Understanding Escrow in Home Buying: A Comprehensive Guide

Understanding Escrow in Home Buying: A Comprehensive Guide

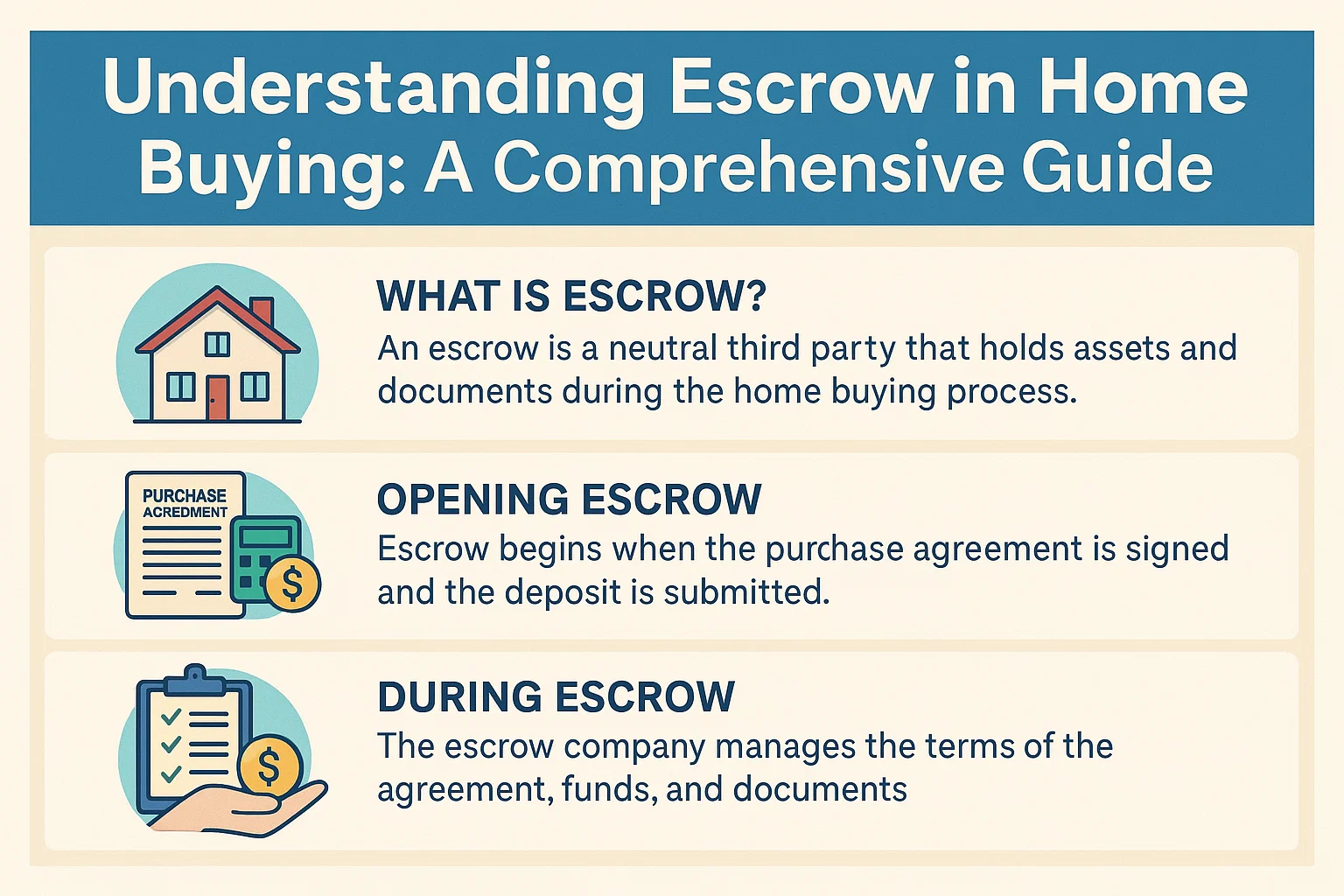

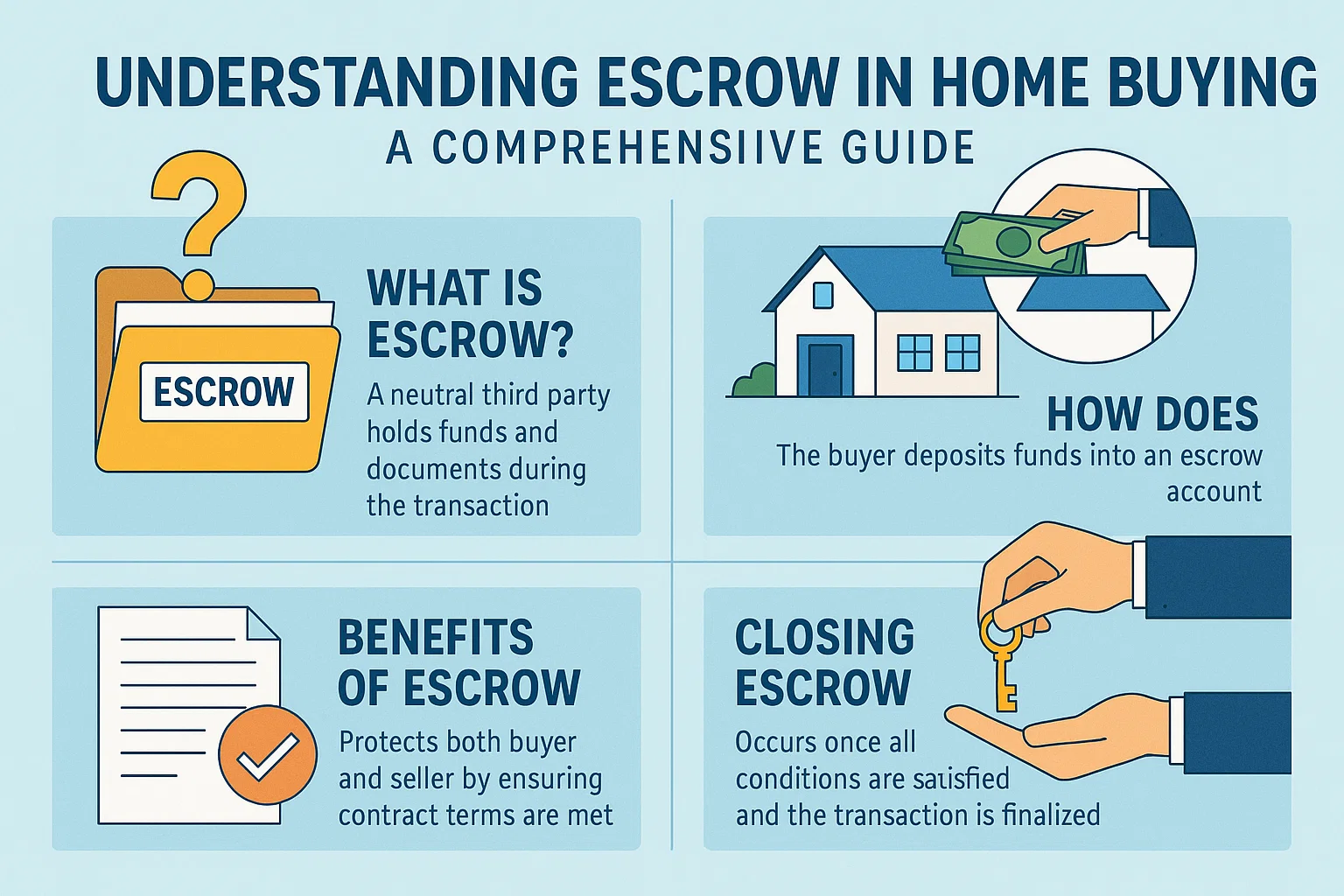

What Is Escrow?

Escrow refers to funds set aside during a home purchase to protect both buyers and sellers. This financial arrangement is managed by a neutral third party and plays a critical role at multiple stages of the transaction.

Earnest Money and Escrow

When making an offer on a home, buyers typically provide earnest money to demonstrate commitment. This deposit is held in escrow until the sale progresses. Key points include:

- Buyer Protection: Once the offer is accepted, the seller must pause active listings and cannot entertain other offers.

- Contingencies: Contracts often include clauses (e.g., inspection failures) allowing buyers to withdraw without penalties.

- Seller Protection: If a buyer backs out without a valid reason, the seller retains the earnest money.

Closing of Escrow

The closing of escrow finalizes the home purchase. This occurs when:

- All funds are disbursed correctly.

- Legal documents are signed and recorded.

- All contractual conditions are met.

Mortgage Escrow Accounts

After purchasing a home, an escrow account may be used to manage recurring expenses like property taxes and insurance. Here’s how it works:

- Monthly Contributions: Lenders divide annual tax and insurance costs into smaller monthly payments.

- Example: If annual taxes are $2,000 and insurance is $1,000, you’ll pay $250 monthly into escrow.

- Automatic Payments: The lender uses escrow funds to pay bills when they’re due, eliminating lump-sum stress.

Annual Escrow Re-Evaluation

Escrow accounts are reviewed yearly due to potential changes in:

- Property tax rates.

- Home insurance premiums.

- Home value fluctuations.

Even with a fixed-rate mortgage, your monthly payment may adjust slightly based on escrow requirements. Lenders will notify you of any changes in advance.