Understanding Mortgage Rates and APR: Key Questions Answered

Understanding Mortgage Rates and APR: Key Questions Answered

The mortgage process can be complex, especially when navigating terms like interest rates and annual percentage rates (APR). To help clarify these critical concepts, here are answers to four common questions that could save you thousands over the life of your loan.

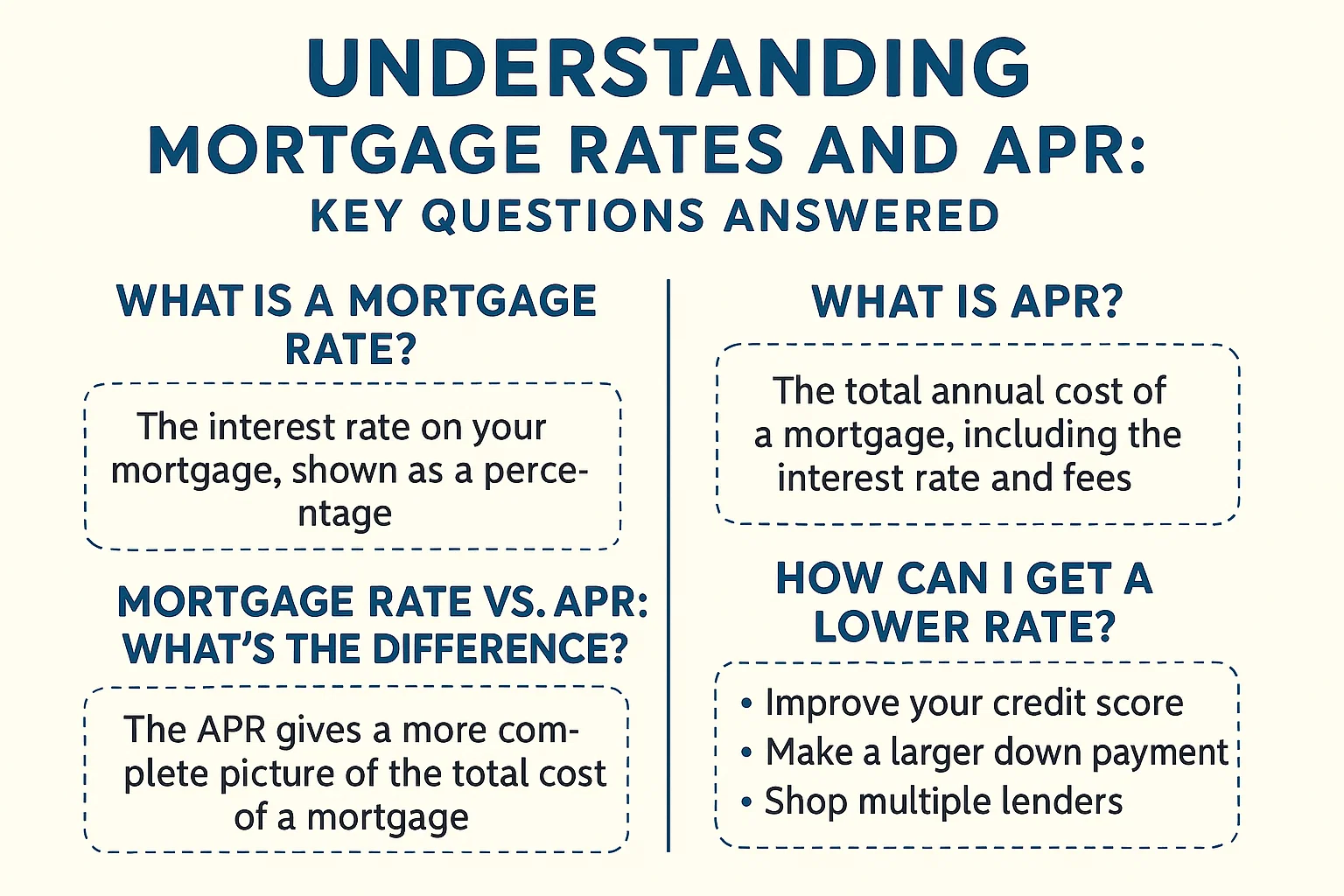

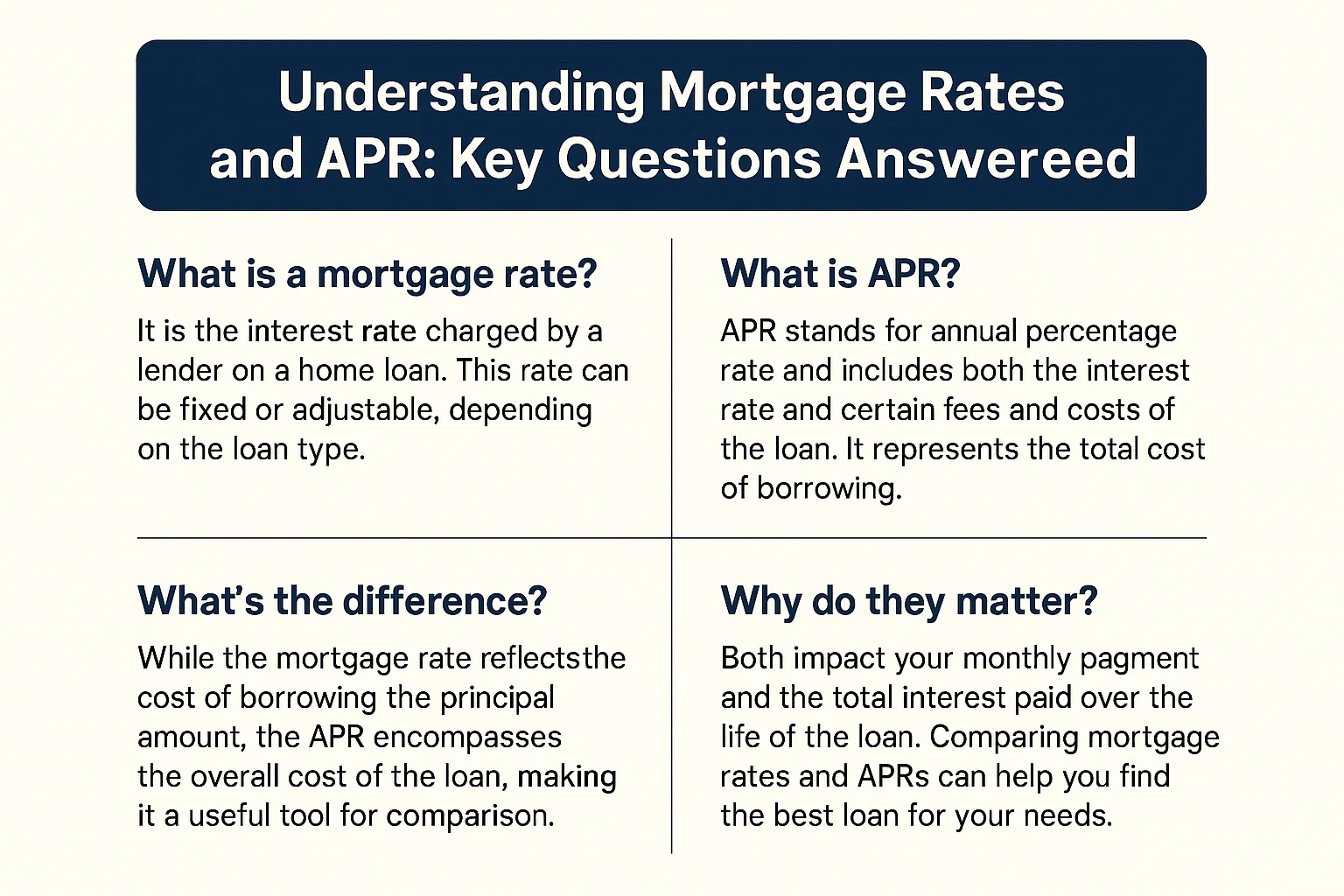

1. What’s the Difference Between Mortgage Interest Rate and APR?

The mortgage interest rate determines your monthly payment and reflects the cost of borrowing funds. The APR, however, provides a broader view by including the interest rate plus additional loan-related expenses, such as:

- Fees

- Discount points

- Closing costs

- Mortgage insurance (if applicable)

Both rates are expressed as percentages, but the APR offers a more comprehensive measure of your loan’s total cost.

2. Why Is My APR Higher Than My Interest Rate?

The APR is typically higher because it incorporates all loan-related fees in addition to the base interest rate. Lenders may include different fees depending on the loan type, which can cause variations in APR calculations. Since these fees are spread over the entire loan term, the APR reflects a long-term cost projection.

3. How Should I Use These Rates to Compare Loans?

Use the interest rate to evaluate monthly payment affordability, and rely on the APR to assess the loan’s total cost over its lifespan. If you prioritize lower monthly payments, focus on the interest rate. If minimizing overall expenses matters more, the APR will guide your decision. Note that APR calculations assume you’ll keep the loan for its full term—if you plan to refinance or sell early, the APR may not accurately reflect your costs.

4. When Should I Lock In My Mortgage Rate?

The ideal timing depends on your financial goals and market conditions. Many borrowers wait until they’ve found a home to lock in a rate, but consult with a loan officer to determine the best strategy for your situation. Avoid rushing into decisions based on advertised “lowest rates”—stay informed and seek expert guidance throughout the process.

Final Tips

Comparing interest rates and APRs side by side allows you to weigh both short- and long-term costs effectively. Always review loan estimates carefully and ask questions to ensure you fully understand the terms before committing.