Understanding Private Mortgage Insurance (PMI): Key Facts and Strategies

Understanding Private Mortgage Insurance (PMI): Key Facts and Strategies

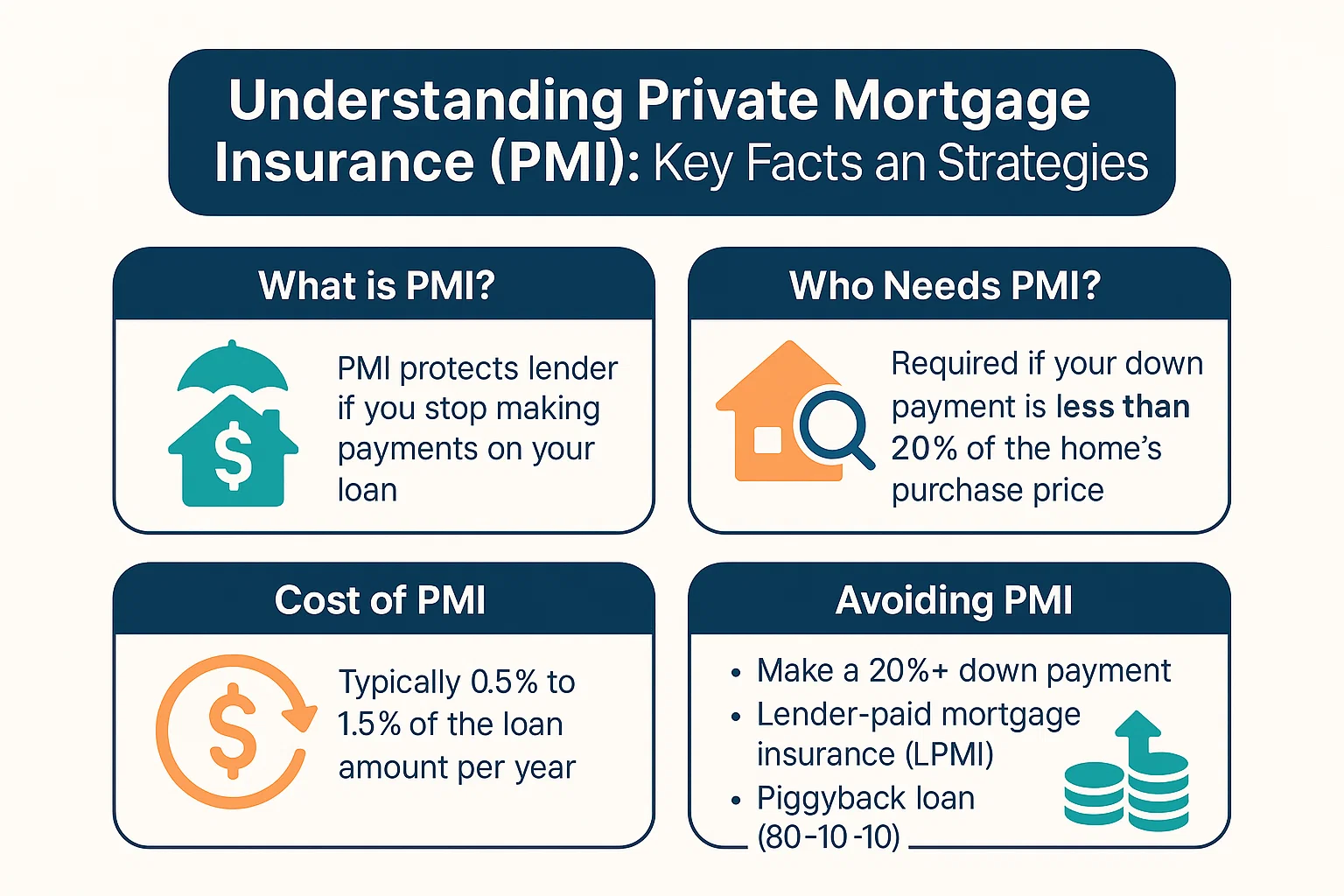

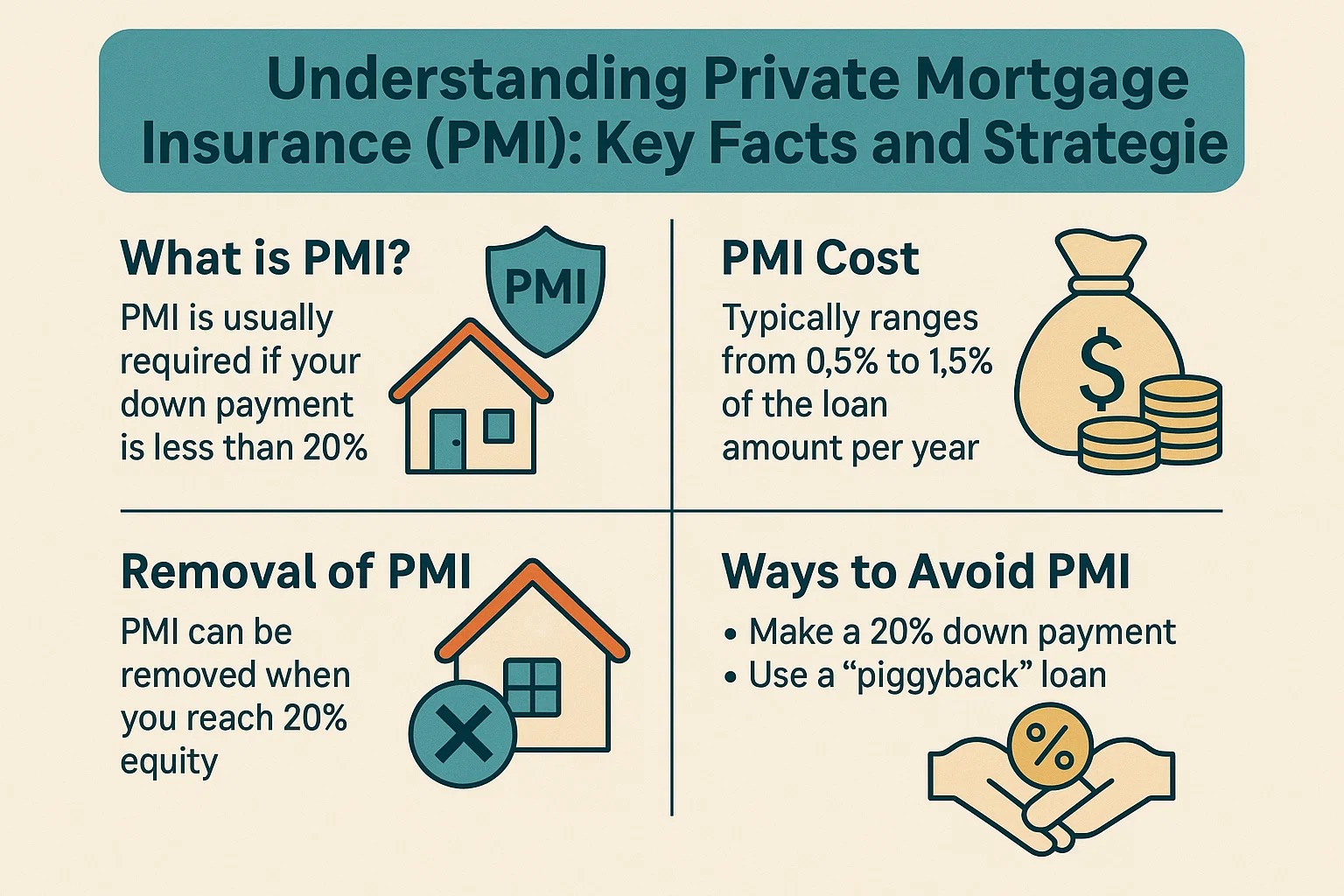

What Is PMI?

Private Mortgage Insurance (PMI) is an insurance policy that protects mortgage lenders from financial loss if a borrower defaults on their loan. Lenders typically require PMI for conventional loans with a down payment of less than 20%.

How Much Does PMI Cost?

PMI costs generally range from 0.5% to 1.0% of the total loan amount annually. The exact cost depends on factors such as:

- Loan amount

- Loan type and term

- Credit score

- Down payment size

How to Cancel PMI

Borrowers can request PMI cancellation once they reach 20% equity in their home. However, lenders are only legally obligated to remove PMI when the borrower attains 22% equity. On average, PMI remains active for 5–7 years, assuming timely mortgage payments.

Strategies to Avoid PMI

- Make a 20% down payment: This is the simplest way to avoid PMI entirely.

- Minimize PMI costs: A larger down payment reduces the loan amount, lowering PMI expenses.

- Use a second loan: Some buyers combine an 80% primary mortgage with a 10% down payment and a 10% secondary loan (e.g., a home equity line of credit). Consult a financial advisor before pursuing this option.

Tax Considerations

PMI premiums may be tax deductible under certain circumstances. Always evaluate the costs and potential savings of each approach with a tax professional.