Get Your Finances in Order: A Step-by-Step Guide to Qualifying for a Home Loan

Get Your Finances in Order: A Step-by-Step Guide to Qualifying for a Home Loan

Whether you plan to buy an existing home or a newly built property, your financial preparations should start a year or more before you turn the key to open your new front door. You need to save money for your purchase, develop a spending plan, and build a credit profile that proves you’ll responsibly repay your loan.

Financing a Newly Built Home

One advantage of buying a new home is the stretch of time between the contract and move-in day, which can last from four to nine months or longer—as opposed to 30 to 60 days for a resale. You can use this time to reduce debt and save more money for your move, a task made easier with the motivation of watching your home being built.

A challenge, easily overcome when working with an experienced lender, is finding the right loan program to match your timeframe. For example:

- Discuss potential requirements with a lender early, such as presale conditions for loan approval.

- Consider working with a builder’s preferred lender who understands the nuances of new construction financing.

- Opt for a long-term interest rate lock if borrowing close to your maximum payment comfort level.

“When you’re buying a newly built home, you need to talk to a lender as early as possible about potential requirements for things, such as a certain number of homes needing to be presold before any loan can close.”

Steps Along the Path to Loan Approval

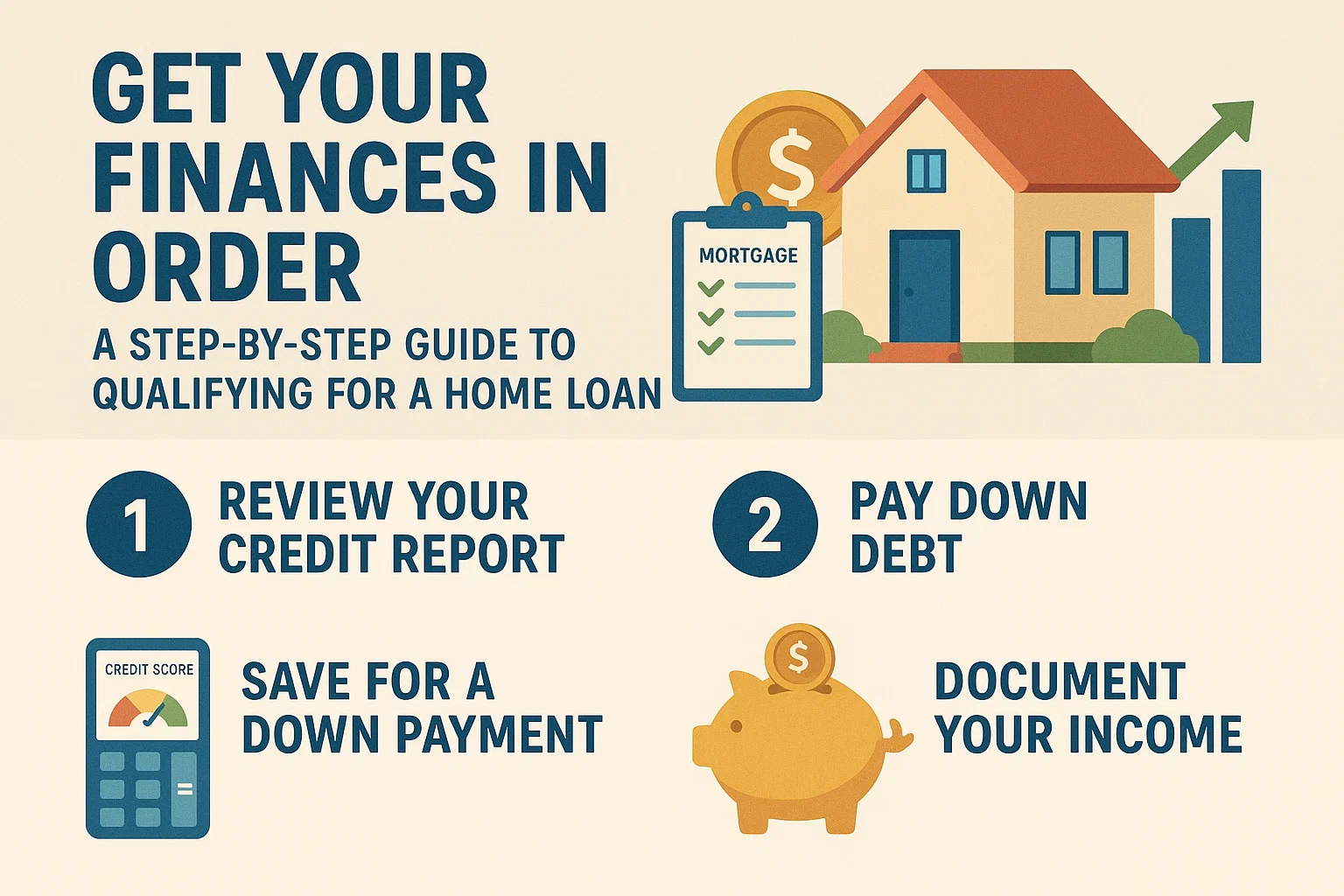

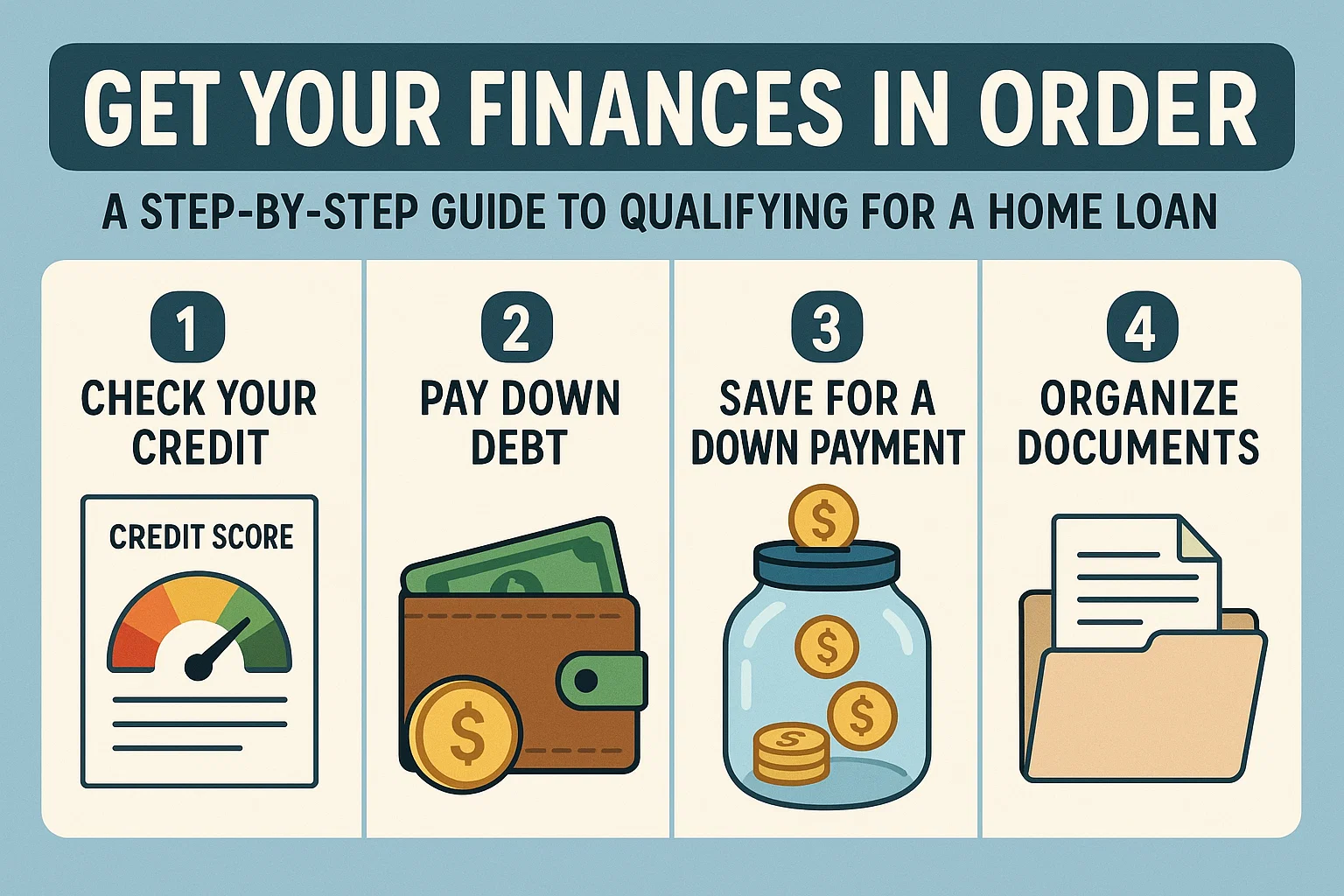

Homeownership requires stable finances, including the following elements:

1. Solid Job History

