The Essential Guide to Mortgage Rate Locks

The Essential Guide to Mortgage Rate Locks

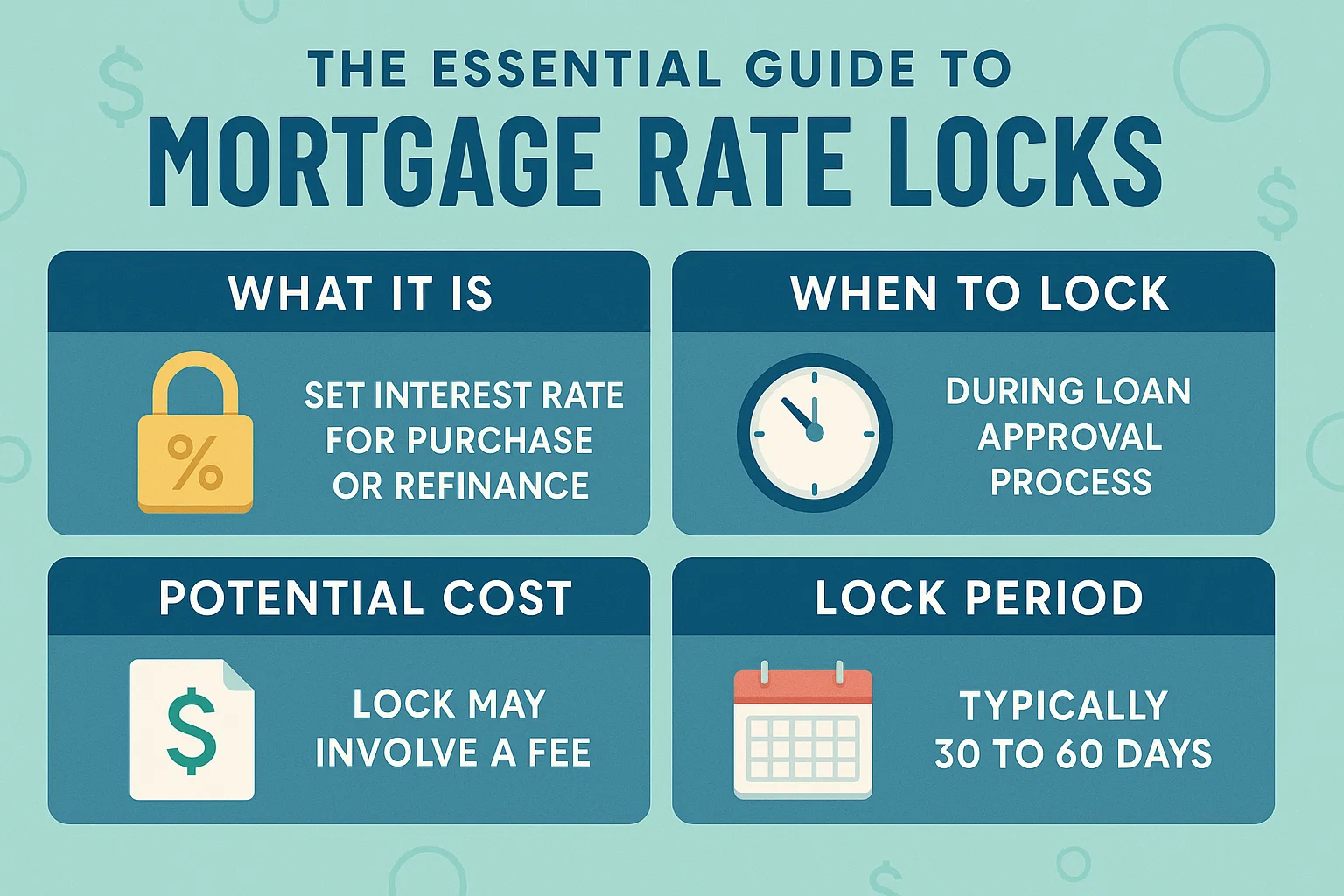

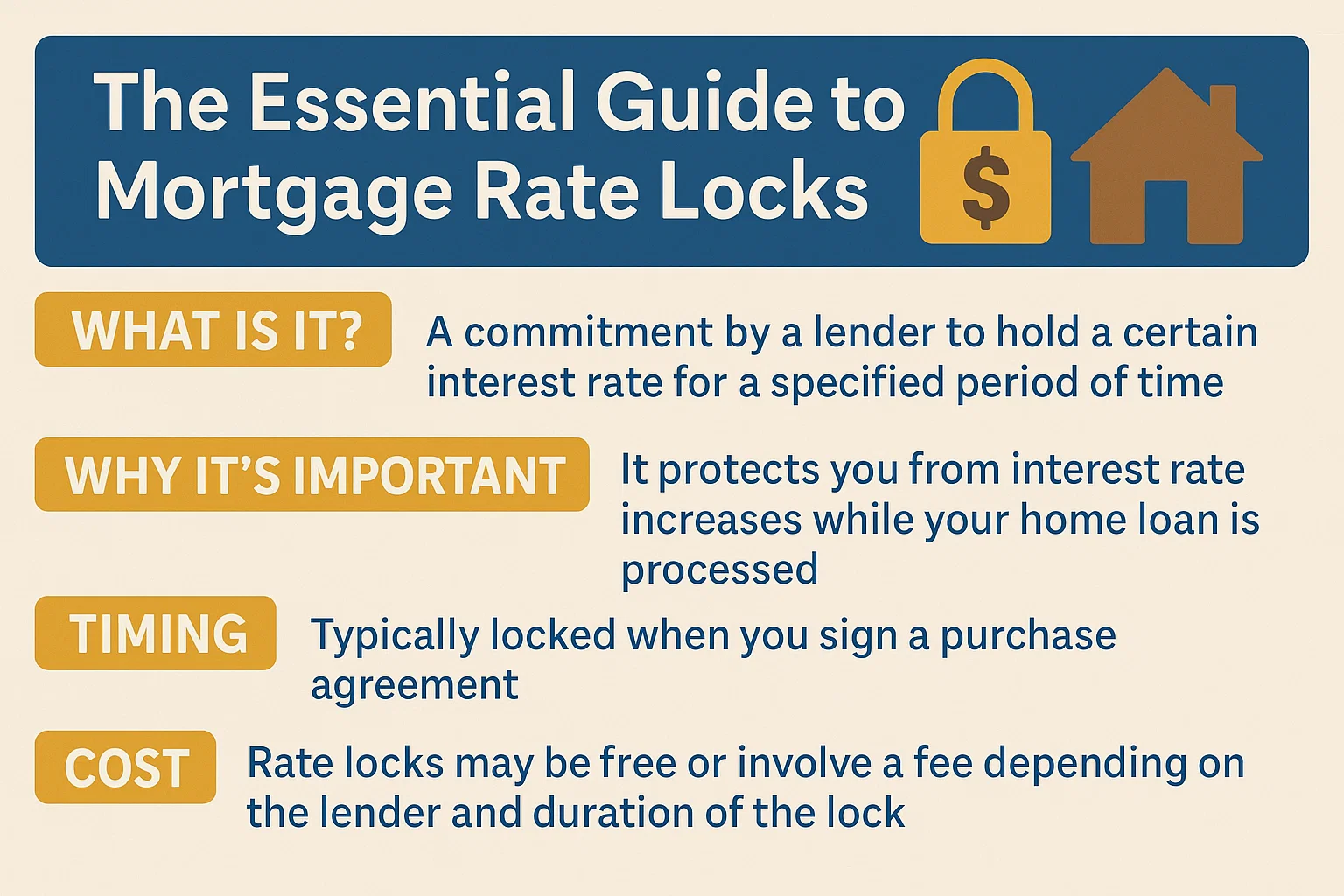

What Does “Locking Your Rate” Mean?

Locking your interest rate means your lender guarantees a specific rate for a set period, typically 30, 45, or 60 days. Shorter or longer terms may be available, though extended locks often come with higher fees. Your rate remains protected as long as you:

- Close within the agreed timeframe

- Avoid changes to your application

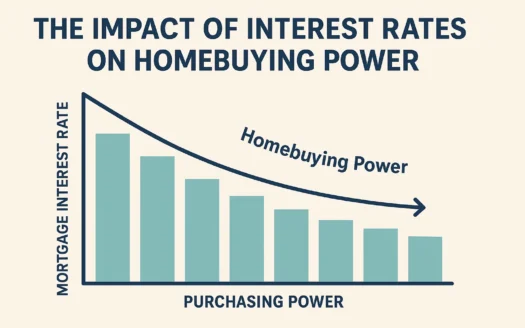

Why Mortgage Rates Are Unpredictable

Interest rates fluctuate constantly due to global events, economic shifts, or market trends—sometimes changing within hours. For example, bond yield increases or geopolitical developments can cause sudden spikes or dips. This volatility makes timing your rate lock critical.

Strategies for Timing Your Rate Lock

Your closing date plays a pivotal role. If you secure a favorable rate but need more time to close, paying a fee to extend the lock might be worthwhile. Rule of thumb: If the rate fits your budget, lock it in. However, waiting could save money if rates drop—though there’s no guarantee they will.

Weighing the Risks

Locking too early might mean missing out on potential rate declines. Conversely, delaying could expose you to rising rates. Mortgage professionals often advise monitoring the market while staying prepared to act decisively.

Final Tips for Homebuyers

No one can guarantee the “best” rate, but understanding your financial limits and market trends empowers smarter decisions. Stay informed, consult your lender, and prioritize a rate that aligns with your timeline and goals. Remember: In rate locks, timing is everything.