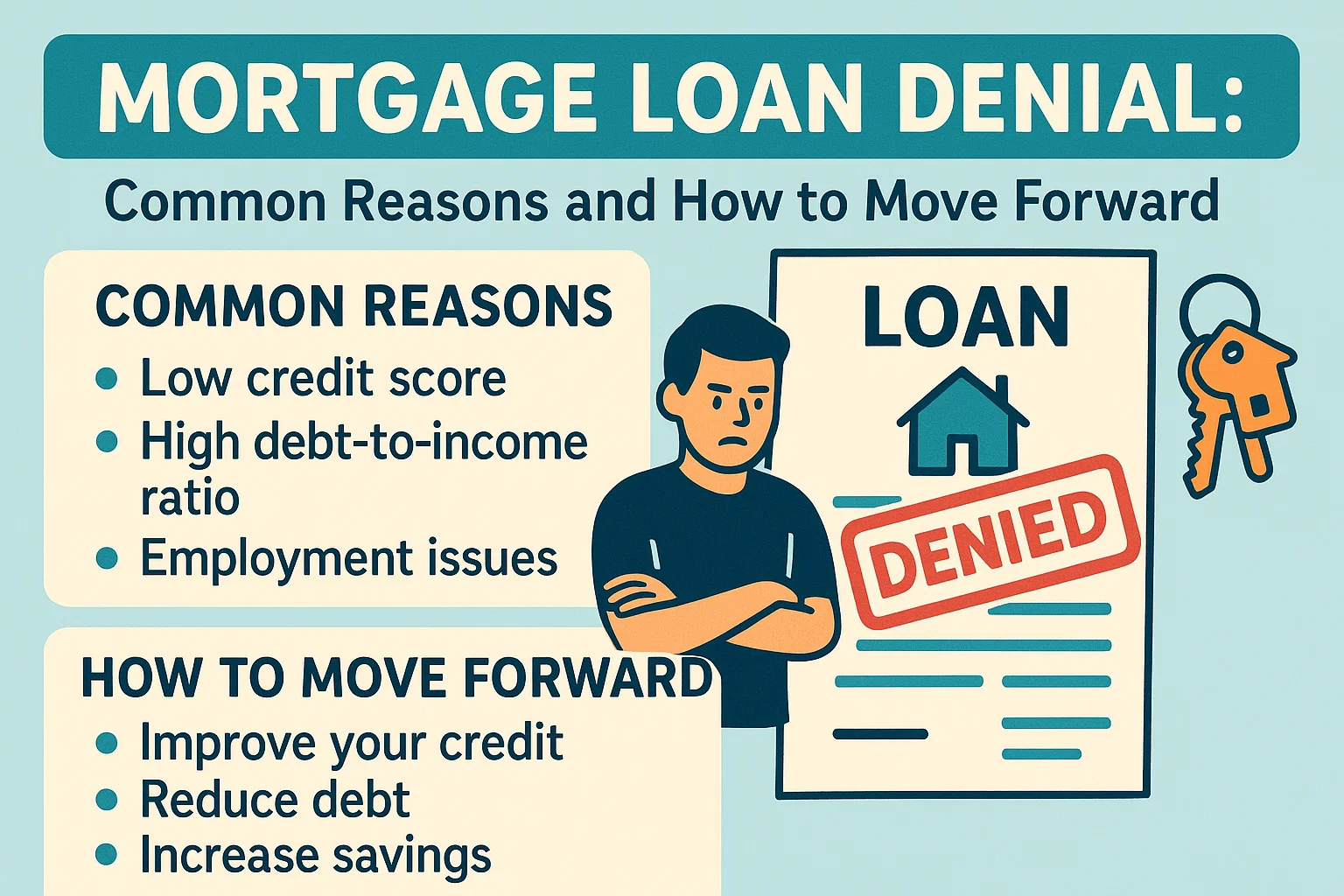

Mortgage Loan Denial: Common Reasons and How to Move Forward

You Finally Found It — The Home of Your Dreams. But Now It’s Slipping Away Because Your Mortgage Loan Application Was Denied.

Amidst all of the emotions you’re feeling, it can start to feel like there’s no next step. Buying a home is an emotional process when everything goes perfectly; any missteps amplify all of those emotions, and a loan denial can feel devastating. Since the 2008 housing crash, lenders have become more cautious, lending standards are more stringent, and now even those with a high credit score are not guaranteed approval.

