Essential Tips for a Successful Loan Application

Essential Tips for a Successful Loan Application

Applying for a loan can be a pivotal step toward achieving your financial goals, whether you’re financing a vehicle, expanding a business, or purchasing property. To ensure a smooth process and improve your chances of approval, follow these key strategies:

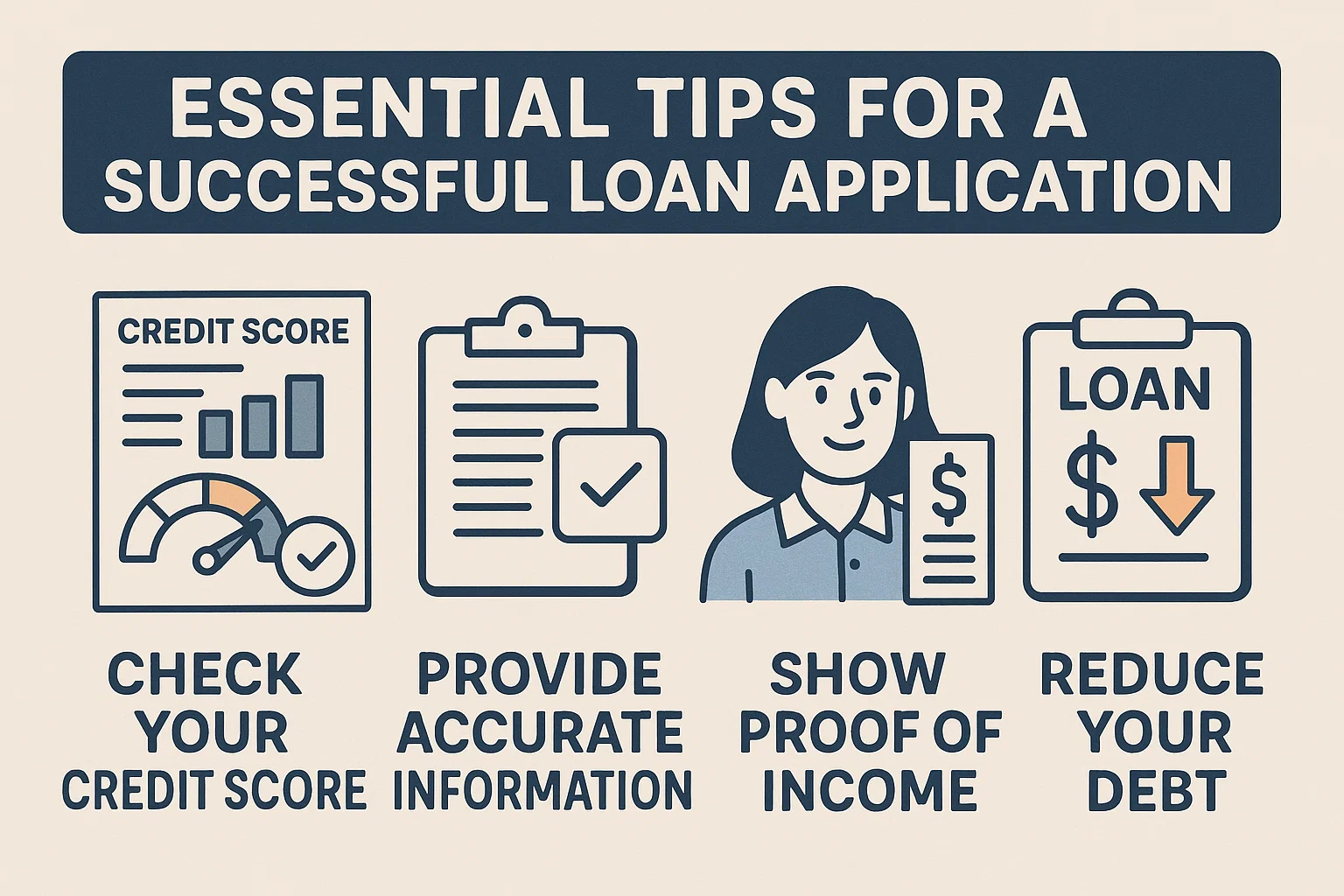

1. Review Your Credit Profile

Why it matters: Lenders prioritize creditworthiness when evaluating applications. A higher credit score often leads to better interest rates and terms.

- Obtain a free credit report from authorized agencies.

- Dispute inaccuracies or outdated information promptly.

- Pay down existing debts to lower your credit utilization ratio.

2. Compare Lending Options

Not all loan providers offer the same benefits. Consider these factors:

- Interest rates: Fixed vs. variable options.

- Fees: Origination charges, prepayment penalties, or late fees.

- Loan terms: Shorter terms may save money over time.

3. Organize Financial Documentation

Prepare these documents to streamline your application:

- Recent pay stubs or tax returns (proof of income).

- Bank statements and investment account details.

- Employment verification or business financial records.

4. Calculate a Realistic Budget

Before committing to a loan:

- Use online calculators to estimate monthly payments.

- Account for potential rate increases in adjustable-rate loans.

- Ensure repayments fit comfortably within your income.

5. Avoid Common Pitfalls

- Don’t rush: Hastily accepting the first offer may lead to unfavorable terms.

- Avoid multiple applications: Excessive credit inquiries can lower your score.

- Read the fine print: Clarify prepayment rules, balloon payments, or hidden clauses.

Final Thoughts

Thorough preparation and research are critical to securing a loan that aligns with your financial needs. By addressing credit health, comparing lenders, and understanding the terms, you’ll position yourself for a successful borrowing experience.