Understanding Home Loans: A Comprehensive Guide to Mortgage Options

Understanding Home Loans: A Comprehensive Guide to Mortgage Options

Basic Requirements to Qualify for a Mortgage

Before diving into loan types, here are the key requirements most lenders expect:

- Proof of income (pay stubs, tax returns)

- Proof of assets or funds (bank statements, investment accounts)

- Credit score (minimum varies by loan type)

- Employment verification

- Government-issued ID and Social Security card

While a credit score of 760+ secures the lowest rates, options exist for scores as low as 500.

Conventional Home Loans

Conventional loans, the most common mortgage type in the U.S., are offered by private lenders like banks. They require:

- Minimum 3% down payment

- Credit score of 620+

- Debt-to-income ratio below 44%

Private Mortgage Insurance (PMI) is required for down payments under 20%, costing 0.3%–1.5% of the loan annually. PMI ends once 20% equity is reached.

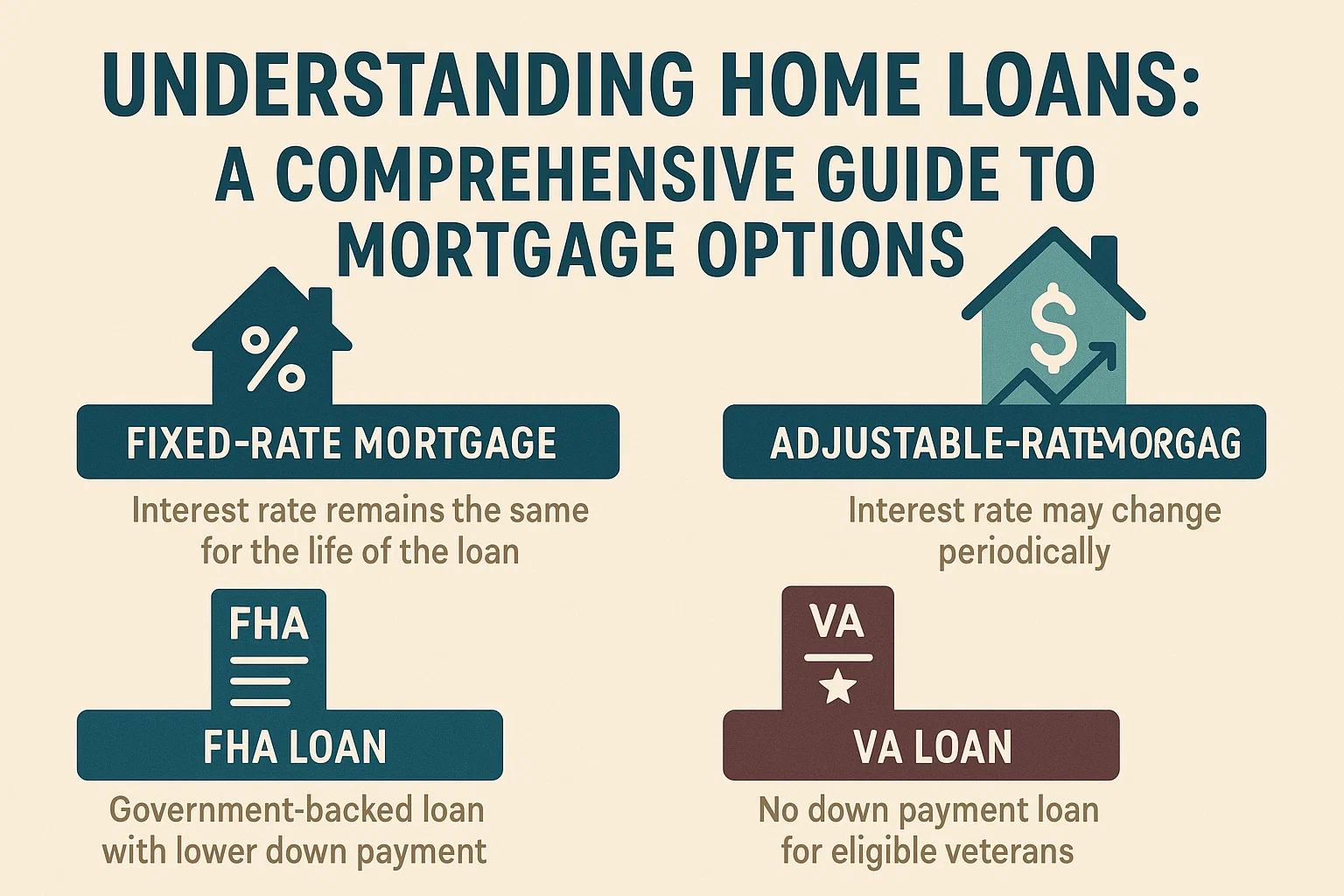

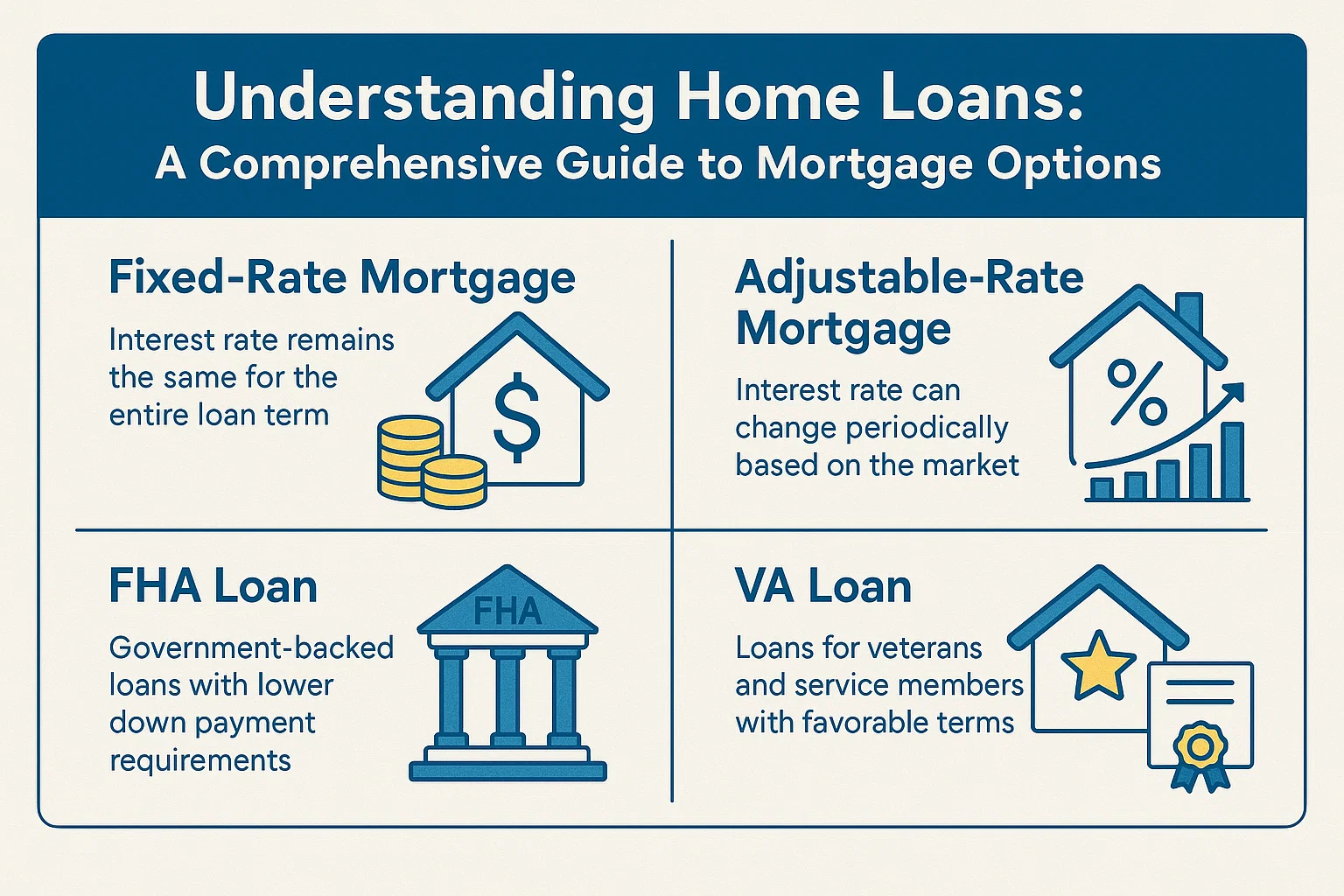

Fixed-Rate Mortgages

Offering stable payments over 15–30 years, fixed-rate loans are ideal for long-term homeowners who value predictability.

Adjustable-Rate Mortgages (ARMs)

ARMs start with a fixed rate (5–10 years) before adjusting annually. They suit buyers planning to sell or refinance before rates adjust.

Jumbo Loans

For homes exceeding conforming loan limits (up to $1 million in high-cost areas), jumbo loans require:

- Credit score of 700+

- 10%+ down payment

- Proof of significant cash reserves

Government-Insured Loans

These loans offer flexible qualifications but are restricted to primary residences.

FHA Loans

- Credit score: 500+ (10% down) or 580+ (3.5% down)

- Lifetime mortgage insurance required

USDA Loans

- No down payment required

- For rural/suburban areas (population limits apply)

- Income restrictions

VA Loans

- Exclusive to veterans, active military, and surviving spouses

- No down payment or PMI

- Low closing costs

Specialty Loan Options

Construction Loans

- Construction-Only: Short-term financing for building

- Construction-to-Permanent: Combines construction and mortgage

- Renovation Loans: FHA-backed 203(k) loans for home upgrades

Interest-Only Mortgages

Pay only interest for 5–15 years, then principal + interest. Best for short-term owners or investors.

Piggyback Loans

Avoid PMI with an 80/10/10 structure: 80% first mortgage, 10% second loan, 10% down payment. Requires strong credit (700+).

Choosing the Right Mortgage

Your financial situation, future plans, and homeownership goals determine the best loan. Consult a financial advisor or mortgage specialist to explore personalized options.