When to Consider Refinancing Your Mortgage: Key Factors to Evaluate

When to Consider Refinancing Your Mortgage: Key Factors to Evaluate

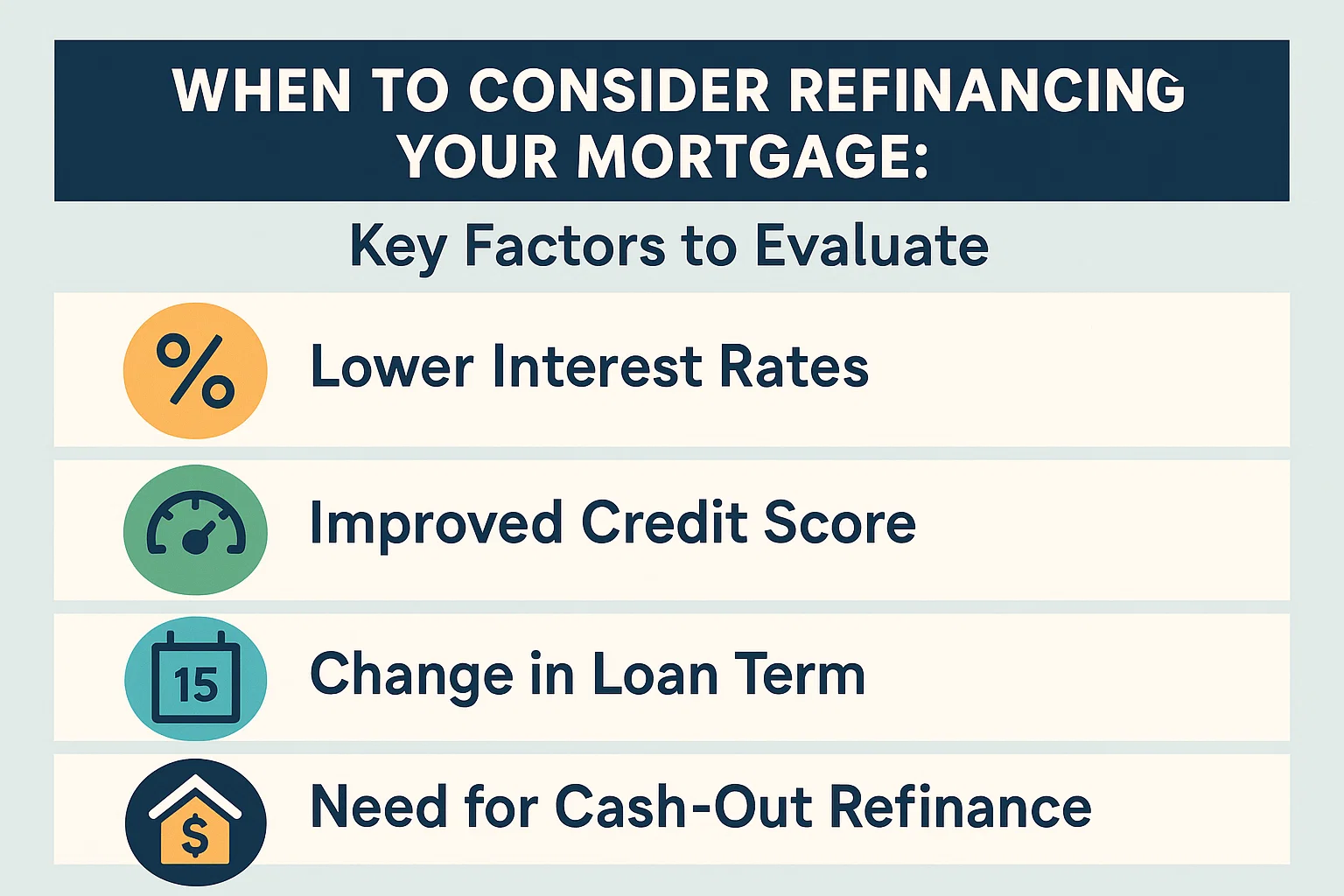

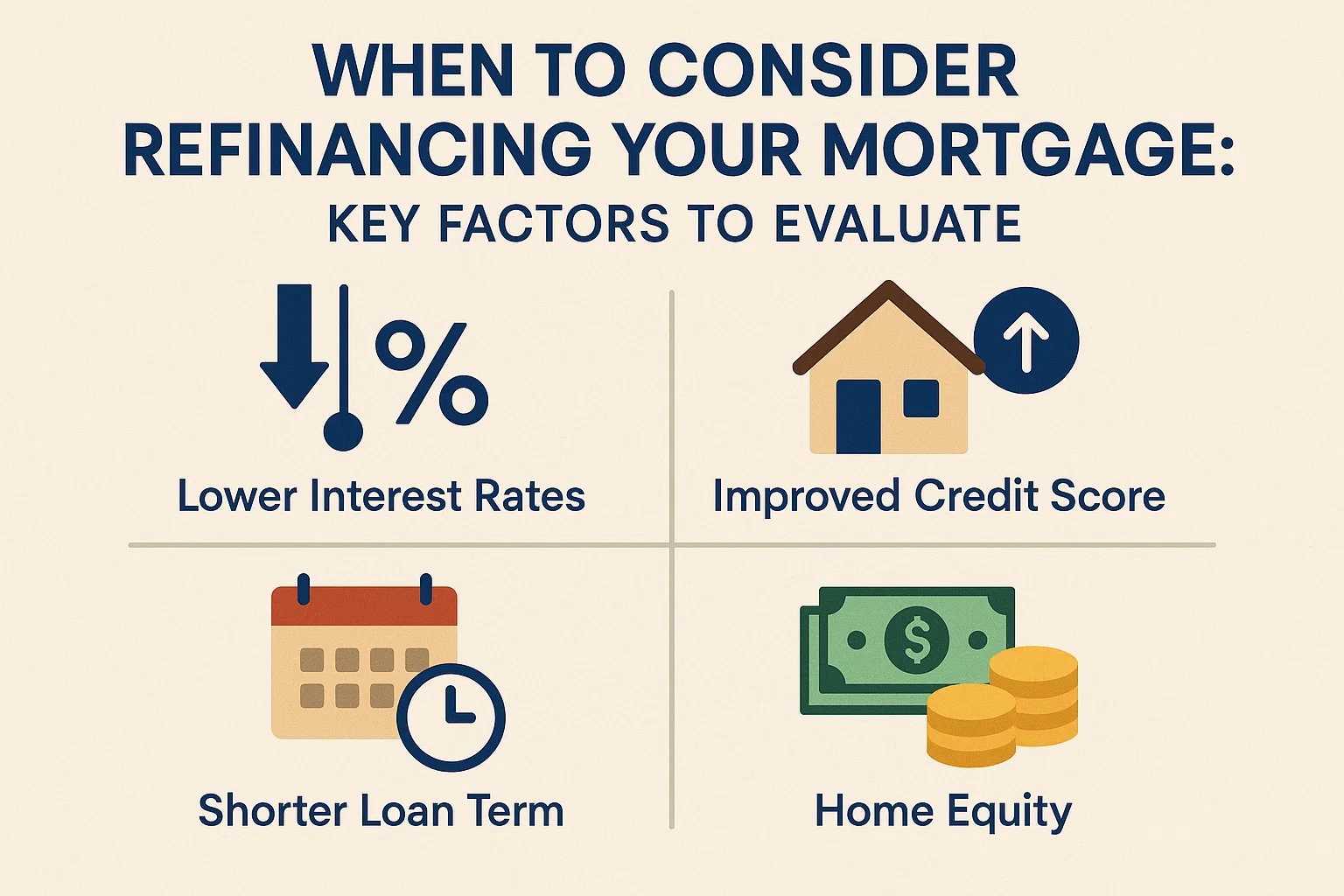

A super-low interest rate can be tempting—lowering your rate might reduce your monthly payment significantly. However, refinancing comes with costs, typically ranging from 2% to 5% of the loan amount. To determine whether refinancing is worthwhile, consider the following factors to ensure you can recoup your expenses over time.

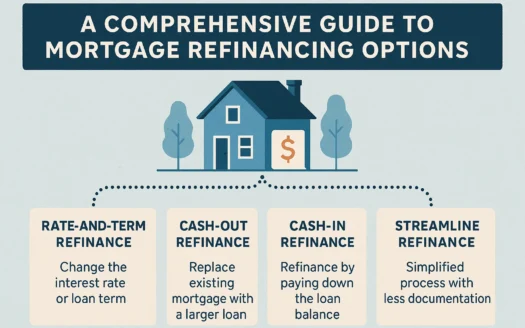

Eliminating Private Mortgage Insurance (PMI)

Homebuyers who purchase a home with less than 20% down usually pay for PMI. Refinancing can help remove this cost if your home’s value has increased enough to give you at least 20% equity. For example, if you initially put down 10% and your home’s value has appreciated by 15%, you may now qualify to drop PMI. Note that some loans require a seasoning period (often two years) before refinancing is allowed.

Switching from an Adjustable-Rate Mortgage (ARM)

ARMs offer low fixed rates for an initial period (typically 5 or 7 years) before adjusting to current market rates. If interest rates are rising, refinancing to a fixed-rate mortgage (e.g., 20- or 30-year terms) can provide stability and long-term savings.

Reducing Interest and Shortening Loan Terms

Refinancing from a 30-year to a 20-year mortgage can save tens of thousands in interest over the loan’s lifespan. This is ideal if your financial situation has improved—such as paying off debt, securing a higher income, or boosting your credit score—to qualify for better rates.

Assessing Your Timeline

Since refinancing costs take time to recoup (often several years), it’s critical to evaluate your plans. If you anticipate relocating or selling soon, the upfront fees may outweigh the savings.

Key Takeaways

- Remove PMI: Refinance if home appreciation boosts equity to 20%.

- Lock in fixed rates: Secure stable payments before an ARM adjusts.

- Shorten loan terms: Save on interest with a stronger financial profile.

- Evaluate break-even timing: Ensure you’ll stay in the home long enough to offset closing costs.

With economic shifts influencing mortgage rates, refinancing could offer financial flexibility, lower stress, or faster debt repayment. Consult a mortgage professional to explore options tailored to your goals.