Understanding Private Mortgage Insurance (PMI): Key Facts and Benefits

Understanding Private Mortgage Insurance (PMI): Key Facts and Benefits

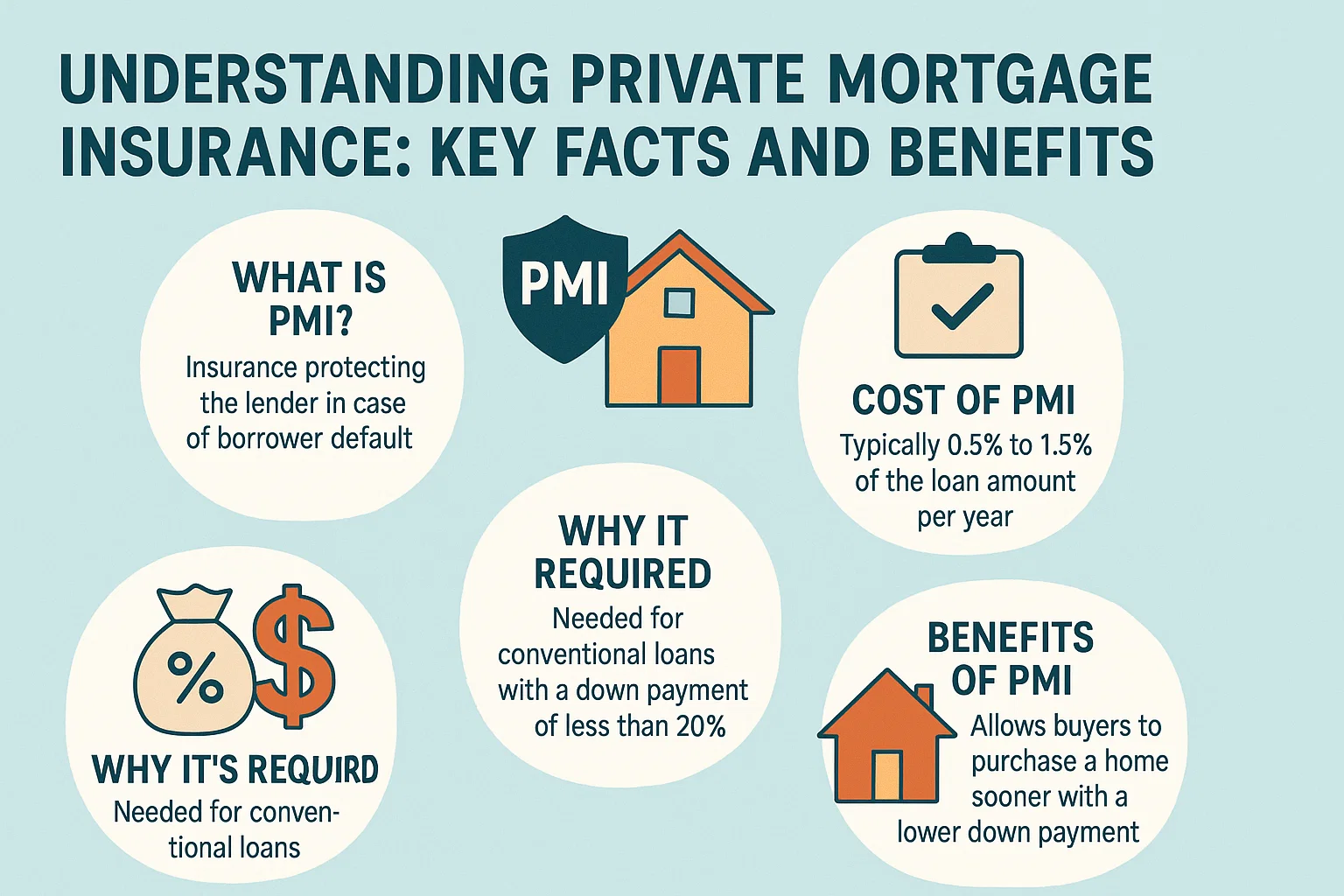

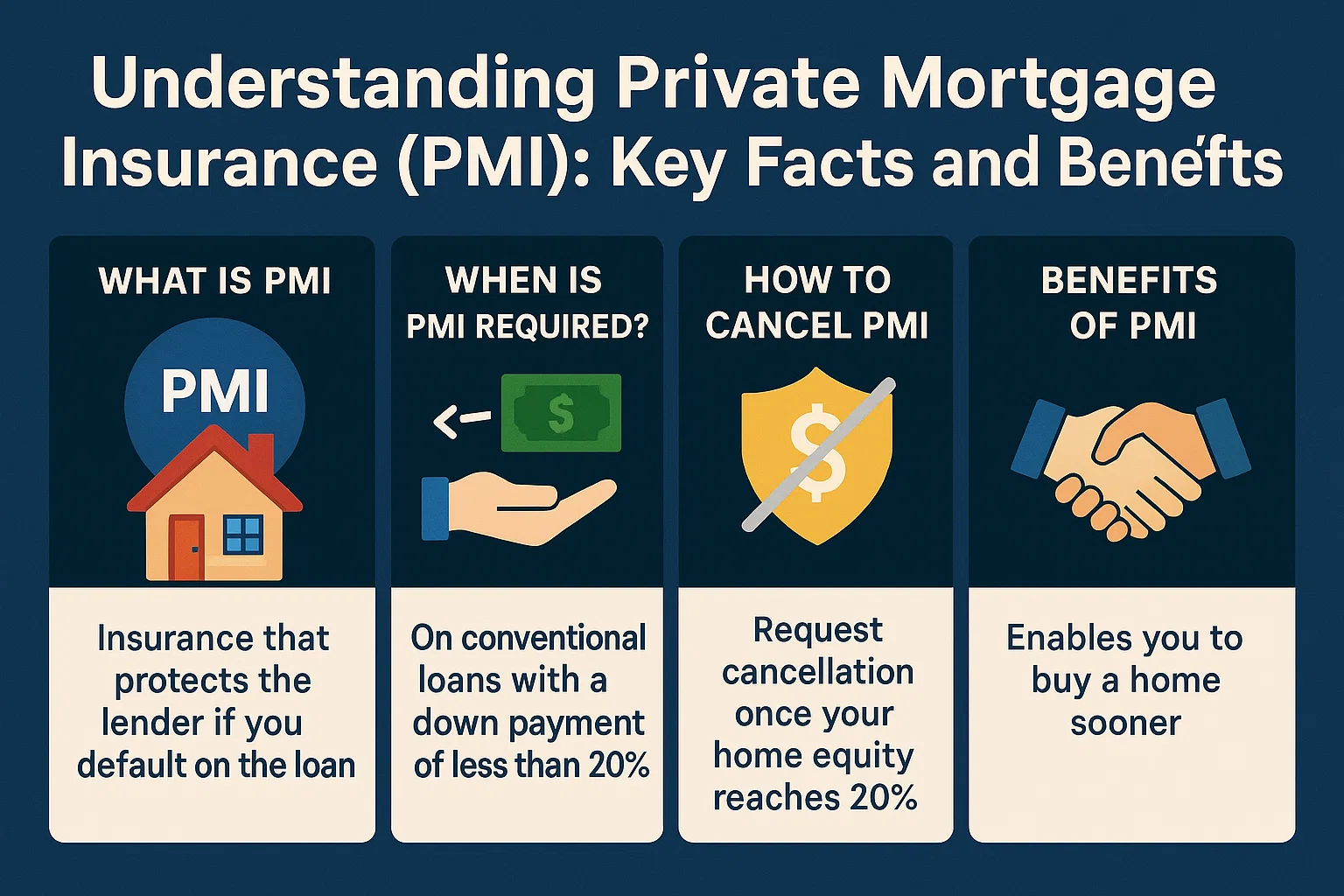

What Is Private Mortgage Insurance (PMI)?

Private Mortgage Insurance (PMI) is a safeguard for lenders if a borrower defaults on their loan. While it increases your monthly mortgage payment, PMI enables homeownership for buyers who may struggle with financial barriers like a small down payment or imperfect credit.

When Is PMI Required?

Lenders typically require PMI if your down payment is less than 20% of the home’s purchase price. It is also mandatory for government-backed loans, such as FHA loans, which are designed for low down-payment scenarios.

How Much Does PMI Cost?

PMI costs vary depending on the lender, down payment amount, and credit history. On average, it amounts to approximately 1% of the total loan annually. To calculate your monthly PMI cost, divide 1% of your loan amount by 12. This fee is added to your regular mortgage payment.

Is PMI Permanent?

No. Lenders are obligated to cancel PMI once your mortgage balance reaches 78% of the home’s original value or the midpoint of your loan term. You can also expedite PMI removal by making extra payments toward your principal balance.

Can You Eliminate PMI Through Refinancing?

Yes. If your home’s value has increased significantly, refinancing might allow you to drop PMI. A higher appraisal could show you now owe less than 80% of the home’s current value, meeting the equity threshold. Always factor in refinancing closing costs before proceeding. Alternatively, request a reappraisal to renegotiate PMI terms with your lender.

The Long-Term Value of PMI

While PMI raises short-term expenses, it supports long-term financial growth by making homeownership accessible. Over time, building equity through mortgage payments can contribute to wealth creation and stability.