What is a Mortgage?

Enter the details of the home in the calculator below including the price of the home, taxes any fees. Also add the downpayment your able to do.

🏡 What Is a Mortgage?

If you’re planning to buy a home—especially a new construction home—chances are you’ll need a mortgage. But what exactly is a mortgage, and how does it work? At PreConstructionHomes.com, we’re here to help you understand the basics so you can make informed decisions with confidence.

📘 Mortgage Definition: The Basics

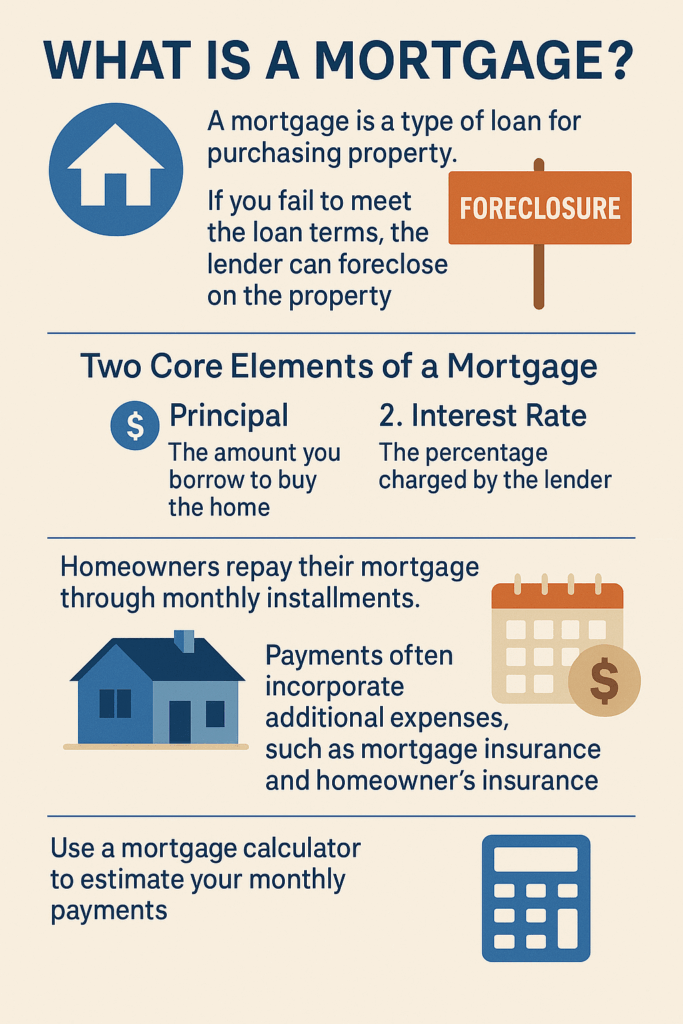

A mortgage is a type of loan used to purchase real estate. It allows homebuyers to borrow money from a lender (typically a bank, credit union, or mortgage company) to pay for a home. In exchange, the buyer agrees to repay the loan over time, usually with interest, through monthly payments.

Until the mortgage is fully paid off, the lender holds a legal claim (lien) on the property—meaning they can take possession of it if the borrower fails to meet the terms of the loan.

🔍 How a Mortgage Works

When you finance a home through a mortgage, your monthly payments typically include four key components, often referred to as PITI:

Principal: The amount you borrowed

Interest: The fee charged by the lender for borrowing the money

Taxes: Property taxes based on your home’s assessed value

Insurance: Homeowners insurance to protect against damage or loss

Some loans may also include PMI (Private Mortgage Insurance) if your down payment is less than 20%.

🧾 Common Mortgage Terms

There are several types of mortgage loans, but the most common include:

Fixed-Rate Mortgage: Interest rate stays the same over the life of the loan (usually 15, 20, or 30 years)

Adjustable-Rate Mortgage (ARM): Interest rate can change after an initial fixed period

FHA Loan: Government-backed loan with low down payment requirements

VA Loan: Available to qualified veterans with no down payment needed

Each loan type has its pros and cons, depending on your financial situation and how long you plan to stay in the home.

💬 Do You Need a Mortgage?

Most homebuyers—especially first-timers or those purchasing new construction homes—use a mortgage to afford their purchase. Paying in cash is possible, but for many buyers, a mortgage provides access to homeownership without requiring full upfront payment.

Why use a mortgage?

Spread out your payments over time

Build equity as you pay down the loan

Potential tax benefits

Lock in historically low interest rates (depending on market conditions)

✅ Getting Pre-Approved: Your First Step

Before touring model homes or selecting finishes, it’s smart to get pre-approved for a mortgage. This shows builders and agents that you’re a serious buyer and gives you a clear idea of your budget.

To get pre-approved, you’ll typically need to provide:

Proof of income (W-2s, pay stubs, tax returns)

Credit history

Employment verification

Asset and debt information

Many builders offer incentives if you work with their preferred lender, so be sure to ask during your tour.

🏗️ Mortgages for New Construction Homes

At PreConstructionHomes.com, we specialize in new builds—and the mortgage process for these homes can be a little different. You may encounter:

Extended rate locks to account for build time

Construction-to-permanent loans, if you’re building from scratch

Builder incentives to help cover closing costs or upgrades

Our team can help connect you with lenders experienced in new construction financing to simplify the process.

A mortgage is more than just a loan—it’s a powerful tool that helps you invest in your future and achieve homeownership. Whether you’re buying your first home, upsizing for your family, or selecting your dream finishes in a brand-new community, understanding how mortgages work is a crucial first step.

Explore your financing options, get pre-approved, and take the first step toward your new home at PreConstructionHomes.com.

Need to fix your credit?

We have partnered with a top tier credit repair company to get quick results needed to get you approved.

Mortgage FAQS

A mortgage is a type of loan used to buy a home. You borrow money from a lender (such as a bank or credit union) to pay for the property, and in return, you agree to repay the loan—plus interest—over time. Until the loan is fully paid off, the lender holds a legal claim (called a lien) on the property.

When you take out a mortgage, you’ll make monthly payments that typically include:

Principal: the amount you borrowed

Interest: the cost of borrowing

Taxes and Insurance: property taxes and homeowners insurance

Some loans also include private mortgage insurance (PMI). You make these payments over a set loan term—usually 15, 20, or 30 years—until the loan is paid off.

Not necessarily. If you have enough cash, you can buy a home outright without a mortgage. However, most homebuyers use a mortgage to afford a home, especially for higher-priced or new construction properties. A mortgage allows you to spread payments over time while building equity in your home.

Lenders evaluate several factors to decide if you qualify for a mortgage, including:

Credit score and credit history

Income and employment stability

Debt-to-income (DTI) ratio

Down payment amount

The property’s value (via appraisal)

A pre-approval helps estimate what you can afford and shows sellers you’re a serious buyer.

Get your credit report

Get Pre-Approved