FICO vs. VantageScore: Key Differences and How to Improve Your Credit

FICO vs. VantageScore: Understanding Credit Scoring Models

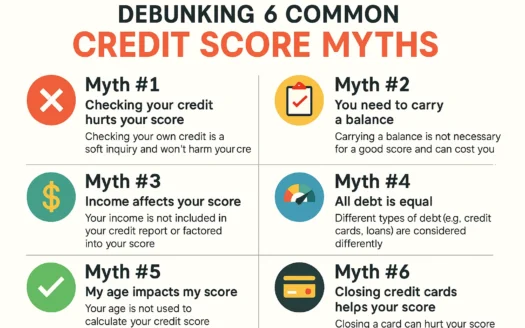

What Are FICO and VantageScore?

When applying for a loan, lenders review your credit score to assess your financial reliability. The two most common scoring models are FICO and VantageScore. While both generate scores ranging from 300 to 850, their methodologies differ significantly.

How FICO Scores Work

FICO scores, developed by the Fair Isaac Corporation, analyze data from the three major credit bureaus: Experian, Equifax, and TransUnion. The scoring model evaluates five key categories:

- Payment History (35%): Timely payments boost your score, while late or missed payments lower it.

- Amounts Owed (30%): High debt levels relative to credit limits can negatively impact your score.

- Length of Credit History (15%): Older accounts contribute positively, provided they’re managed well.

- Credit Mix (10%): A diverse mix of credit types (e.g., credit cards, loans) can improve your score.

- New Credit (10%): Opening multiple accounts quickly may lower your score, especially with limited credit history.

These weights may vary slightly depending on individual financial circumstances.

How VantageScore Differs

VantageScore uses similar credit data but prioritizes factors differently. Key distinctions include:

- Shorter Credit History Requirement: Only one month of history is needed, compared to FICO’s six months.

- Severity of Late Payments: Late mortgage payments are penalized more harshly than other late payments.

- Paid Collections: Paid collection accounts are excluded, whereas FICO ignores collections under $100.

VantageScore often favors individuals with limited credit history, potentially offering higher scores in such cases.

Tips to Boost Both Credit Scores

To improve your creditworthiness under either model:

- Pay bills on time, every time.

- Keep credit utilization below 30% of your limit.

- Avoid opening unnecessary new accounts.

Scoring Criteria Comparison

| Factor | FICO Weight | VantageScore Weight |

|---|---|---|

| Payment History | 35% | Highly Influential |

| Debt Levels | 30% | Moderately Influential |

| Credit Age | 15% | Less Influential |