Understanding Your Loan Estimate: A Comprehensive Guide

Understanding Your Loan Estimate: A Comprehensive Guide

During the mortgage application process, federal regulations require lenders to provide a Loan Estimate to help you understand the terms and costs of your loan. This document must be delivered to you within three business days of submitting your mortgage application. While lenders may adjust the design for branding, all Loan Estimates are mandated to include the same core information. Below, we break down the key sections to help you navigate this important document.

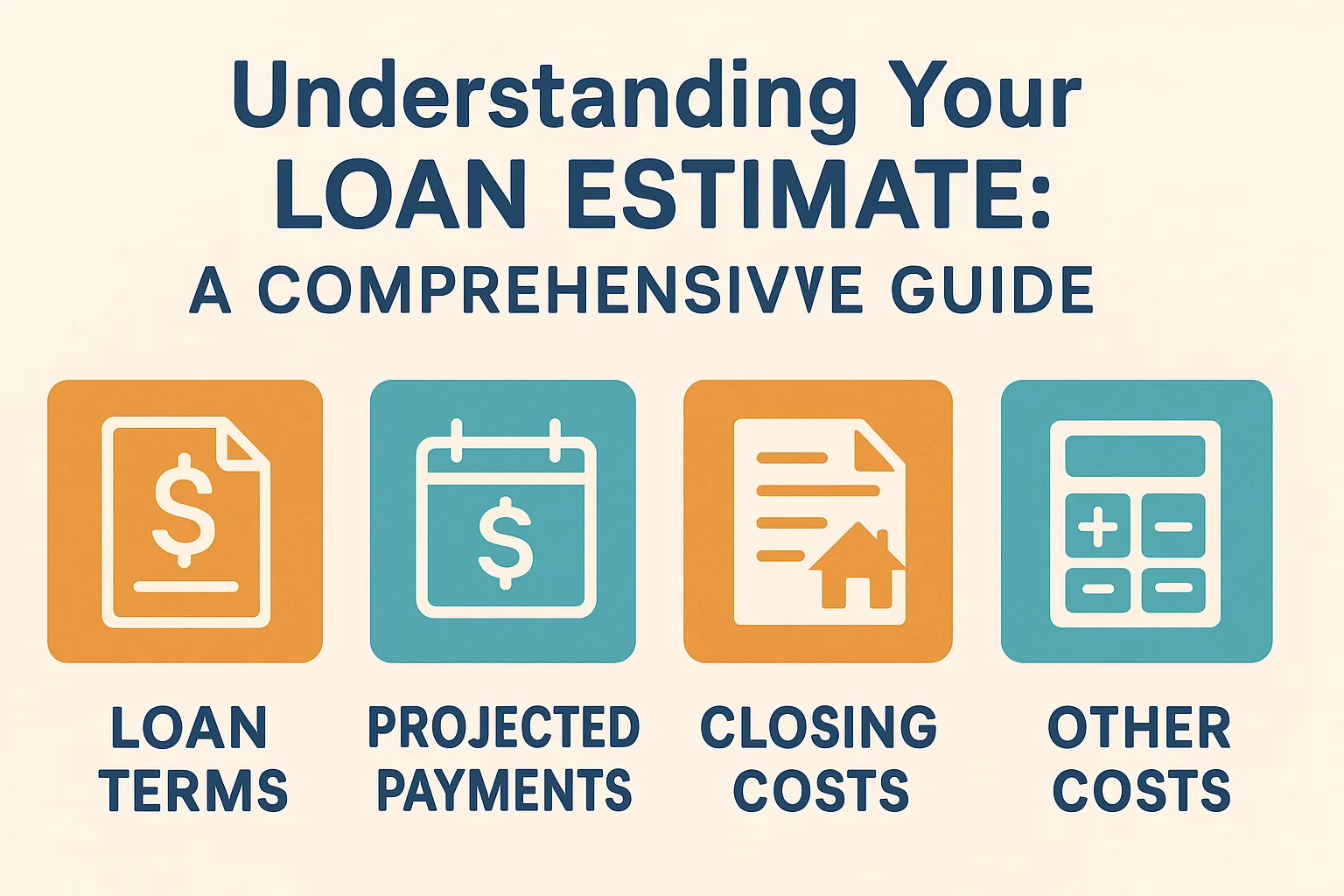

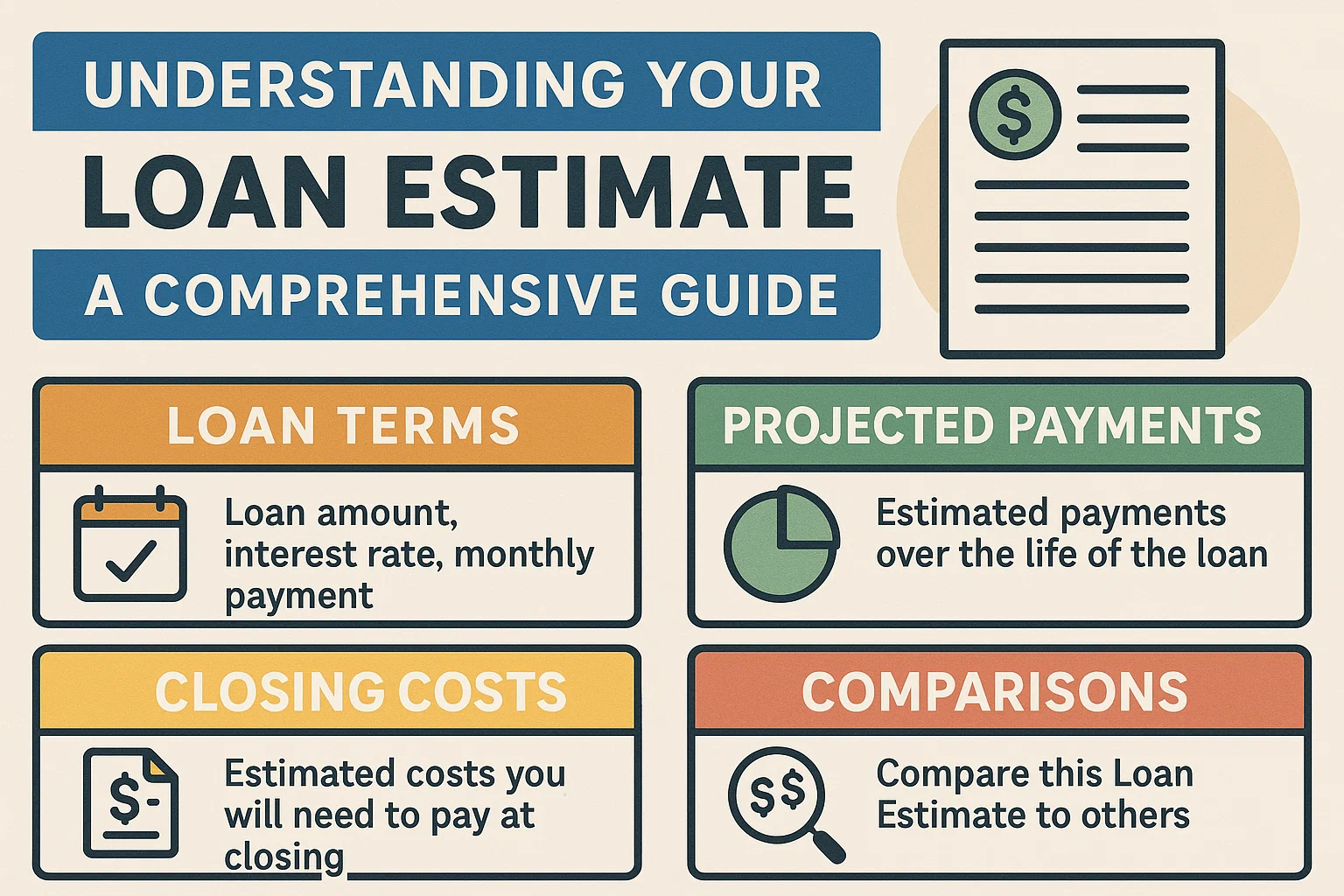

Key Sections of Your Loan Estimate

1. General Loan Information

The top of the Loan Estimate includes basic details such as:

- Your name and contact information

- The property address and sale price

- The loan type, purpose, and term

- Rate lock expiration date (if applicable)

2. Loan Terms

This section outlines critical loan details, including:

- Loan amount

- Interest rate

- Monthly principal and interest payments

- Prepayment penalties or balloon payments (if any)

3. Projected Payments

Here, you’ll see a breakdown of your estimated monthly payments, covering:

- Principal and interest

- Mortgage insurance

- Escrowed property taxes and insurance

4. Closing Costs

This portion summarizes upfront fees, such as:

- Origination charges

- Appraisal or credit report fees

- Title insurance and other third-party services

5. Additional Disclosures

Important comparisons and warnings are highlighted here, including:

- Total interest percentage over the loan term

- Late payment policies

- Escrow account requirements

Why This Matters

The Loan Estimate empowers you to compare offers from multiple lenders and make informed decisions. Review each section carefully and ask questions about unclear terms or fees. By understanding this document, you can confidently move forward with your mortgage application.