Debunking 4 Common Refinancing Myths Holding Homeowners Back

Debunking 4 Common Refinancing Myths Holding Homeowners Back

You’ve likely heard that refinancing can save homeowners thousands—so why aren’t more people exploring this option? Misconceptions about refinancing often discourage homeowners from taking the plunge. Let’s dismantle four widespread myths and uncover why they shouldn’t hold you back.

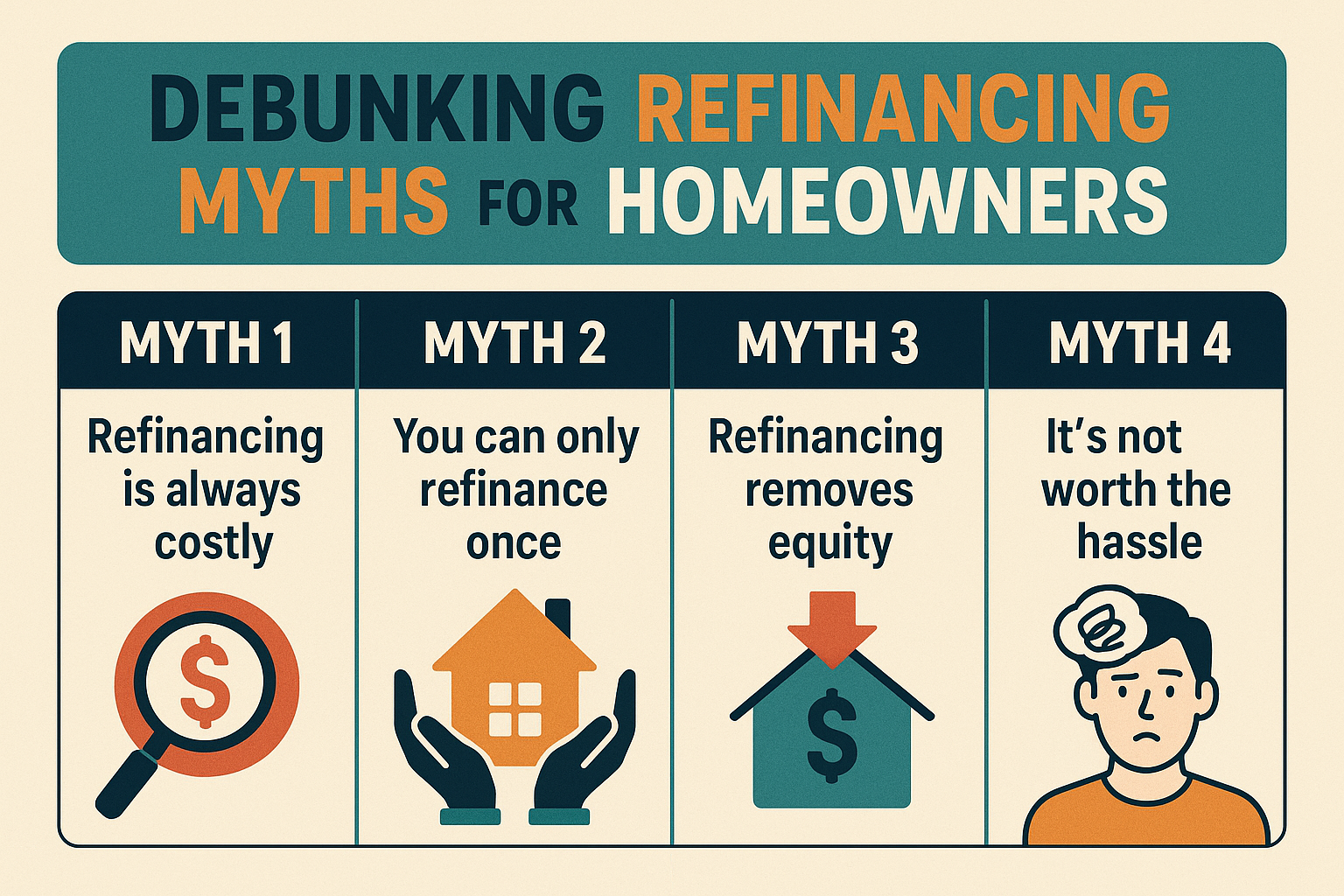

Myth 1: “Rising Interest Rates Mean It’s Too Late to Refinance”

While the Federal Reserve’s rate hikes might make refinancing seem less appealing, they don’t automatically disqualify you from savings. The key is to calculate the costs of refinancing against your potential monthly savings. If the math works in your favor, refinancing remains a smart financial strategy—even in a shifting rate environment.

Myth 2: “You Need Perfect Credit to Qualify”

Though lenders tightened requirements after the 2008 housing crisis, the market has evolved. Today, more options exist for borrowers with less-than-ideal credit. Instead of assuming you’ll be rejected, consult a mortgage expert to explore programs tailored to your financial situation.

Myth 3: “Refinancing Is Too Complicated”

Yes, refinancing involves paperwork and steps like appraisals or income verification. However, working with a trusted lender can streamline the process. Many institutions offer simplified workflows, and the effort often pays off in long-term savings.

Myth 4: “The Savings Aren’t Worth It”

Even a modest reduction in your monthly payment can add up over time. For example, saving $100 a month amounts to $6,000 over five years. Combine this with potential benefits like shorter loan terms or fixed-rate stability, and refinancing becomes a compelling option for many.

Don’t Let Myths Dictate Your Financial Choices

Refinancing isn’t a one-size-fits-all solution, but dismissing it based on rumors could cost you. By evaluating your unique circumstances and partnering with a knowledgeable advisor, you can make an informed decision that aligns with your goals.