Navigating Home Loans: A Glossary for New Buyers

Navigating Home Loans: A Glossary for New Buyers

Adjustable-Rate Mortgage (ARM)

Most ARMs today are hybrid loans with a period of one, five, seven, or 10 years at a fixed rate followed by adjusting interest rates. These loans often start with a lower interest rate than fixed-rate options, potentially saving you money during the initial period.

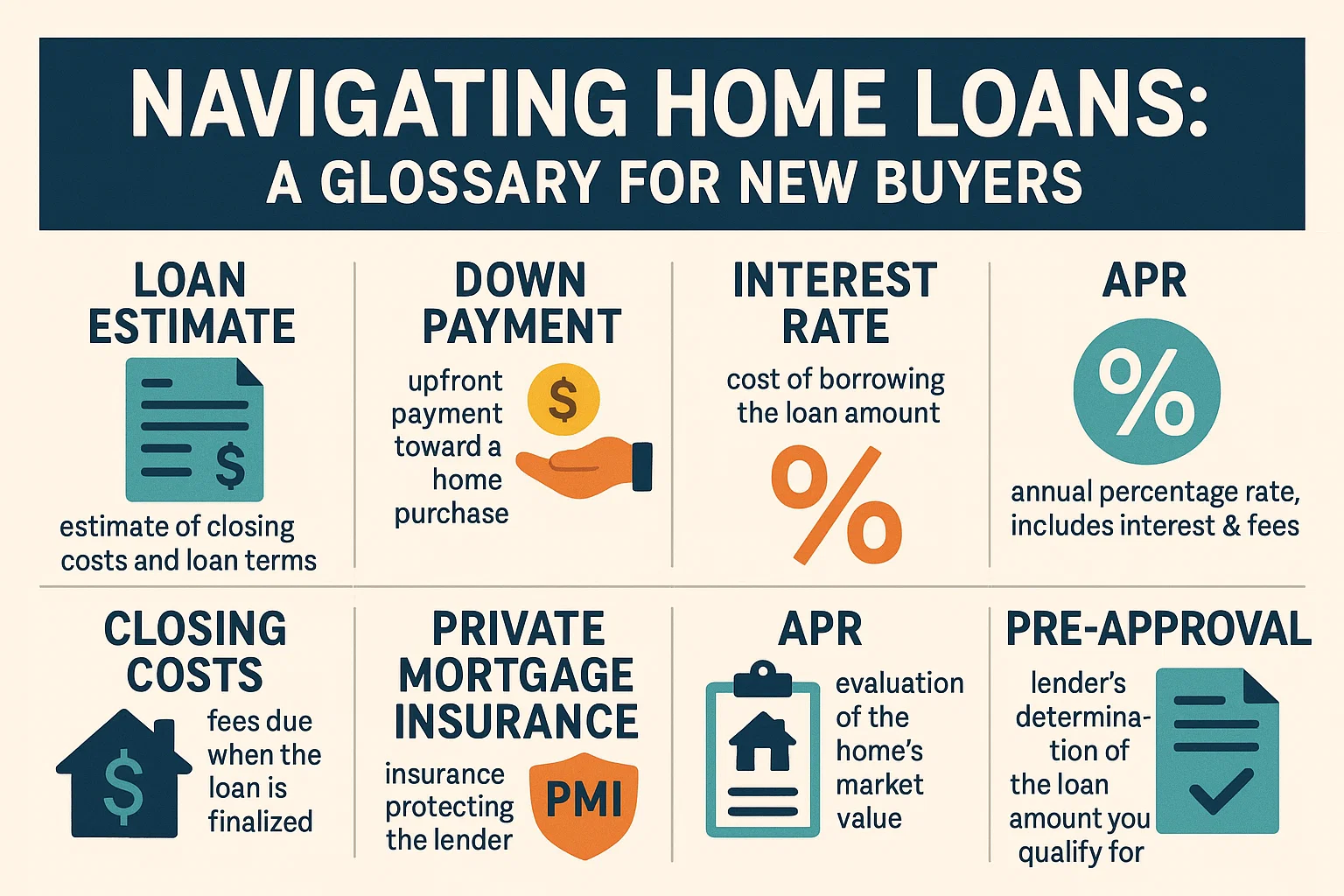

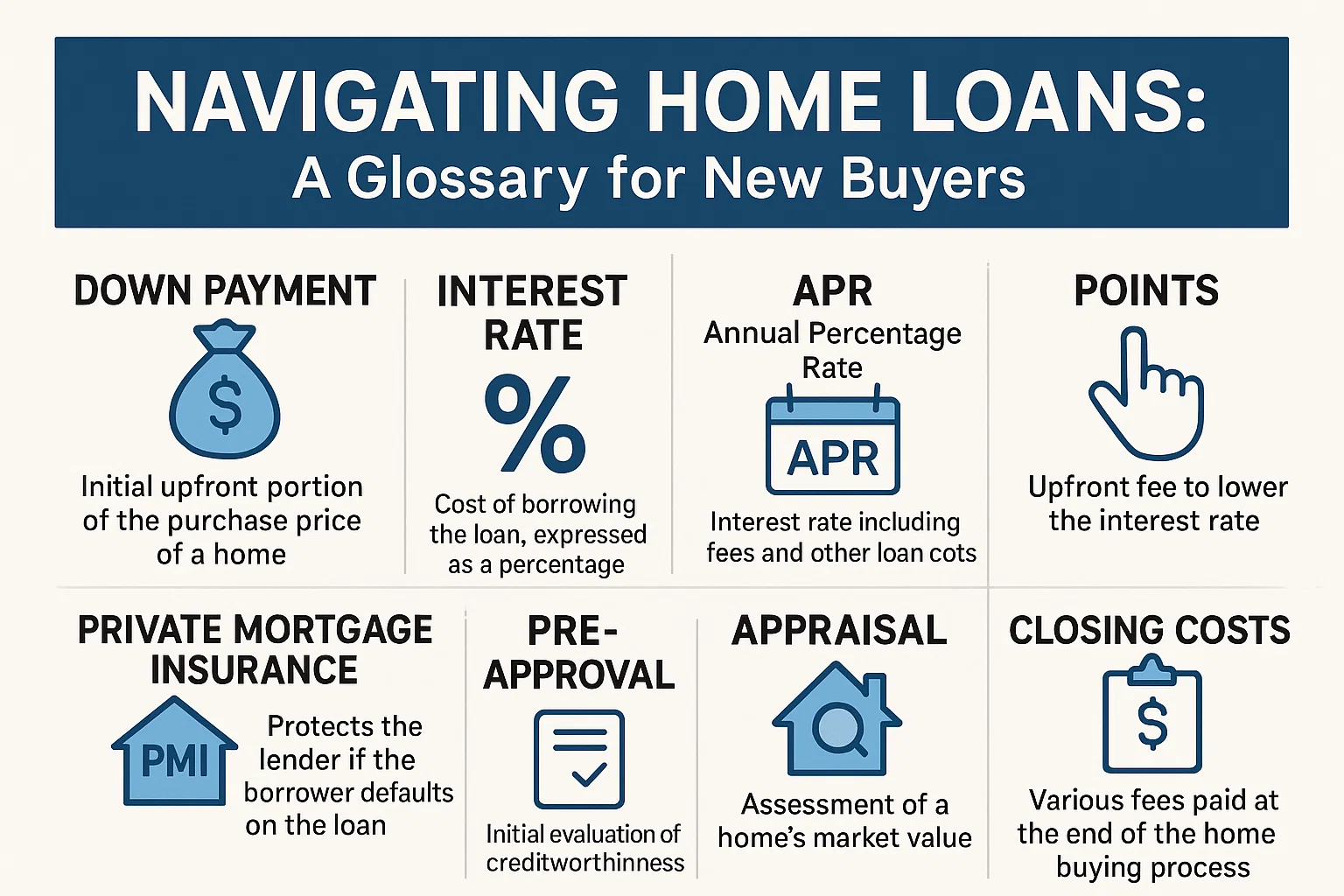

Appraisal

An estimate of a home’s value, used by lenders to verify if the property is worth the purchase price. New home values are typically based on land costs and other factors.

Bridge Loan

Short-term financing to cover timing gaps, such as buying a new home before selling your current one. Lenders use your existing home’s equity as collateral.

Builder Financing

Builders often partner with mortgage companies to offer financing options to buyers, streamlining the purchasing process.

Construction Loan

Short-term funding for building a home, typically converted to a long-term mortgage after construction. Ideal for custom builds or acting as your own contractor.

Conventional Loan

Loans designed for sale to Fannie Mae or Freddie Mac, requiring 10–20% down payments. Lower down payments may require costly private mortgage insurance (PMI).

Credit Restoration Program

Services aimed at improving your credit score to qualify for better loan terms.

Credit Score

A numerical rating (300–850) that impacts loan eligibility, interest rates, and employment opportunities. Scores of 650–699 are considered fair by most lenders.

Debt-To-Income Ratio

A comparison of your monthly debt payments to your gross income, used to assess loan affordability.

Discount Points

Upfront fees paid at closing to reduce your loan’s interest rate. One point equals 1% of the loan amount.

Down Payment

The initial cash investment to secure a home purchase, varying based on loan terms and available funds.

FHA Loan

Government-backed loans with low down payments (as low as 3.5%) and flexible credit requirements.

FICO Score

The most widely used credit score (300–850), calculated using payment history, debt levels, credit age, and other factors.

