FHA vs. Conventional Loans: Key Differences Explained

FHA vs. Conventional Loans: Which Is Right for You?

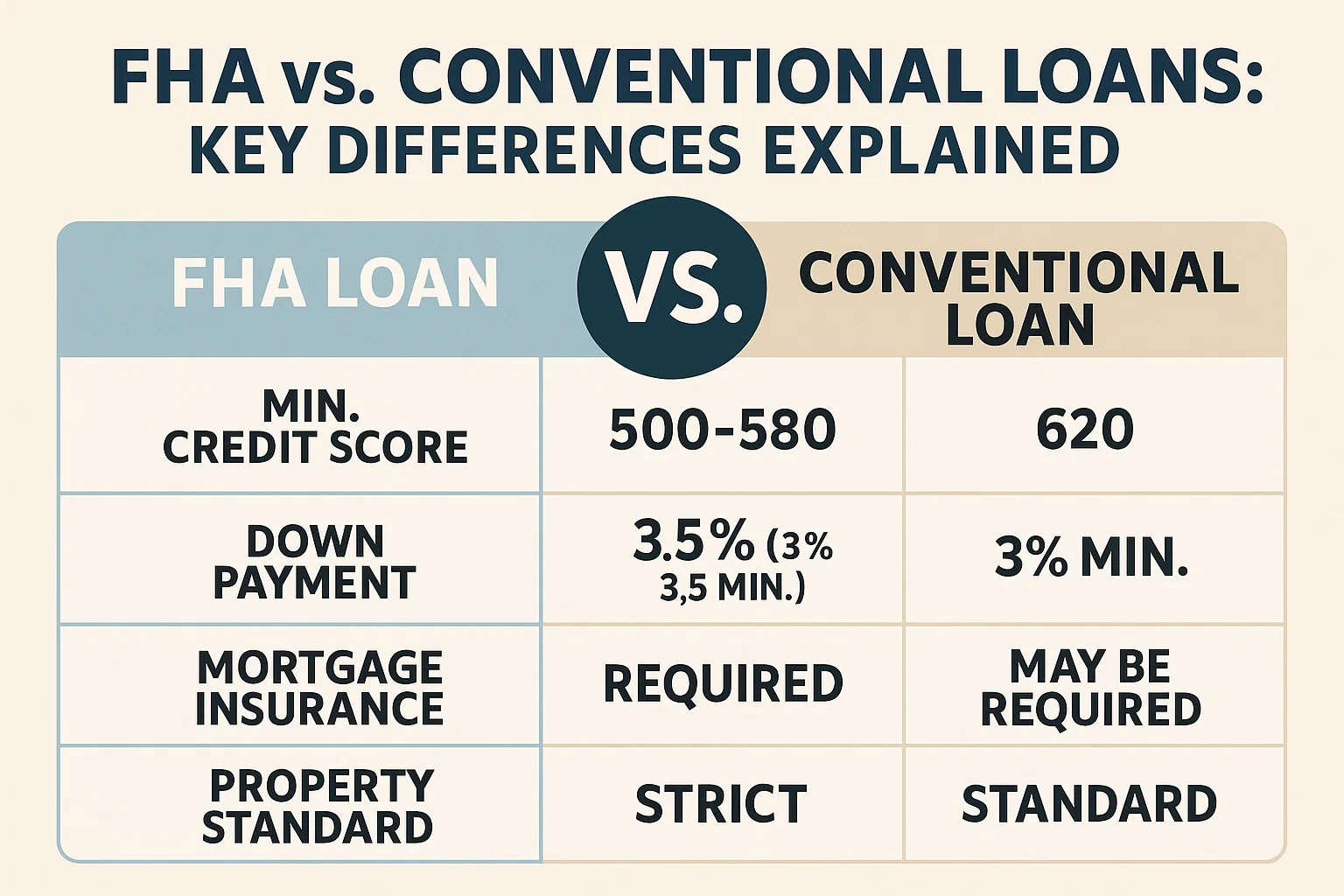

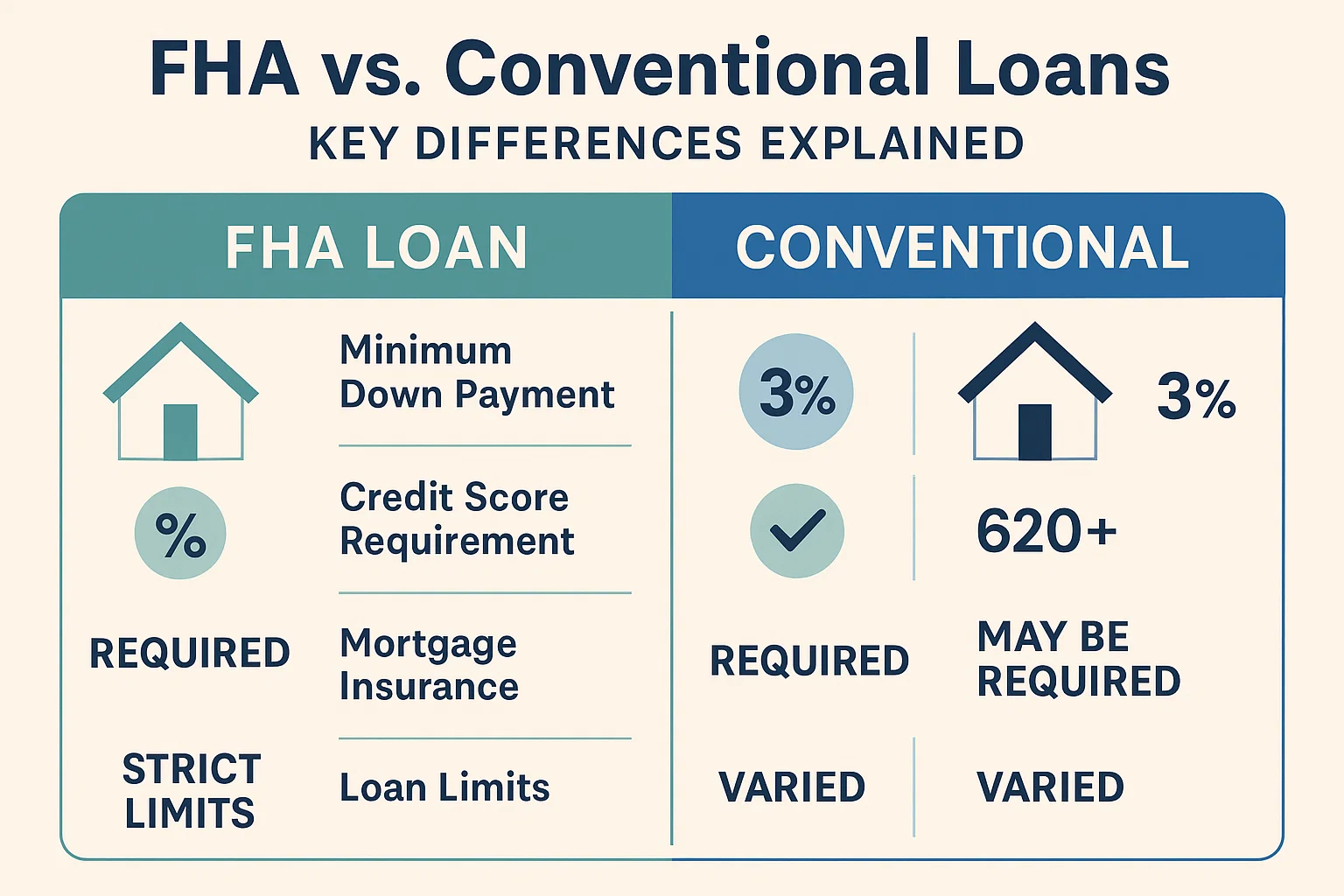

When exploring mortgage options, the Federal Housing Administration (FHA) and conventional (conforming) loans are two of the most popular choices. While both serve the same purpose, their features cater to different financial situations. Let’s break down the critical distinctions to help you decide.

Credit Score Flexibility

FHA loans are often more accessible for borrowers with lower credit scores. If your score is below 620, an FHA loan may be your only viable option, as conventional loans typically require higher credit thresholds.

Down Payment Requirements

Historically, conventional loans demanded a 20% down payment, but this standard has evolved. Today, some conventional loans allow lower down payments than FHA options. However, putting 20% down (if possible) still offers advantages like avoiding private mortgage insurance (PMI).

Interest Rates and Costs

FHA loans usually offer slightly lower interest rates compared to conventional loans, though the difference can vary with market conditions. Where conventional loans pull ahead is in mortgage insurance:

- FHA loans: Require Mortgage Insurance Premiums (MIP) for the entire loan term if the down payment is less than 10%.

- Conventional loans: PMI can be canceled once you reach 20% equity, saving borrowers long-term costs.

Key Takeaways

- FHA loans are ideal for lower credit scores or smaller upfront savings.

- Conventional loans offer more flexibility for higher-credit borrowers and better long-term savings on insurance.

- Compare both options based on your financial profile and long-term goals.

Note: Mortgage insurance rates typically range from 0.5% to 1.0% of the loan amount annually.