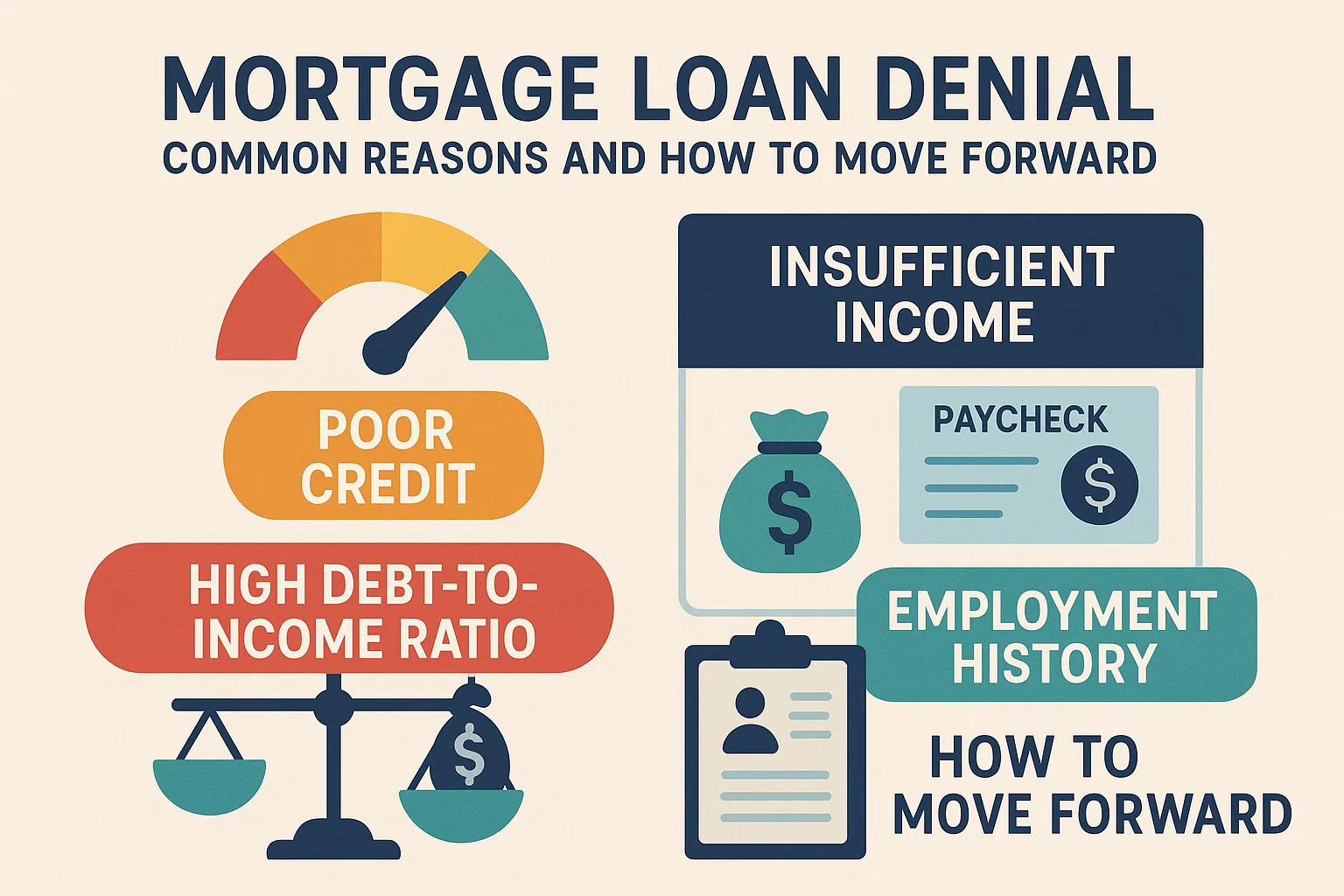

Why Would a Home Loan Be Denied?

You can’t fix what you don’t know, so first find out why your application wasn’t approved. Lenders are required to provide a rejection letter explaining the reason behind their decision, and you can always ask the loan officer for more information. Here are a few common reasons loans are denied, and what you can do next in each situation.

Debt-to-Income Ratio (DTI) Too High

Lenders are looking for financially sound investments, and having a high debt-to-income ratio increases risk. If your monthly debt payments take up a large percentage of your income, this indicates to lenders that adding another debt payment such as a mortgage is likely to make you more financially unstable.

What to do next:

- Avoid opening new lines of credit for 6–12 months before applying.

- Focus on paying off existing debts.

- Increase income through raises, side jobs, or refinancing.

Poor Credit

A low credit score can limit your mortgage options. To improve your score:

- Dispute inaccuracies on your credit report.

- Set up auto-payments to avoid missed deadlines.

- Build credit history with small loans or credit cards.

Low Down Payment

A down payment (typically 5–20%) signals commitment to lenders. If denied due to a low down payment:

- Reassess your budget to offer a stronger payment.

- Explore loans with lower down payment requirements.

Unstable Employment

Lenders prefer consistent job history. If denied due to employment:

- Work toward stable employment while improving credit and DTI.

- Use the time to save for a larger down payment.

Unexplained Income or Expenses

Unusual transactions can raise red flags. When reapplying:

- Document all income sources and expenses.

- Provide written proof for large monetary gifts.

Missing Information

Omitted details can lead to denial. Always:

- Double-check application accuracy.

- Disclose debts or financial challenges upfront.

Risky Moves After Pre-Approval

Avoid damaging your credit post-pre-approval. If denied due to new debt:

- Wait to reapply until finances stabilize.

Low Home Appraisal

If the home’s appraisal is too low:

- Negotiate a lower price with the seller.

- Pay the difference out of pocket.

Before Applying for a Mortgage

Prepare proactively to avoid denial:

- Know Your Credit Score: Check reports from all three bureaus and fix errors.

- Manage Your Debt: Consolidate payments without closing long-term accounts.

- Manage Your Expectations: Stay realistic about affordability.

A mortgage loan denial is an obstacle, but it doesn’t have to derail your home search. Evaluate your situation, make improvements, and reapply as a stronger candidate. Have questions about buying or building a home? Visit Pre-ConstructionHomes.com’s Learn Center for more resources.