Credit Score - Get your Credit Report

With ____ you can instantly get your credit scores from all 3 major credit bureaus! Select the ‘Get my free score!’ button below to get started.

Do you know what your credit score is?

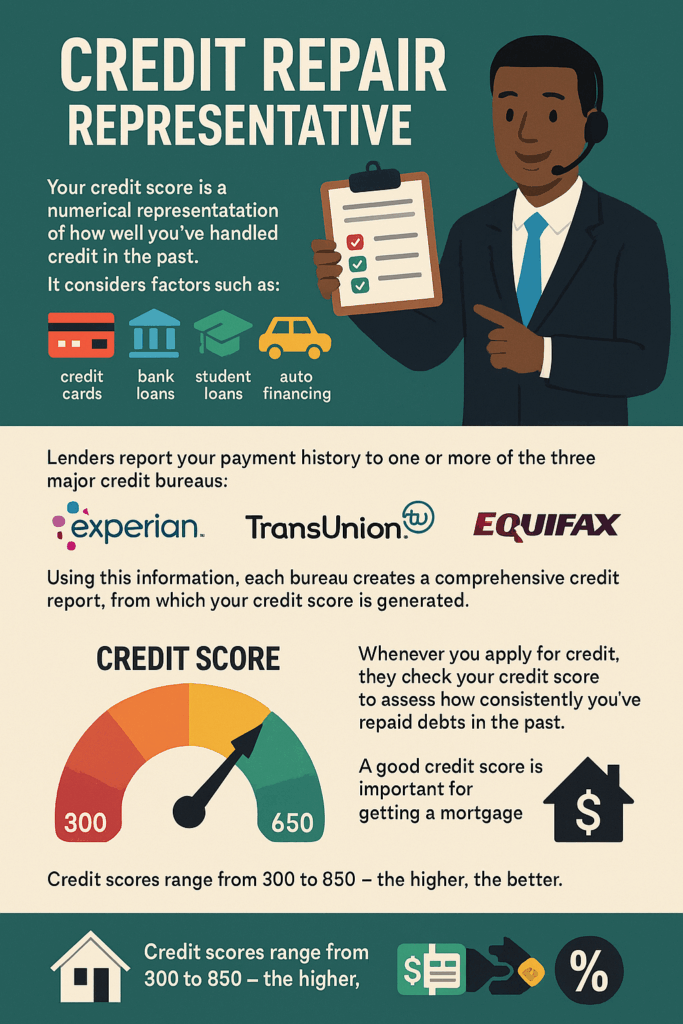

Your credit score is a number that represents how well you’ve done with credit in the past. It looks at credit cards, bank loans, student loans, auto financing and other credit products. Lenders report your payment history to one or more of the three major credit bureaus—Experian, TransUnion and Equifax. Each bureau uses this information to create a credit report and from that, your credit score. Since lenders update your payment history every month, your credit report is refreshed every month and your credit score fluctuates.

When you apply for credit from banks, credit card companies or other financial institutions, they check your credit score to see how consistently you’ve paid debts in the past. A good credit score is especially important if you’re applying for a mortgage as it helps lenders determine if you can manage borrowed money and if you’re likely to default on your loans. Your credit score plays a big role not only in getting a mortgage but also in getting a good interest rate.

Credit scores range from 300 to 850—the higher the better. Use the FreeScore360 tool on this page to check your credit score from all three major credit bureaus for free.

Need to fix your credit?

We have partnered with a top tier credit repair company to get quick results needed to get you approved.

Credit Score FAQS

Lenders determine how much they’re willing to lend by evaluating your finances, including your income, credit score, debt-to-income ratio, down payment, and the terms of your loan.

If you want to borrow more than the calculator suggests or your pre-qualification amount, increasing your income, saving for a larger down payment, or lowering your debt can help boost your borrowing capacity.

While lenders focus on key fixed expenses, homebuyers should also consider additional costs like childcare, travel, and lifestyle, as well as their financial stability and comfort level with managing debt.

Lenders often follow a general rule of thumb: no more than 28% of your gross monthly income should go toward housing expenses, and your total debt, including your mortgage, should not exceed 36%.

New vs Used Homes

Mortgage Calculator