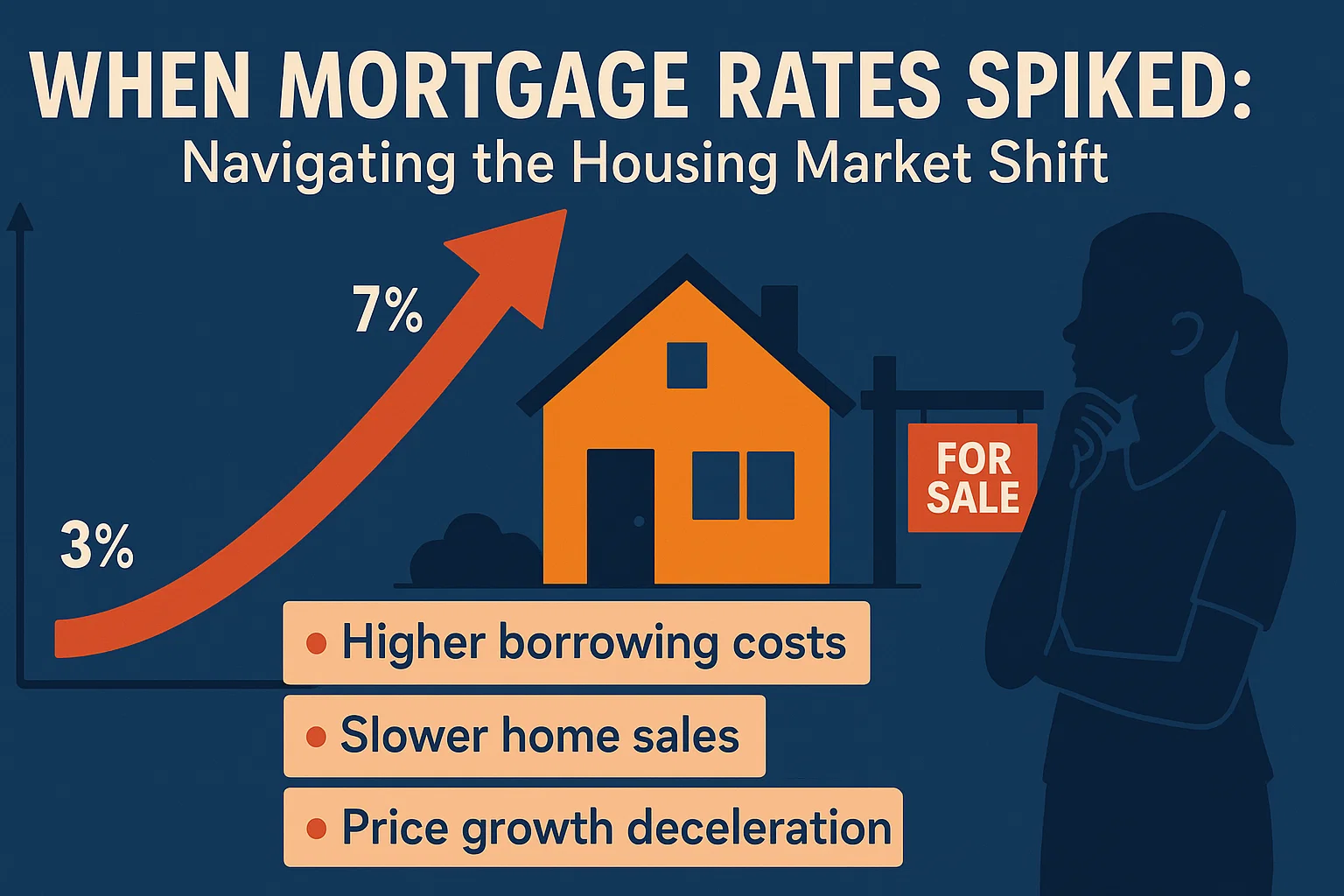

When Mortgage Rates Spiked: Navigating the Housing Market Shift

When Mortgage Rates Spiked: Navigating the Housing Market Shift

When mortgage rates surged from just under 3% in late 2025 to nearly 7% by late 2025, the housing market felt the shockwaves immediately. Though historically, rates between 5% and 6% are considered normal—and early 2025 saw a dip closer to 6%—buyers entering the new construction market faced unexpected financial hurdles. Despite this, demand for new homes remains robust as rates stabilize.

Industry professionals emphasize the importance of educating buyers on financial strategies. “Our approach is to equip sales teams and lenders nationwide to guide buyers through their options,” says a mortgage executive. “Programs exist to improve credit scores within 30–90 days, which can reduce private mortgage insurance (PMI) costs for those with down payments below 20%.”

Down Payments and Flexibility

A 20% down payment eliminates PMI, but increasing it to 25% has minimal impact on monthly payments. For example:

- $500,000 home with 20% down: $100,000 down, $400,000 loan at 6% = $2,398/month.

- 25% down: $125,000 down reduces payments by only $150/month to $2,248.

Builders are now offering pre-construction sales and incentives like closing cost assistance, giving buyers room to negotiate upgrades or plan future refinancing.

Financing Options to Manage Higher Mortgage Rates

Low Interest Rate Loans

Builders often partner with lenders to secure discounted rates for buyers. “A builder might pay upfront to offer rates below market—like 4.875% versus 6%—which attracts buyers,” explains a mortgage expert.

Temporary Rate Buydowns

Builders may subsidize a 3/2/1 buydown, lowering rates incrementally over three years (e.g., 3% Year 1, 4% Year 2, 5% Year 3). Buyers must qualify at the full rate (6% in this example).

Permanent Rate Buydowns

A permanent buydown locks in a lower rate for the loan term (e.g., 5.25% vs. 6.25%). Builder contributions to buydowns are capped between 2%–9% of the loan amount, depending on the program.

Long-Term Rate Locks

Lenders offer rate locks up to one year for a fee. “If rates drop, you can float down, and the fee rolls into closing costs,” notes a branch manager.

Adjustable-Rate Mortgages (ARMs)

Hybrid ARMs with fixed initial terms (5/7/10 years) regained popularity in 2025. These suit buyers planning to sell or refinance before adjustments occur.

Refinance Fee Waivers

Some lenders waive refinance fees within three years of purchase, easing the burden of future rate changes.

Timing the Market

“If rates drop below 5.5%, demand and prices could surge again,” warns a mortgage strategist. Collaborating with lenders and builders to secure favorable terms now may outweigh waiting for uncertain market shifts.