Financial Profile

A summary of your employment, credit, and debt history. Frequent job changes or new credit applications during the “quiet period” may affect loan approval.

Fixed-Rate Loan

A mortgage with a consistent interest rate and principal payment. Taxes and insurance costs may still cause payment changes over time.

Interest

The cost of borrowing money, paid regularly at a rate determined by your creditworthiness and lender terms.

Job History

Lenders prefer stable employment; frequent job changes may hinder loan approval.

Jumbo Loan

Financing for amounts exceeding conventional loan limits, requiring larger down payments (20–25%) and stricter credit standards.

Loan Terms

The duration of your loan. Shorter terms (e.g., 15 years) reduce total interest paid, while 30-year terms lower monthly payments.

Mortgage

A legal agreement granting conditional home ownership to a lender as loan collateral. The lien is removed once the loan is repaid.

Preapproval

A lender’s conditional commitment to fund your loan, valid for 90 days. Helps define your home search budget.

Pre-Qualification

A preliminary assessment of your eligibility for a loan, based on unverified financial information.

Principal

The unpaid portion of your loan amount.

Private Mortgage Insurance (PMI)

Required for down payments under 20%. PMI can be paid monthly, upfront, or via a higher interest rate.

Quiet Period

A critical phase before closing where financial changes (e.g., new debt) can jeopardize loan terms or approval.

Reverse Mortgage

An FHA-insured option for homeowners over 62, allowing home purchases with a 40–50% down payment. No monthly payments are required; the loan is repaid when the homeowner leaves the property.

Single-Close Financing

Also called a construction-to-permanent loan (C2P), this automatically converts to long-term financing after home completion.

Spending Plan

A budget outlining affordable home costs, including principal, interest, taxes, and insurance.

USDA Rural Loans

Zero-down-payment loans for eligible buyers in designated rural areas, often with income restrictions.

VA Loan

No-down-payment mortgages available to active-duty military personnel and veterans.