Understanding Mortgage Preapproval: Your Path to Homeownership

Understanding Mortgage Preapproval: Your Path to Homeownership

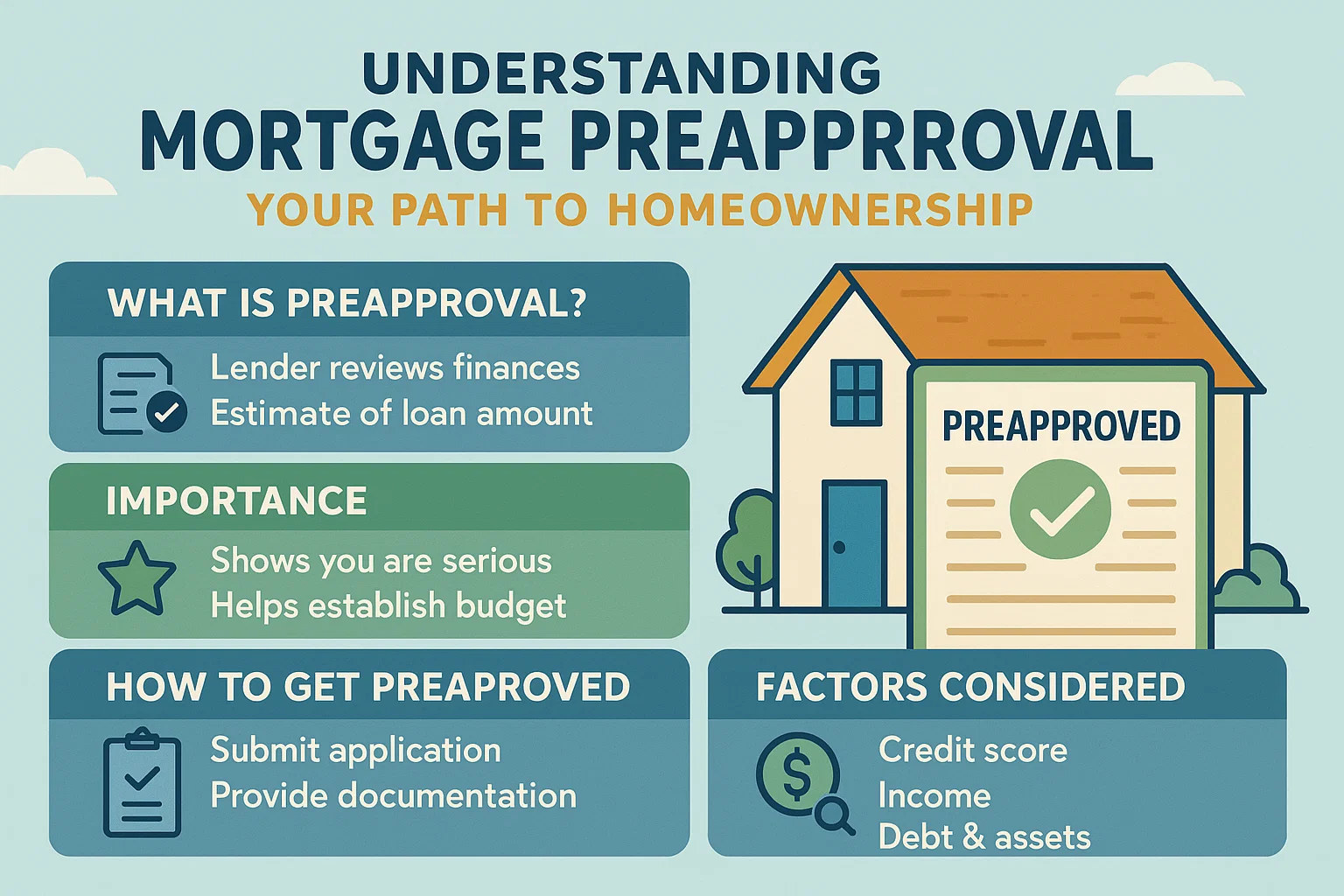

You’ve done your homework and know you need to work with a mortgage professional to get preapproved for a loan. But what does preapproval mean exactly, and will it ensure that you’ll be able to purchase your dream home? Follow along as we break down the preapproval process and how to navigate it successfully.

Prequalifying vs. Preapproval

You’ve probably heard the terms prequalification and preapproval used interchangeably—but they’re not the same. Here’s the distinction:

Prequalification

Prequalifying is a preliminary step where you discuss your financial situation with a loan officer to estimate how much you might qualify to borrow. No documents are submitted, and your credit report isn’t pulled. Think of it as first base in the homebuying process: It gets the ball rolling but doesn’t guarantee success.

Preapproval

Preapproval, on the other hand, is like reaching third base. This involves a thorough review of your financial documents, including income verification, bank statements, and a credit check. A mortgage professional evaluates your application to determine if you’ll qualify for a specific loan amount. Preapproval signals serious intent to sellers and strengthens your offer.

Does Preapproval Guarantee a Loan?

“Preapproval is not a commitment to lend you money. Nor is it a guarantee from the lender. It is simply the lender’s way of saying they will likely approve you for a certain amount, as long as you clear the underwriting process.”

Even with preapproval, final loan approval depends on clearing underwriting requirements. Changes to your finances, employment, or credit during the process can still derail your application.

Why Preapproval Matters in Homebuying

Preapproval offers several advantages:

- Credibility with Sellers: It shows you’re a serious buyer with verified finances, reducing the risk of delays or deal breakdowns.

- Competitive Edge: In a seller’s market, preapproval can make your offer stand out against others.

- Clarity on Budget: You’ll know exactly how much you can afford, streamlining your home search.

How Long Does Preapproval Last?

Preapproval typically expires after 90 days. Lenders require updated financial documents and a new credit check if your home search extends beyond this period. Avoid major financial changes during this time to keep your approval intact.

Avoiding Loan Approval Pitfalls

Stay vigilant about these factors to ensure a smooth path to closing:

Employment Stability

Keep your job status consistent. Switching careers, becoming self-employed, or resigning can jeopardize your loan. Discuss any changes with your mortgage professional first.

Credit Health

Avoid new credit inquiries, late payments, or paying off large debts without consulting your lender. Even small changes can raise red flags during underwriting.

Debt-to-Income Ratio (DTI)

Don’t take on new debt (e.g., auto loans, leases) or make large purchases on credit. Stick to cash for big expenses to keep your DTI unchanged.

Bank Account Activity

Avoid large deposits, transfers, or opening/closing accounts. Lenders prefer steady, predictable financial behavior.

Final Steps to Closing

Preapproval brings you closer to homeownership, but the game isn’t over yet. Work closely with your mortgage professional, keep your finances stable, and act quickly to secure your dream home within the 90-day window. With careful planning, you’ll be rounding the bases toward a successful closing.