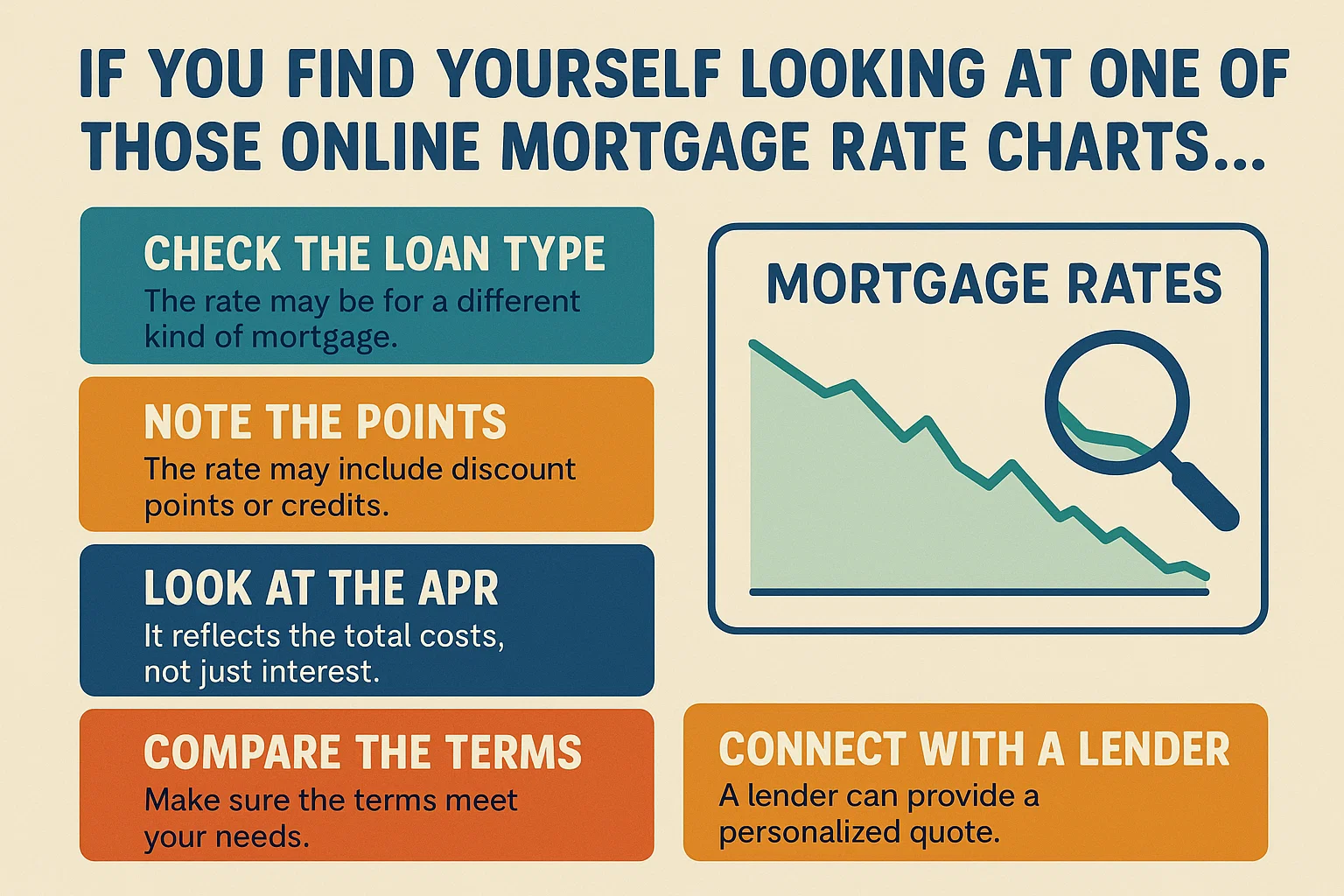

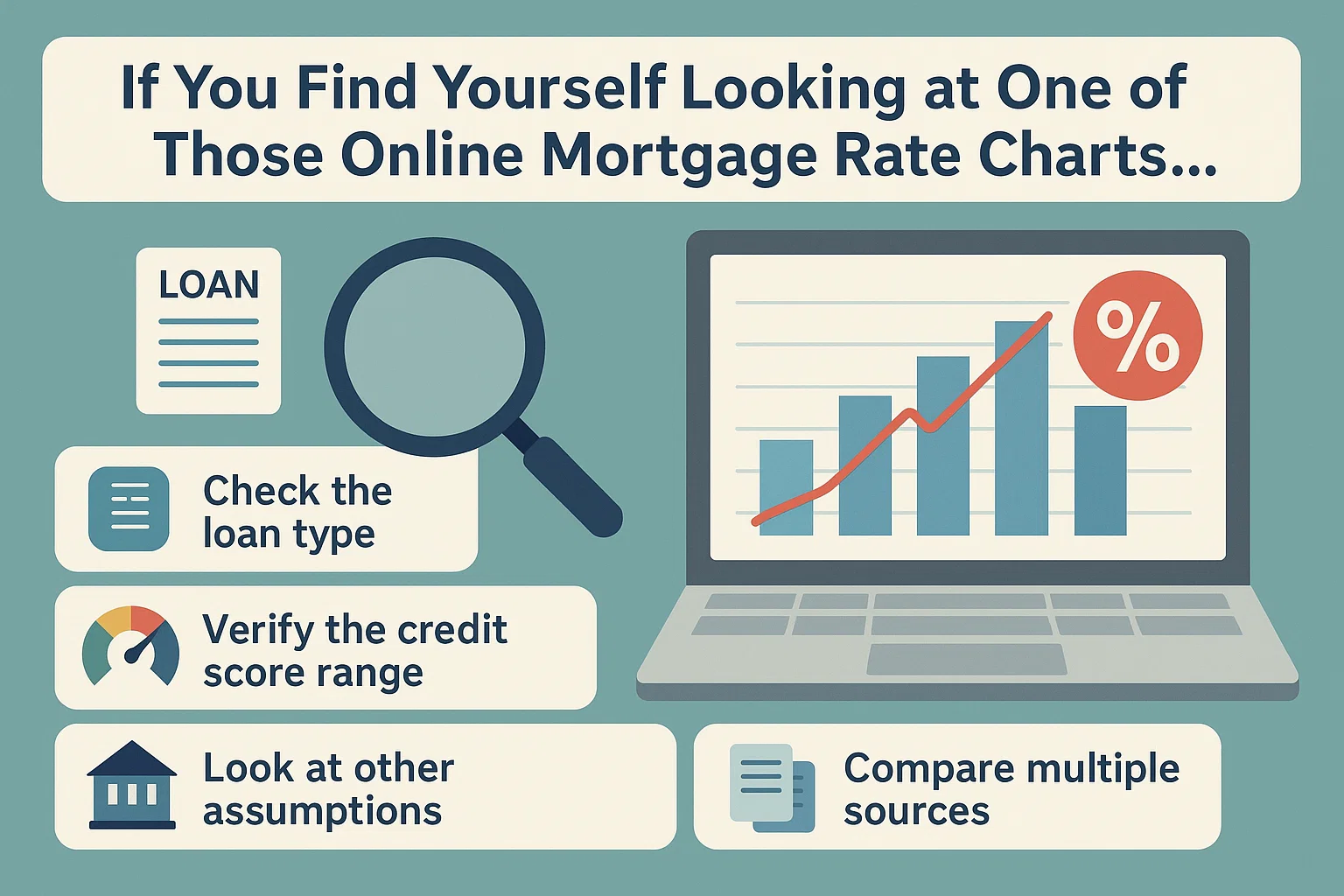

If You Find Yourself Looking at One of Those Online Mortgage Rate Charts…

If You Find Yourself Looking at One of Those Online Mortgage Rate Charts…

Adjustable-rate mortgages (ARMs) can look pretty tempting, particularly with those low initial interest rates. While this type of loan has its advantages, it isn’t right for everyone. In fact, an adjustable-rate mortgage could end up costing you more (lots more) in the long run. Want to see if an adjustable-rate mortgage is a good fit for your needs? Let’s dive in.

What’s an Adjustable-Rate Mortgage?

To start, let’s dive into what an adjustable-rate mortgage (ARM) is in the first place. The majority of U.S. mortgages are fixed-rate mortgages, which offer a single interest rate across the entire loan term (usually 30 years). Adjustable-rate mortgages, on the other hand, have rates that can change. “Adjustable-rate mortgages have a fixed rate for a number of years and then adjust based upon a benchmark rate, with a margin added on top,” explains Bobby Heytota, director of secondary markets for online lender Better.com.

ARMs are typically expressed with two numbers, such as a 5/1 ARM. The first number indicates the length of the fixed period (five years), and the second represents how often the rate adjusts after that (once per year). “ARMs typically have a lower initial rate compared to fixed-rate mortgages,” says Heytota. However, after the fixed period, there’s a risk the rate could increase—taking your monthly payment and overall housing costs with it.

