New Vs. Used Homes

The price of a used home can be misleading. Use our true cost of ownership calculator to discover how buying new could save you money in the long run.

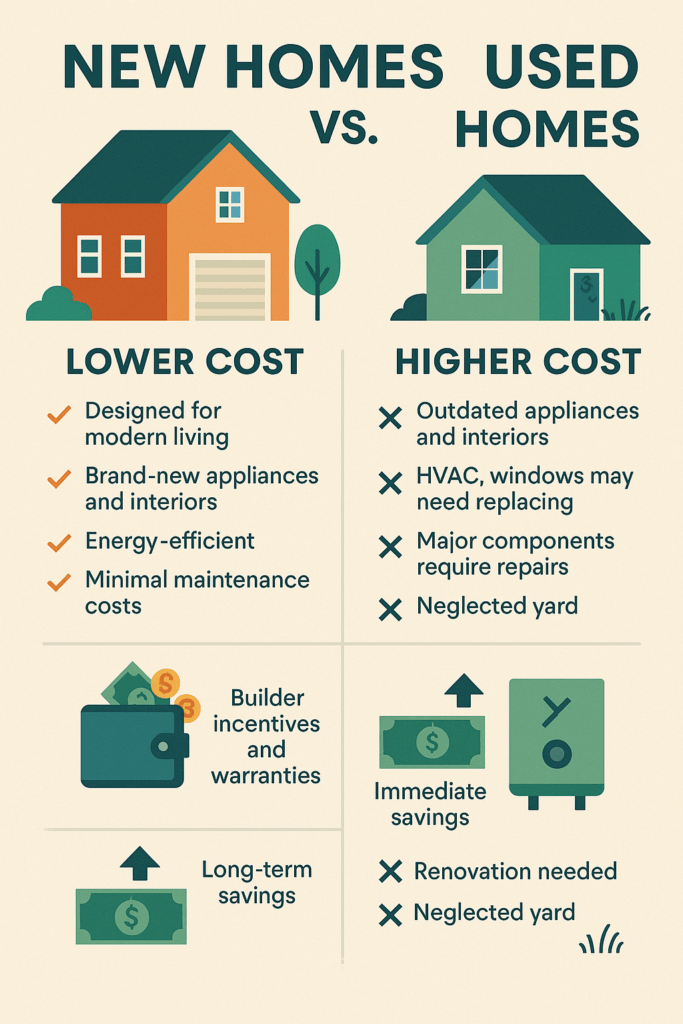

Used Homes Cost More

When looking for a new home you might be tempted to go with a resale to save some money upfront. A lower price tag means a smaller down payment and mortgage plus immediate savings you can use later to renovate the home to your liking—right?

In many ways new homes are a smarter investment than existing ones. You get a home designed for modern living with brand new appliances and interiors and still stay within your budget.

Buying new means your home is as energy efficient as possible—no drafty windows or outdated energy sucking HVAC systems. Plus you can trust all your appliances are new and won’t need repairs or replacements anytime soon. When you factor in builder incentives and warranties buying new often ends up saving you more in the long run.

New homes do come with some minor annual maintenance costs—HVAC servicing, seasonal landscaping or gutter cleaning—but these are minimal compared to the cost of repairing or replacing major components in an older home like a worn out water heater or a neglected yard. Over time the energy savings and reduced need for repairs will help you recoup the extra upfront cost of a new home and you can spend more on what matters most to you instead of on home repairs.

Need to fix your credit?

We have partnered with a top tier credit repair company to get quick results needed to get you approved.

New vs Used Home FAQS

Lenders determine how much they’re willing to lend by evaluating your finances, including your income, credit score, debt-to-income ratio, down payment, and the terms of your loan.

If you want to borrow more than the calculator suggests or your pre-qualification amount, increasing your income, saving for a larger down payment, or lowering your debt can help boost your borrowing capacity.

While lenders focus on key fixed expenses, homebuyers should also consider additional costs like childcare, travel, and lifestyle, as well as their financial stability and comfort level with managing debt.

Lenders often follow a general rule of thumb: no more than 28% of your gross monthly income should go toward housing expenses, and your total debt, including your mortgage, should not exceed 36%.

Affordability Calculator

Recomended Credit Rating