- A steady employment history is critical. Frequent job changes can complicate loan approval.

- Avoid switching to self-employment during the application process, as lenders typically require two years of documented self-employment income.

2. Create a Spending Plan

- Your monthly housing payment (including principal, interest, taxes, and insurance) should not exceed 33% of your gross monthly income.

- Factor in additional costs like homeowner association dues and mortgage insurance.

3. Start Saving Early

- Save 3–5% of the home price for a down payment and an additional 2–3% for closing costs (unless covered by the builder).

- Build cash reserves for moving expenses, landscaping, and unexpected costs.

“Consolidate funds for your home purchase into one accessible savings account to simplify documentation.”

4. Check Your Credit Report

- Review your credit report early to address any errors or blemishes.

- Maintain at least three active lines of credit with a consistent repayment history.

“No credit is as bad as having bad credit. Establish a positive repayment history early.”

5. Get Preapproved for a Loan

- Secure a formal preapproval to determine your budget and streamline the final approval process.

- Use this preapproval to shop confidently within your price range.

6. Improve Your Credit Score

- Avoid taking on new debt or applying for credit during the loan process.

- Pay all bills on time and reduce credit card balances.

- Use free credit score checkers to monitor progress.

“Pay credit card balances early before your credit is pulled to avoid appearing overextended.”

By following these steps, you’ll position yourself to qualify for a home loan and transition smoothly into homeownership. Start early, stay disciplined, and prioritize financial stability every step of the way.