Pros and Cons of ARMs

Pros

- Lower Initial Rates: ARMs often start with rates 0.75% or more below fixed-rate loans, leading to lower monthly payments and less interest upfront.

- Potential Rate Decreases: If the benchmark index tied to your loan falls, your rate and payments could decrease.

- Faster Equity Building: Lower initial rates allow you to pay down your principal faster, boosting equity.

Cons

- Rate and Payment Risk: Rates can rise significantly after the fixed period, straining your budget.

- Complexity: ARMs come with fees, rate caps, and penalties that require careful review.

When to Use an ARM

Deciding whether to use an ARM hinges on risk versus reward. Consider one if:

- You plan to sell or refinance before the fixed-rate period ends.

- Initial ARM rates are significantly lower than fixed rates (Heytota suggests avoiding ARMs if the rate difference is less than 0.50%).

- Your income is stable or expected to rise before adjustments begin.

When Not to Use an ARM

- Long-Term Homeownership: The risk of rising rates over decades is high.

- Tight Budgets or Fixed Income: Payment increases could cause financial stress.

- Minimal Rate Difference: A small gap between ARM and fixed rates may not justify the risk.

The Bottom Line

Always weigh your mortgage options and risks carefully. Consider your long-term goals, income stability, and risk tolerance. Consult a mortgage professional to determine the best path for your financial situation.