Understanding the Hidden Factors That Influence Your Credit Score

Understanding the Hidden Factors That Influence Your Credit Score

When it comes to your credit score, some rules are straightforward—others are less obvious. For instance, while avoiding multiple credit applications is common advice, many people don’t realize that closing existing accounts—even those with zero balances—can harm their credit health. Here’s why.

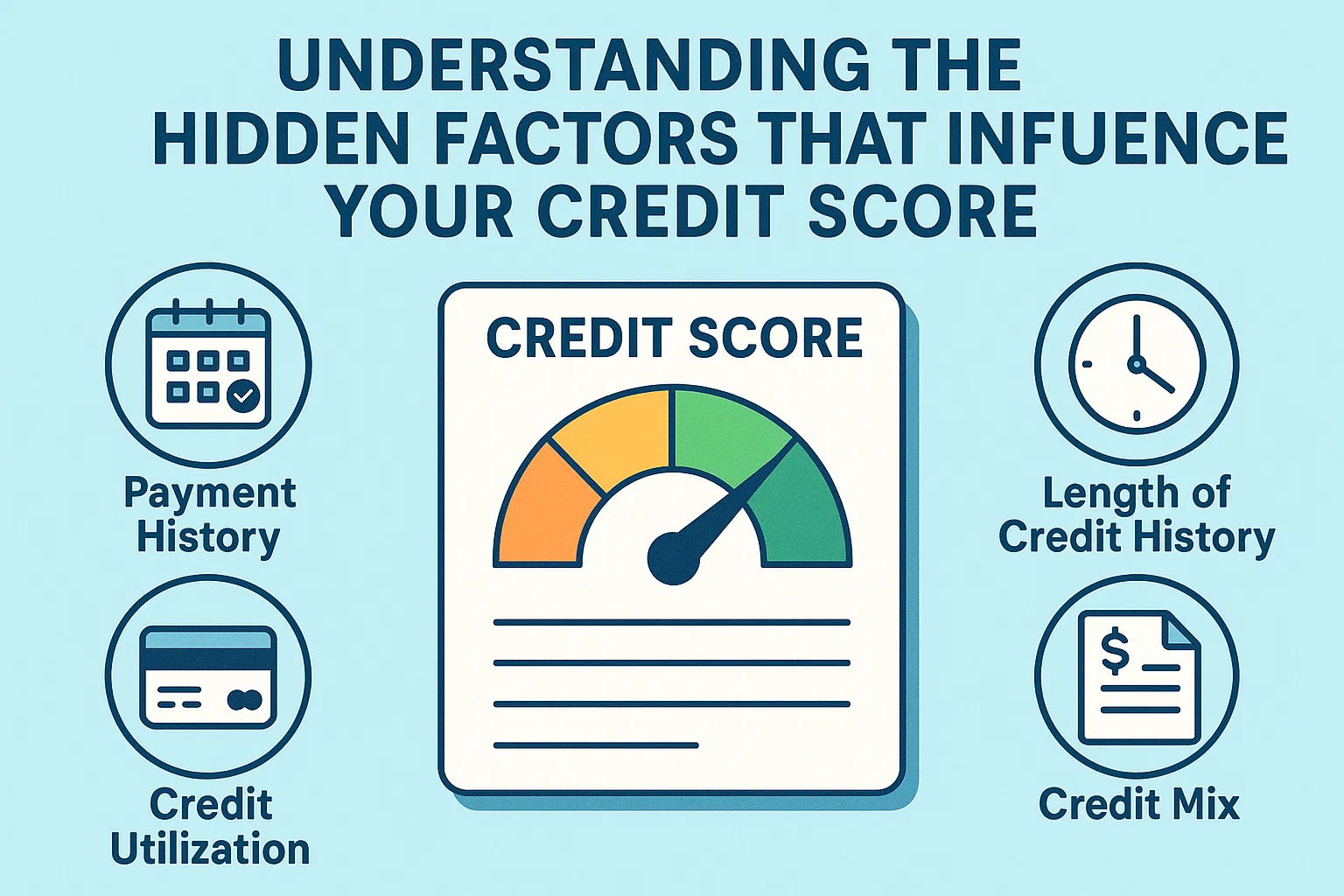

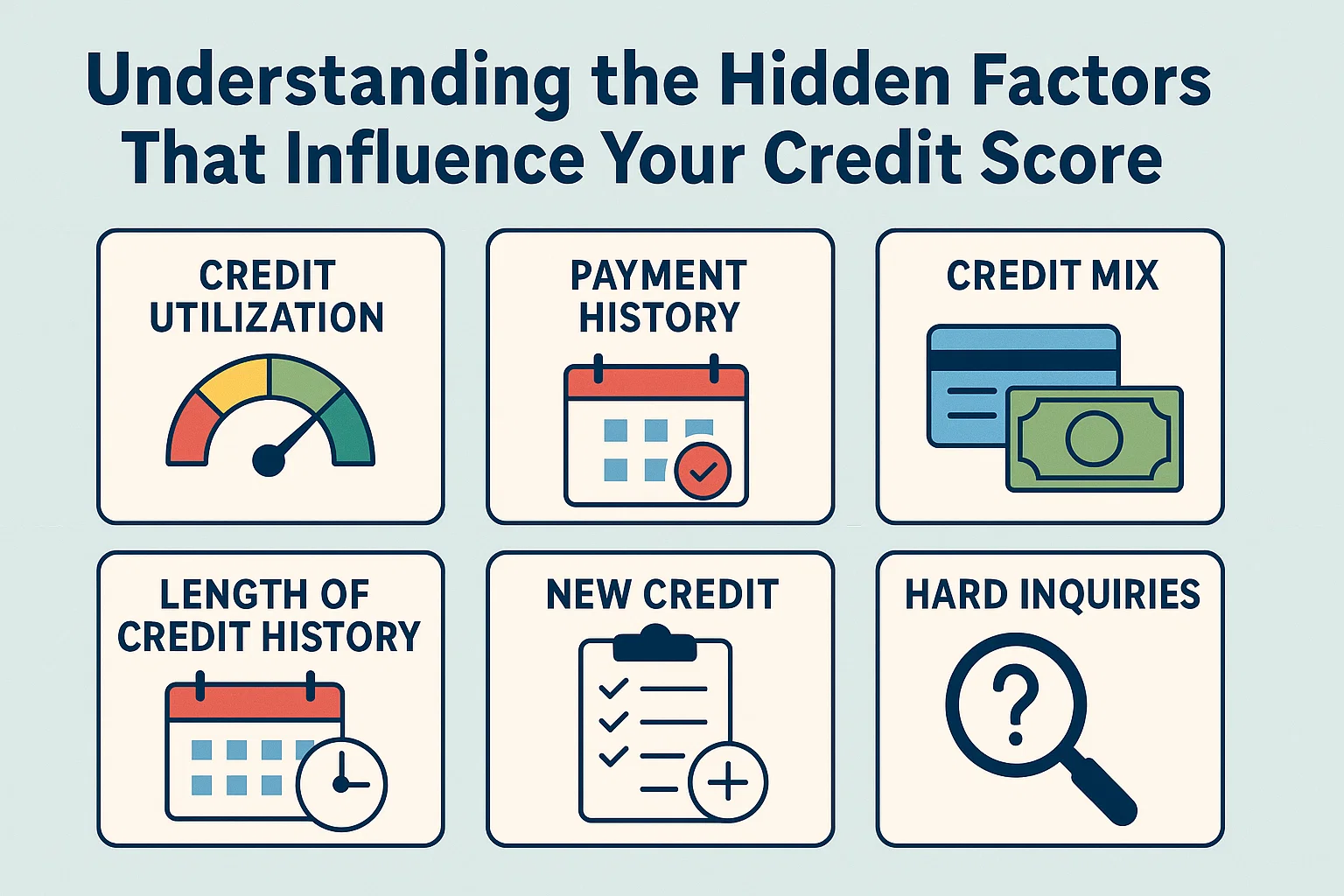

Why Credit History Length Matters

Lenders assess your reliability as a borrower by examining the length of your credit history, which contributes to 15% of your credit score. Closing long-standing accounts shortens this history, making you appear riskier to creditors. Even inactive accounts play a role in demonstrating your financial track record.

The Critical Role of Credit Utilization

Another key factor is credit utilization—the ratio of your debt to available credit. Lower utilization rates (ideally below 30%) signal responsible credit management. For example:

- If you have 4 credit cards with a $10,000 total limit and a $1,500 balance, your utilization is 15%.

- Closing two unused cards (removing $5,000 of available credit) raises your utilization to 30%.

This sudden jump could negatively impact your score, even if your spending habits remain unchanged.

Navigating Credit Score Complexities

Credit scoring formulas can be confusing, but understanding these hidden factors is crucial for maintaining a healthy score. Consulting with credit professionals can provide personalized strategies to optimize your financial profile and avoid common pitfalls.