Navigating Homeownership After Foreclosure: A Step-by-Step Guide

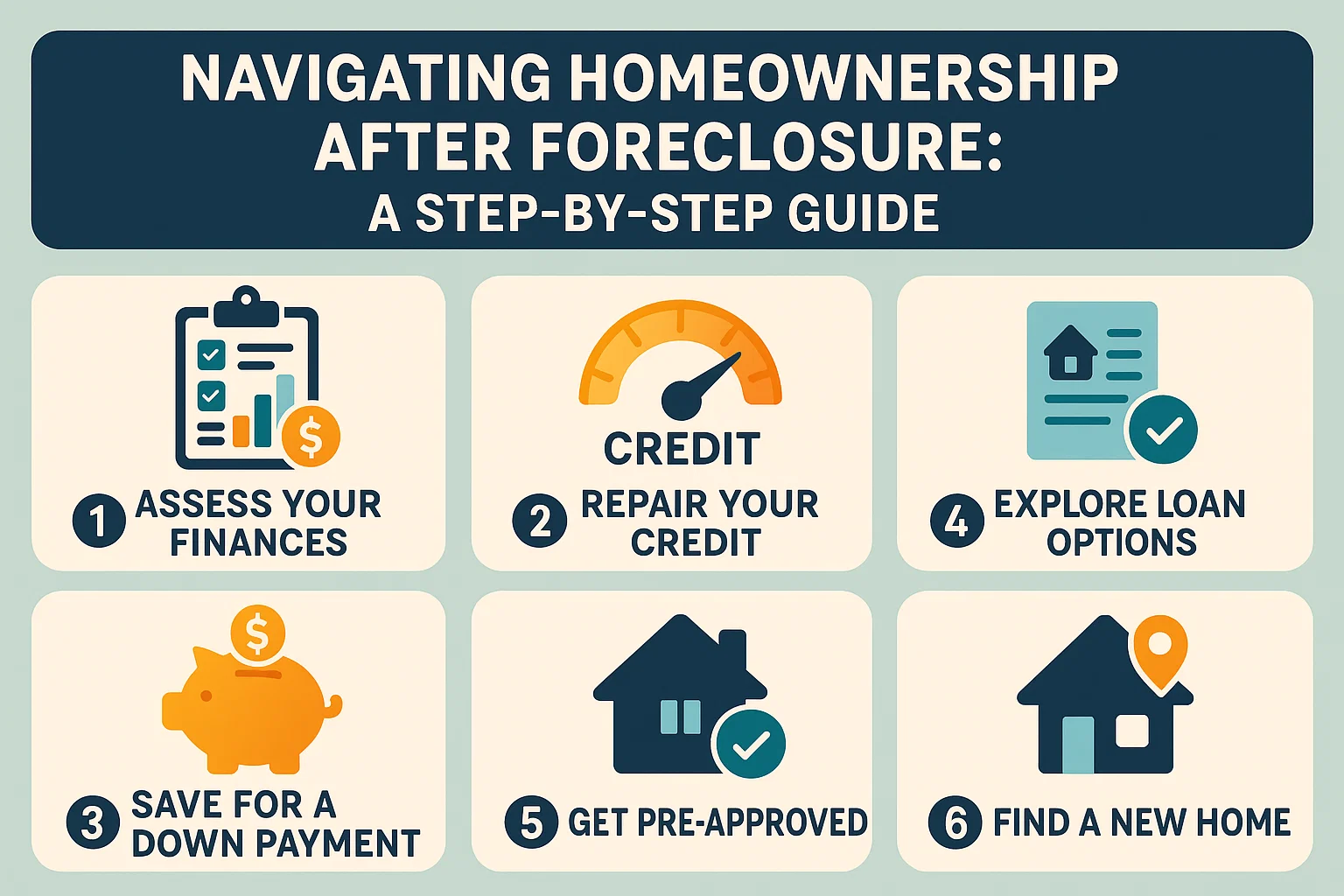

Rebuilding Your Path to Homeownership Post-Foreclosure

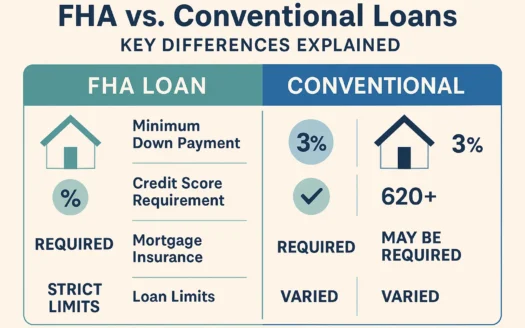

Understanding Lender Waiting Periods

While you may have rebuilt your finances and credit, most lenders require a waiting period before approving a mortgage. Key considerations include:

- Loan type matters: Government-backed FHA loans often have shorter waiting periods compared to conventional loans.

- Timing starts at resolution: Waiting periods typically begin after your foreclosure, bankruptcy discharge, or short sale completion.

- Additional requirements: Be prepared for potential credit score minimums, loan-to-value ratios, or occupancy rules.

Audit and Strengthen Your Credit Profile

Thoroughly review reports from all three major credit bureaus:

- Identify errors like incorrect account statuses or personal information mismatches

- Monitor for fraudulent activity or unresolved debts

- Leverage your annual free credit report access

Address any credit issues systematically to improve your financial standing.

Establish a Realistic Homebuying Budget

Create sustainable financial parameters:

- Limit housing costs to 28-31% of gross income

- Account for variable factors like interest rates and loan terms

- Include insurance, taxes, and maintenance in monthly estimates

Leverage Pre-Qualification Insights

Use lender consultations to:

- Gauge potential loan amounts based on current finances

- Understand different mortgage program requirements

- Refine your home price target and search parameters

Note: Pre-qualification provides estimates, not guaranteed approvals.

Moving Forward with Confidence

By systematically addressing these key areas, you can position yourself for successful homeownership reentry. Stay informed about changing lender requirements and maintain financial discipline throughout the process.