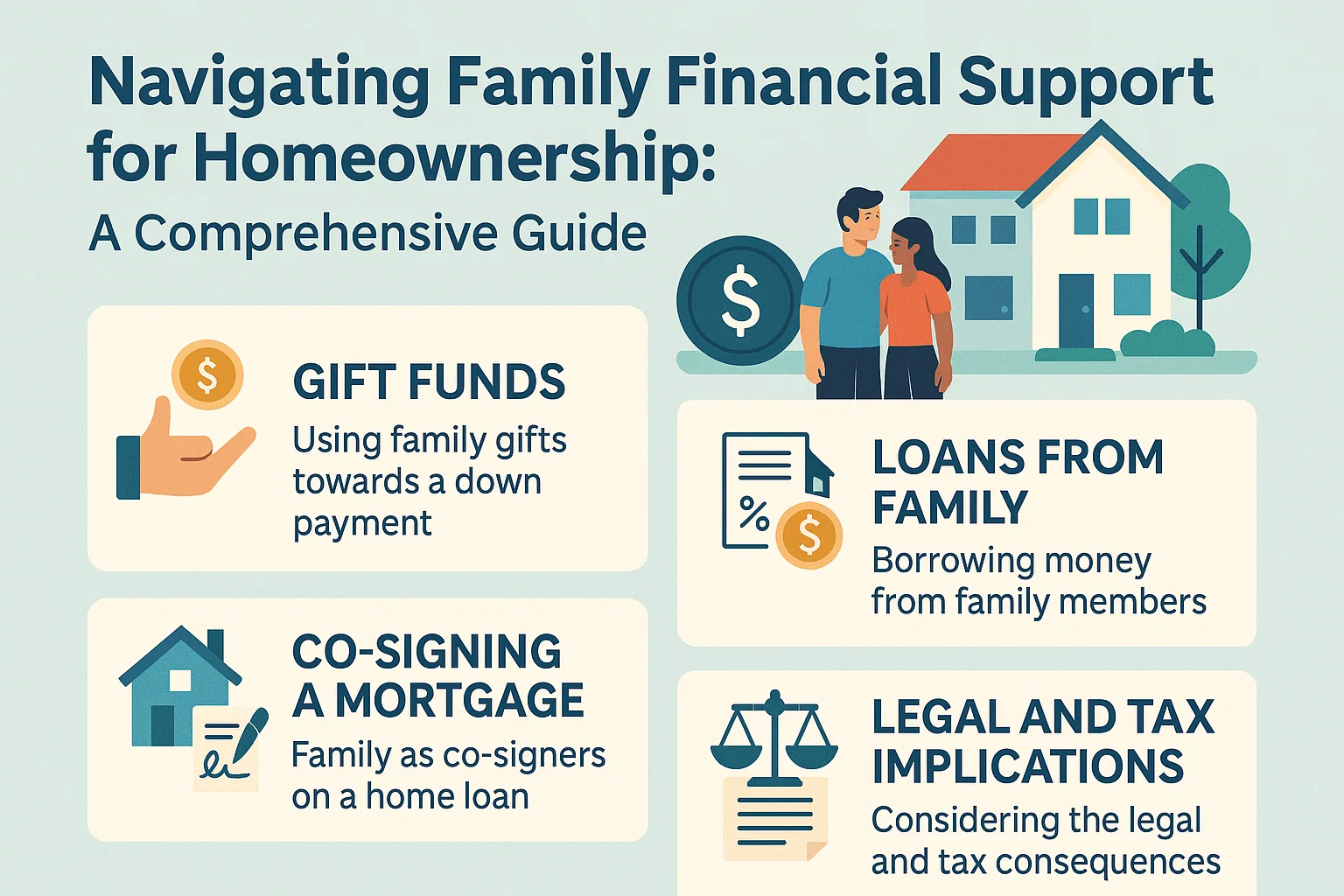

Purchasing a home is a thrilling milestone, but the financial commitment can feel overwhelming. Fortunately, family members can play a pivotal role in easing this burden through monetary gifts. To ensure a smooth borrowing process, clear communication and proper documentation are essential. Below, we outline key guidelines for leveraging family gifts under conventional, FHA, and VA loan programs.

General Guidelines for Gift Funds

- Primary Residences: Gifts from relatives may cover all or part of the required funds.

- Second Homes: Borrowers must contribute at least 5% of the down payment from personal funds, with remaining costs eligible for gift assistance.

Permissible Gift Donors

Donors must fall into one of the following categories:

- Spouse, child, or dependent

- Blood relatives, adoptive family, or legal guardians

- Fiancé(e) or domestic partner

Restrictions on Donors

- Real estate agents may only gift funds to cover closing costs if the gift is part of their commission.

- Donors cannot be affiliated with the builder, developer, or any party with financial ties to the transaction unless a pre-existing familial relationship exists.

Documentation Requirements

A signed gift letter is mandatory and must include:

- Donor’s name, contact information, and relationship to the borrower

- Gift amount and confirmation that repayment is not expected

- Property address (if applicable)

Verifying Gift Funds

- For deposited gifts: Provide donor’s bank statement showing withdrawal and borrower’s statement showing deposit.

- For undeposited gifts: Submit a certified check, cashier’s check, or wire transfer receipt, along with donor’s bank statement proving sufficient funds.

- Important: Cash gifts are not permitted. All funds must originate from a verified bank account.

Loan-Specific Rules

Conventional Loans

- Gift funds may cover down payment, closing costs, or reserves.

- Live-in relatives contributing funds must provide additional documentation, such as proof of residency.

FHA Loans

- Gifts are permitted from approved donors but require thorough documentation.

- No minimum borrower contribution for down payment if gifts cover the full amount.

VA Loans

- Gifts are allowed but prohibited from donors linked to the transaction (e.g., sellers, agents).

- Funds must be transferred to the borrower’s account or provided to the closing agent via certified check.

Final Tips for Success

Family support—financial or otherwise—can make homeownership more attainable. To avoid misunderstandings:

- Clarify expectations upfront regarding repayment and documentation.

- Ensure all parties understand the legal and financial requirements.

By adhering to these guidelines, you can transform family generosity into a seamless path toward homeownership.